高速・低速二重移動平均線取引戦略

概要

ダブル移動平均線トレーディング戦略は、短期移動平均線と長期移動平均線を計算し、その2本の移動平均線のクロス状況に基づいて取引シグナルを生成します。短期移動平均線が長期移動平均線を上抜けた場合にはロング戦略をとり、短期移動平均線が長期移動平均線を下抜けた場合にはショート戦略をとります。この戦略はトレンドフォロー戦略としても、逆張り戦略としても使用できます。

戦略の原理

この戦略はまず、短期移動平均線の長さmaFastLengthと長期移動平均線の長さmaSlowLengthを設定します。その後、短期移動平均線fastMAと長期移動平均線slowMAを計算します。短期移動平均線は価格変動に敏感に反応するため、現在のトレンドを判断するために使用されます。長期移動平均線は価格変動に鈍感で、トレンドの方向性を判断するために使用されます。

短期移動平均線が長期移動平均線を上抜けた場合には、ロング戦略をとり、goLong()シグナルを生成します。短期移動平均線が長期移動平均線を下抜けた場合には、ロングポジションを決済し、killLong()シグナルを生成します。

ロングのみの戦略(longonly)、ショートのみの戦略(shorting)、または双方向取引(swapping)を選択できます。

ロング戦略の場合、goLong()シグナルが発生したときにロングポジションを建て、killLong()シグナルが発生したときに決済します。

ショート戦略の場合、killLong()シグナルが発生したときにショートポジションを建て、goLong()シグナルが発生したときに決済します。

双方向取引の場合、goLong()シグナルが発生したときにロングポジションを建て、killLong()シグナルが発生したときにロングポジションを決済し、同時にショートポジションを建てます。

さらに、この戦略にはストップロス、トレーリングストップ、取引メッセージ通知などの機能が含まれており、使用の有無を柔軟に選択できます。

戦略の利点

- 戦略はシンプルで理解しやすく、実装が容易です。

- ロング、ショート、または双方向取引を自由に選択できます。

- ストップロスやトレーリングストップなどのリスク管理機能の使用有無を柔軟に選択できます。

- 取引メッセージをカスタマイズし、取引行動をリアルタイムで通知できます。

- 短期・長期の移動平均線戦略は市場トレンドの変化に敏感で、強いトレンドを捉えることができます。

- 戦略パラメータは調整可能で、異なる市場に合わせてパラメータを調整でき、適応性が高いです。

戦略のリスク

- 市場に明確なトレンドがない場合、多くの偽シグナルが発生し、過剰取引を引き起こす可能性があります。

- 移動平均線システムは突発的な出来事に鈍感であり、突発的な機会を逃す可能性があります。

- 移動平均線のパラメータを適切に選択する必要があり、パラメータの選択を誤ると戦略の効果に影響を与える可能性があります。

- 戦略シグナルに厳密に従う必要があり、自由裁量による取引を避ける必要があります。

- 取引コストが戦略の収益性に与える影響に注意する必要があります。

戦略の最適化方向

- 他の指標(例:RSI)を導入して取引シグナルを検証し、誤ったシグナルの発生を防ぐことができます。

- パラメータ最適化機能を設定し、最適なパラメータの組み合わせを自動的に探索することができます。

- 動的ストップロスを設定して利益を確定し、適宜ストップロスポイントを調整することができます。

- 機械学習モデルを追加して、トレンド方向の判断を補助することができます。

- メッセージ通知機能を最適化し、自身の取引習慣にさらに適合させることができます。

まとめ

ダブル移動平均線トレーディング戦略は全体的にシンプルで実用的であり、市場トレンドの変化に敏感で、強いトレンドによる取引機会を捉えることができます。ただし、トレンドのない市場での誤った取引を防ぎ、さまざまな市場環境に適応するためにパラメータを適切に調整する必要があります。また、補助的なテクニカル指標や最適化機能を適宜追加することで、戦略の安定性と適応性をさらに向上させることができます。

