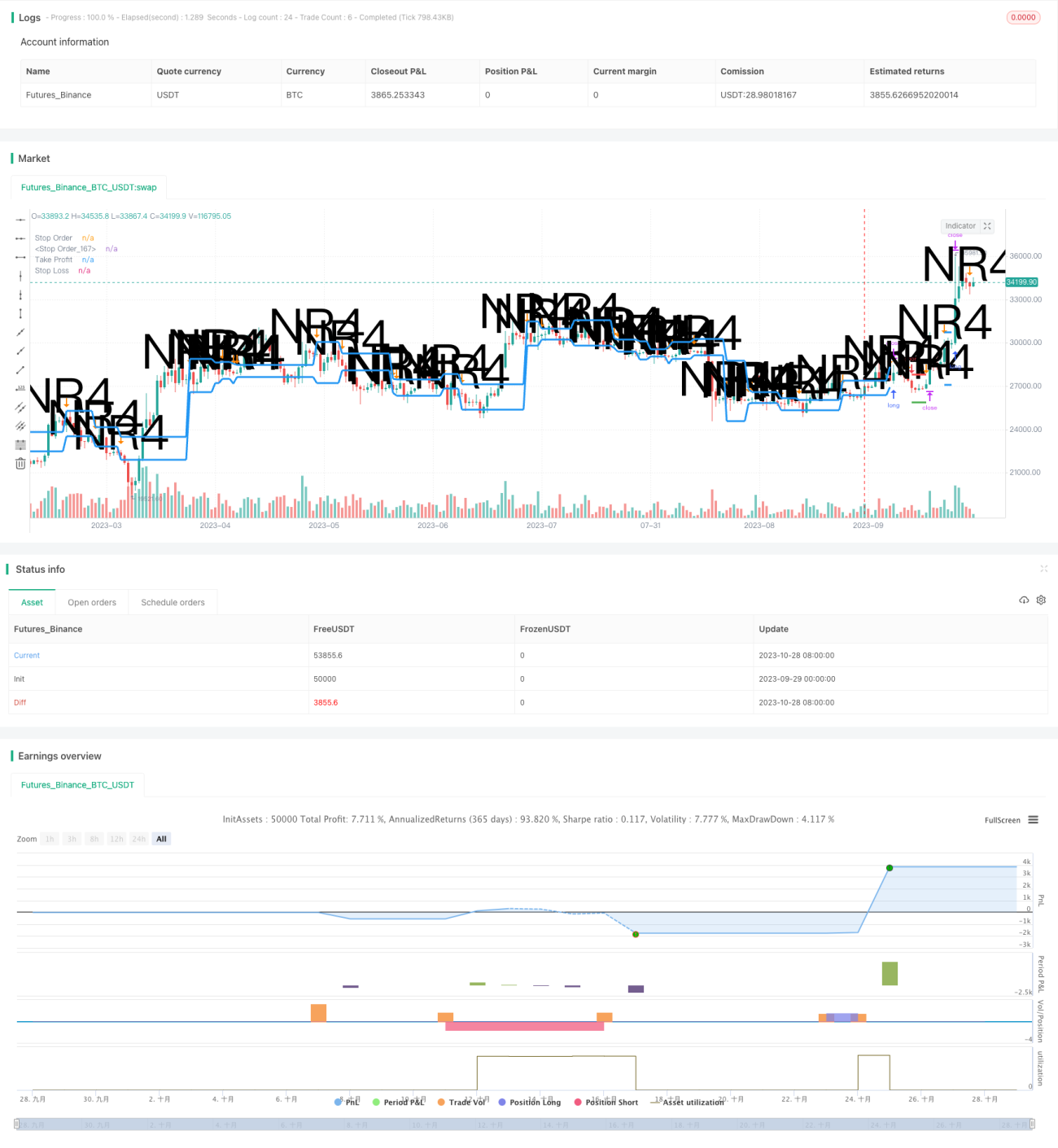

概要

休眠レンジ逆転戦略は、価格ボラティリティが低下する期間をポジション構築のシグナルとして利用し、ボラティリティが再び上昇した際に利益確定を行います。価格が狭いレンジ内に制限されている休眠レンジを識別することで、まもなく勃発する価格トレンドを捉えます。この戦略は通常、現在のボラティリティが低水準であるが、将来的に爆発の可能性がある場合に適用されます。

