漸積突破トレーディング戦略

概要

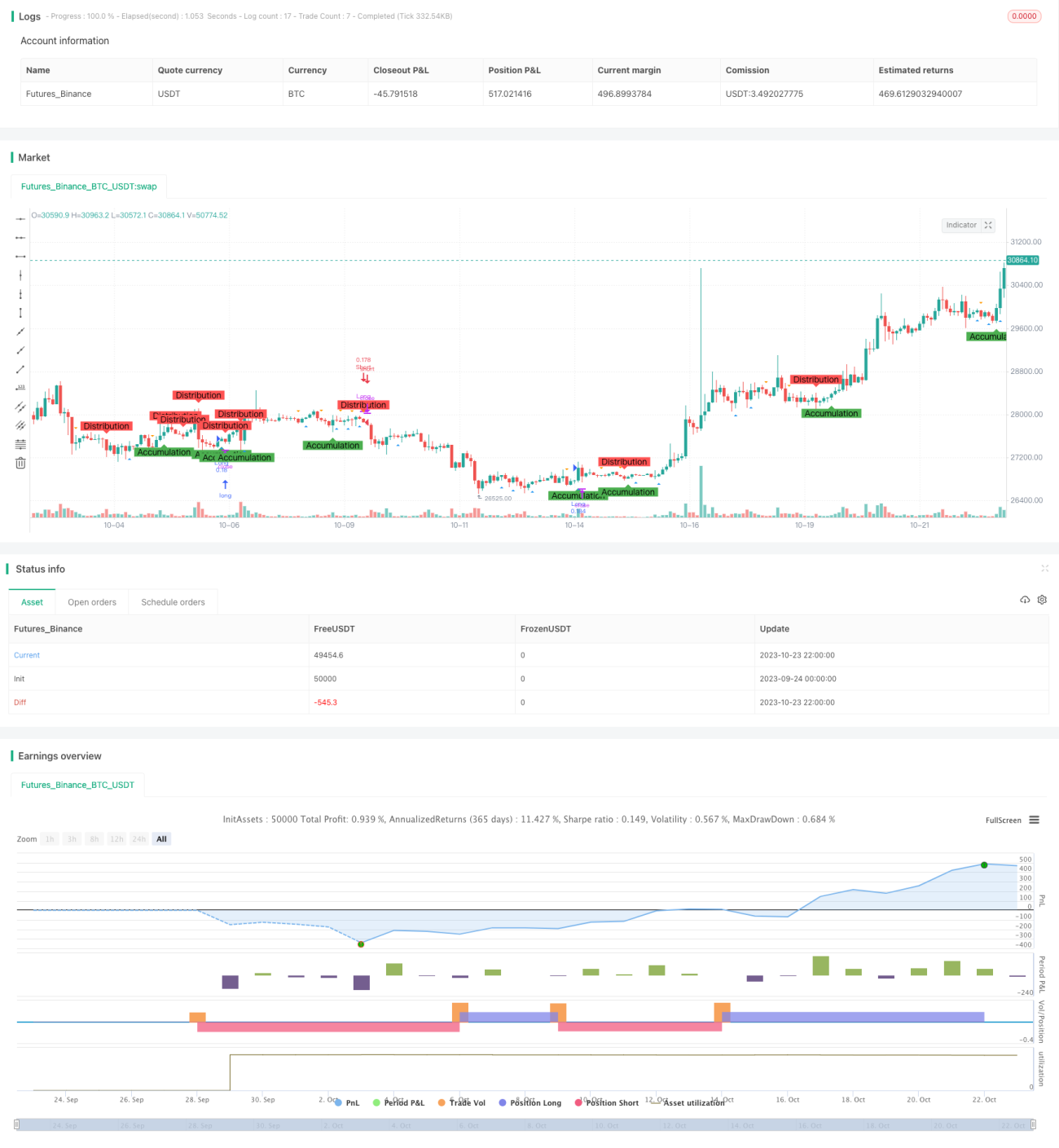

漸積突破取引戦略は、市場の漸積局面と分配局面を識別し、ビクター分析の原理を採用し、スリングショットパターンと反転パターンの判断を補助として、潜在的な買いと売りの機会を探します。

戦略の原理

-

異なる長さの移動平均線のクロスを使用して、漸積局面と分配局面を識別します。終値がAccumulationLengthの移動平均線を上抜けた場合、漸積局面と判断します。終値がDistributionLengthの移動平均線を下抜けた場合、分配局面と判断します。

-

異なる長さの移動平均線のクロスを使用して、スリングショットパターンと反転パターンを識別します。安値がSpringLengthの移動平均線を上抜けた場合、スリングショットパターンと判断します。高値がUpthrustLengthの移動平均線を下抜けた場合、反転パターンと判断します。

-

漸積局面でスリングショットパターンが観測された場合にロングし、分配局面で反転パターンが観測された場合にショートします。

-

ストップロス水準を設定します。ロングポジションのストップロス価格は終値×(1 - ストップロス%)、ショートポジションのストップロス価格は終値×(1 + ストップロス%)とします。

-

チャート上に漸積局面、分配局面、スリングショットパターン、反転パターンをマークし、パターン識別を容易にします。

優位性分析

-

ビクター分析手法を使用して市場のエネルギー蓄積の漸積局面と分配局面を識別することで、取引シグナルの信頼性を高めることができます。

-

スリングショットパターンと反転パターンを組み合わせて取引することで、取引シグナルをさらに検証できます。

-

ストップロスを設定することで、1回の損失を効果的に管理できます。

-

チャート上にマークを付けることで、エネルギー蓄積の全過程を明確に観察できます。

-

本戦略のパラメータは調整可能であり、異なる市場や取引時間帯に最適化できます。

リスク分析

-

相場の合流により、移動平均線のシグナルが誤ったシグナルを発する可能性があります。

-

スリングショットパターンや反転パターンが無効になる可能性があります。

-

ストップロスが突破されると損失が拡大する可能性があります。

-

異なる市場に合わせてパラメータを調整する必要があり、適切でない場合、取引シグナルが誤る可能性があります。

-

機械的な取引システムはバックテスト期間の柔軟性に欠ける可能性があり、人間による監視が必要です。

最適化の方向性

-

異なる市場や時間枠におけるパラメータの最適な組み合わせをテストできます。

-

出来高の要素を追加して取引シグナルを確認することを検討できます。

-

動的なストップロスを設定し、市場の変動に応じてストップロス水準を調整できます。

-

ファンダメンタル要因を組み込んで、重要なタイミングでの誤取引を回避することを検討できます。

-

機械学習アルゴリズムを導入して、パラメータを動的に最適化できます。

まとめ

漸積突破取引戦略は、ビクター分析、移動平均線指標、パターン認識など複数のテクニカル分析手法を統合し、市場のエネルギー蓄積を効果的に識別し、取引シグナルを生成します。本戦略は、信頼性の高い取引シグナル、管理可能なリスク、明確な視覚的表示などの利点を持ちます。ただし、機械的な取引システムとして、そのバックテスト期間やパラメータ適応性には改善の余地があります。今後の最適化の方向性としては、パラメータ組み合わせの最適化、出来高による確認、ストップロスの最適化、重要なファンダメンタル要因の組み込みなどが挙げられます。総じて、本戦略は日中短期取引に有効な意思決定支援を提供します。

- 1