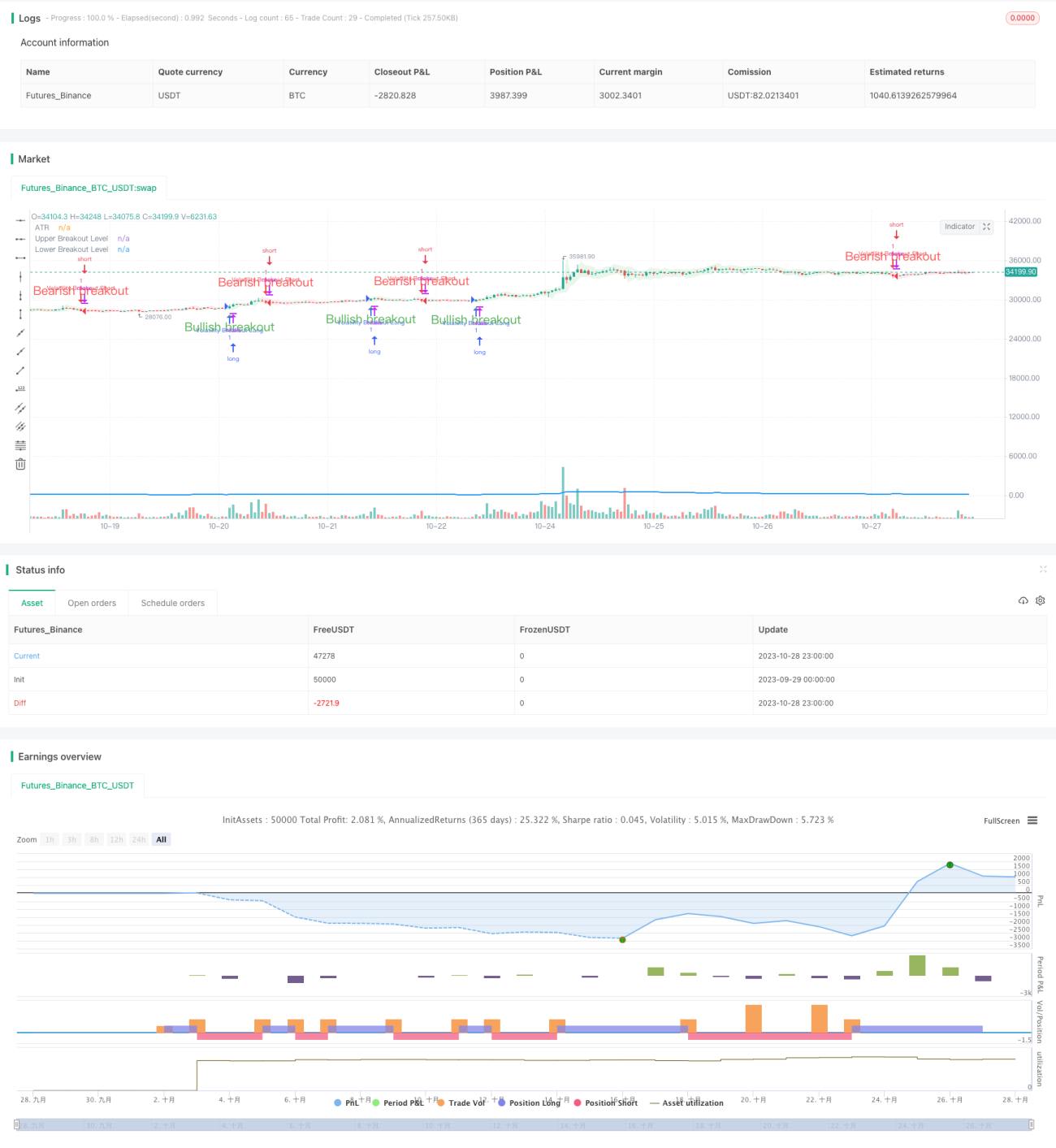

概要

ブレイクアウト戦略は、市場のボラティリティの増加によって引き起こされる価格のブレイクアウトを捉えることを目的としています。この戦略では、平均真値範囲(ATR)指標を使用して、特定の期間における資産のボラティリティを測定します。価格がATRによって決定される上下2本のブレイクラインを突破すると、ロングシグナルおよびショートシグナルが発生します。

戦略の原理

この戦略はまず、指定された期間のATRを計算します。次に、ATRに基づいて上限バンドと下限バンドを計算します。終値が上限バンドを上回った場合にロングシグナルが発生し、終値が下限バンドを下回った場合にショートシグナルが発生します。シグナルをさらに確定させるために、現在のローソク足の実体部分が閉じている必要があります。

終値が上限バンドと下限バンドを突破した場合、突破方向にギャップの色が塗られます。この特徴により、現在のトレンド方向を迅速に識別することができます。

ロングシグナルが発生し、現在ポジションがない場合、戦略はロングでエントリーします。ショートシグナルが発生し、現在ポジションがない場合、戦略はショートでエントリーします。

Lengthパラメータは、ボラティリティを測定する期間の長さを決定します。Lengthの値が大きいほど、より長い価格変動に注目します。例えば、Lengthが20の場合、各トレードは約100本のローソク足にまたがり、複数の変動を含みます。

Lengthの値を小さくすると、より短期的な価格変動に注目し、取引頻度が増加します。Lengthの値と平均取引長さの間に厳密な対応関係はなく、試行錯誤を通じて最適なLength値を見つける必要があります。

優位性分析

この戦略はブレイクアウトの原理を利用しており、市場の変動によってもたらされる大きな行情を捉えることができます。ATR指標は動的にブレイクアウトラインを計算するため、固定パラメータの使用を避けられます。

実体ローソク足によるシグナル確認により、偽のブレイクアウトをフィルタリングできます。ブレイクアウトギャップの色塗りにより、トレンド方向が視覚的に表示されます。

Lengthパラメータは戦略調整の柔軟性を提供し、特定の市場に合わせてパラメータを最適化できます。

リスク分析

ブレイクアウト取引には、だまし取引(フェイクアウト)のリスクがあります。ストップロスを設定することで、1回の損失をコントロールできます。

ブレイクアウトシグナルが誤報となり、超短期トレードを引き起こす可能性があります。適切にLengthパラメータを調整することで、誤報をフィルタリングできます。

パラメータの最適化には十分な取引データの蓄積が必要です。初期のパラメータ選択が不適切な場合、取引パフォーマンスが低下する可能性があります。

最適化の方向性

ATR期間にボリンジャーバンドを導入し、新たなブレイクアウトラインの計算方法とすることができます。ボリンジャーバンドのブレイクアウトは誤報率を低下させることができます。

ブレイクアウト後、即座にストップロスせずにトレンドを追跡し続けることができます。例えば、トレンドフォロー型のストップロスを追加します。

レンジ相場では異なるパラメータを使用するか、まったく取引をしないことで、だまし取引を回避することを検討できます。

まとめ

ブレイクアウト戦略は市場のボラティリティを利用し、価格が大きなブレイクアウトを起こした際にトレンドに乗ります。ATR指標が動的にブレイクアウトラインを決定し、実体ローソク足が偽のブレイクアウトをフィルタリングします。Lengthパラメータは戦略期間の調整に柔軟性を提供します。この戦略は中長期トレンドの追跡に適していますが、ブレイクアウト取引のリスクに注意し、パラメータ最適化を行う必要があります。

/*backtest

start: 2023-09-29 00:00:00

end: 2023-10-29 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

strategy("Volatility Breakout Strategy [Angel Algo]", overlay = true)- 1