戦略の原理

この戦略はまず休眠レンジ、すなわち価格が前営業日の価格範囲内に制限されている状況を識別します。これは現在のボラティリティが数日前に比べて低下していることを示します。現在の営業日の最高値をn日前(通常は4日)の最高値と比較し、現在の営業日の最安値をn日前の最安値と比較することで、休眠レンジの条件を満たすかどうかを判断します。

休眠レンジが確認されると、この戦略は同時に2つの注文を出します。範囲の高値付近に買い注文、範囲の安値付近に売り注文です。その後、価格が休眠レンジを突破して上昇または下落するのを待ちます。価格が上方に突破すれば買い注文が執行されてロングポジションが構築され、下方に突破すれば売り注文が執行されてショートポジションが構築されます。

ポジション構築後、戦略はストップロス注文とテイクプロフィット注文を設定します。ストップロスは下振れリスクを制限し、テイクプロフィットは利益確定のために使用されます。ストップロスの価格はエントリー価格から一定の比率(リスク管理パラメータで設定)の距離に置かれ、テイクプロフィットの価格はエントリー価格から休眠レンジのサイズ分離れた場所に置かれます。これは、価格の動きの幅が以前のボラティリティと同等になると予想されるためです。

最後に、この戦略には資金管理モジュールも含まれています。固定倍率法を用いて注文の取引資金量を調整し、利益が出ているときは資金利用率を高め、損失が出ているときはリスクを低減します。

優位性分析

この戦略には以下のような利点があります。

-

ボラティリティが低下するタイミングをポジション構築のシグナルとすることで、価格トレンドが発生する前に機会を捉えられます。

-

同時にロング・ショート双方向の取引注文を設定することで、上昇トレンドまたは下降トレンドのいずれも捉えられます。

-

ストップロスとテイクプロフィット戦略を採用することで、一回の取引リスクを効果的にコントロールできます。

-

固定倍率資金管理法を適用することで、資金効率を高められます。

-

戦略ロジックは単純明快で実施が容易です。

リスク分析

この戦略には注意すべきリスクもいくつか存在します。

-

休眠レンジのブレイク方向を誤るリスク。価格が上下どちらにも明確にブレイクせず、エントリー方向を誤る可能性があります。

-

ブレイク後も方向性を持続できないリスク。ブレイクが単なる短期的な反転現象に終わる可能性があります。

-

ストップロスが突破されるリスク。非常に大きな相場変動が発生すると、ストップロスラインを直接突破する可能性があります。

-

固定倍率法によるポジション増加で損失が拡大するリスク。固定倍率の値を下げることでリスクを低減できます。

-

パラメータ設定が不適切だと戦略の効果が低下する可能性があります。

最適化の方向性

この戦略は以下の点からさらに最適化できます。

-

ブレイク時のダイバージェンスなどのフィルターシグナルを追加し、誤ったブレイクを回避します。

-

ストップロス戦略の改善(トレーリングストップ、指値ストップロスなど)。

-

トレンド判断指標を追加し、逆張りエントリーを回避します。

-

固定倍率の値を最適化し、損益比率のバランスをとります。

-

複数の時間足分析を組み合わせ、利益獲得確率を高めます。

-

機械学習手法を利用してパラメータを自動最適化します。

まとめ

休眠レンジ逆転戦略は全体的な考え方が明確で、一定の利益獲得の可能性があります。パラメータ最適化、リスク管理、シグナルフィルタリングなどの手段により、戦略の安定性をさらに向上させることができます。しかし、いかなるトレンド逆転戦略にも一定のリスクが伴うため、慎重に使用し、ポジションサイズを適切に調整する必要があります。この戦略は、逆転操作に精通し、リスク認識のあるトレーダーに適しています。

- 1