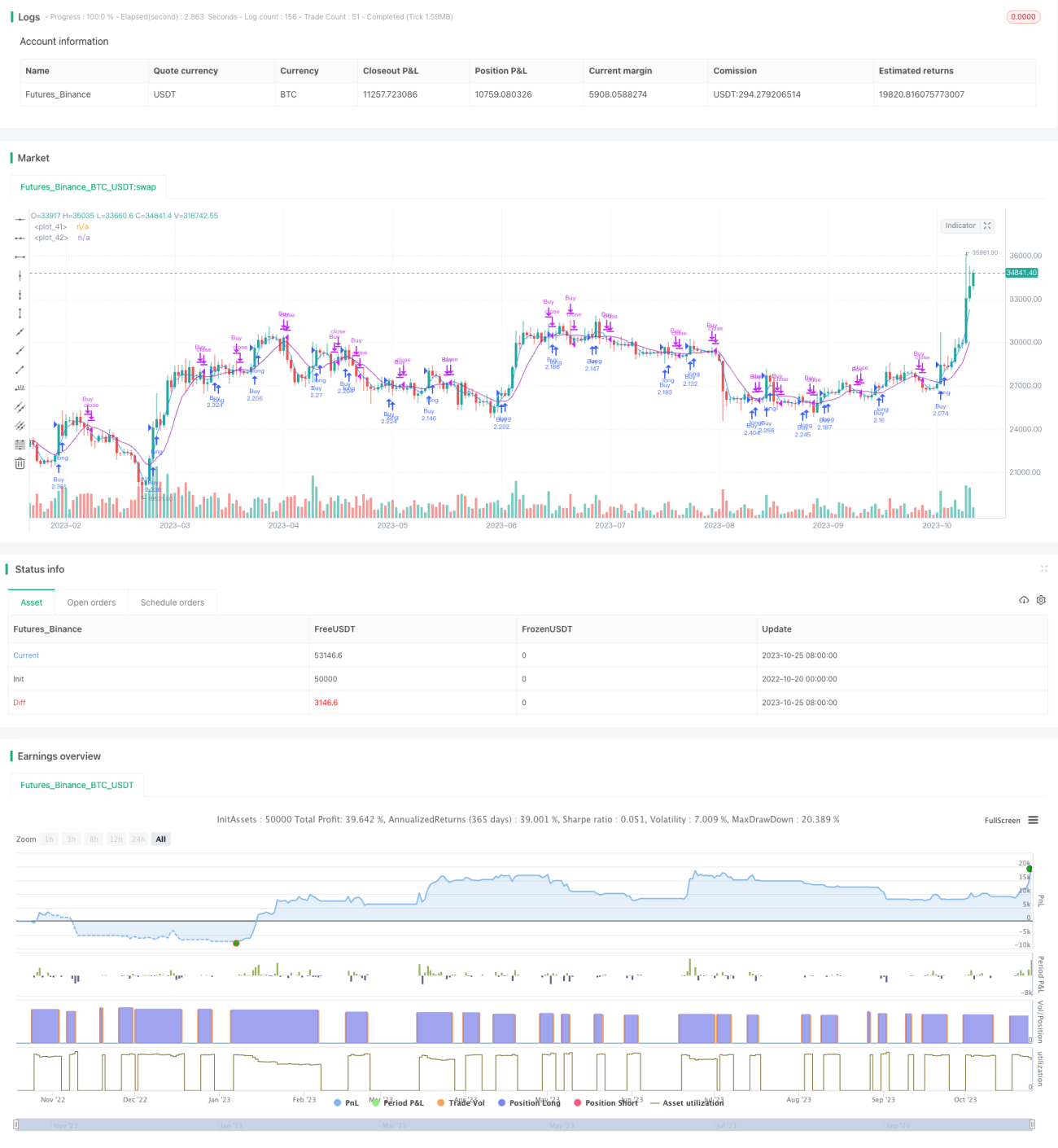

/*backtest

start: 2022-10-20 00:00:00

end: 2023-10-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SMA Strategy", shorttitle="SMA Strategy", overlay=true, pyramiding=0, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

- 1