概要

ライオンクラック均衡戦略は、移動平均線のクロスをベースにしたシンプルな短期トレード戦略です。この戦略は主に2本の移動平均線を使用し、短期移動平均線が長期移動平均線を下から上にクロスしたときにロング、長期移動平均線を上から下にクロスしたときにポジションをクローズします。戦略名はトレード界で人気のある「ライオンクラック」という用語に由来し、短期間の価格の微細な動きを捉え、狭い移動平均線の隙間で利益を得ることを意味します。

戦略原理

この戦略では、2本の移動平均線(短期移動平均線:smallMAPeriod、長期移動平均線:bigMAPeriod)を使用します。2本の移動平均線が価格チャネルを形成し、チャネルの下限が短期移動平均線、上限が長期移動平均線となります。価格が下から上にチャネル下限(短期移動平均線)をブレイクしたときにロング、上から下にチャネル上限(長期移動平均線)を割り込んだときにポジションをクローズします。

具体的には、まず短期移動平均線smallMAと長期移動平均線bigMAを計算します。次に、チャネル下限である買い線buyMAを計算します。これは長期移動平均線の(100 - percentBelowToBuy)%です。短期移動平均線smallMAが下から上に買い線buyMAをクロスしたときにロングエントリーし、利益が1%に達した場合、または利益に達していないが7本のローソク足をホールドした場合にポジションをクローズします。

以上より、この戦略は移動平均線の「ライオンクラック」、すなわちチャネル下限突破の機会を捉え、短期利益を狙います。同時に利確・損切条件を設定し、1トレードあたりのリスクをコントロールします。

優位性分析

この戦略には以下のような利点があります。

- コンセプトがシンプルで理解・実装が容易。ダブル移動平均線クロスは最も基本的なテクニカル指標戦略です。

- バックテストが簡単。TradingView標準のバックテスト機能を直接使用でき、追加実装は不要です。

- 可視化に優れている。TradingView上で直接チャートにシグナルポイントやバックテストの統計データを表示できます。

- リスク管理が可能。利確・損切条件を設定することで、1トレードあたりの損失を効果的にコントロールできます。

- 柔軟な調整が可能。ユーザーは自分のニーズに合わせて移動平均線のパラメータや他のテクニカル指標を調整し、異なる銘柄やトレードスタイルに適応できます。

リスク分析

この戦略には以下のリスクも存在します。

- シグナルが多発する可能性。ダブル移動平均線戦略はレンジ相場で誤ったシグナルを複数回発生させやすい。

- 単一指標への依存。移動平均線クロスのみで判断し、他の要素を無視するため、シグナル品質が低い可能性がある。

- パラメータ最適化が困難。移動平均線の期間パラメータの組み合わせ最適化には多くの計算が必要で、最適パラメータを見つけにくい。

- バックテストのバイアス。シンプルなダブル移動平均線戦略のバックテスト結果は、実運用を上回ることが多い。

- 損切の難しさ。固定の損切ラインでは相場の変動に対応しにくい。

最適化の方向性

この戦略は以下の観点から最適化が可能です。

- 他の指標(出来高、ボラティリティなど)を組み合わせてシグナルをフィルタリングし、レンジの中での無効なシグナルを回避する。

- トレンドに基づく判断を追加し、逆張りを避ける。より長い期間の移動平均線を追加してトレンド方向を判断する。

- 機械学習を用いた最適パラメータの探索。逐次パラメータ最適化や遺伝的アルゴリズムにより自動的に優れたパラメータ組み合わせを見つける。

- トレーリングストップ、移動ストップなどの損切戦略を追加し、損切をより柔軟にする。

- エントリータイミングの最適化。他の指標を使ってより有効なエントリーポイントを特定する。

- 定量リサーチを用いてパラメータ組み合わせのバックテスト最適化を行い、安定性を高める。

- 自動売買システムを開発し、プログラムトレードによるパラメータ最適化と戦略評価を実現する。

まとめ

ライオンクラック均衡戦略は、初心者が学ぶのに非常に適した入門戦略です。シンプルなダブル移動平均線クロスの原理を利用し、利確・損切ルールを設定することで、短期的な価格変動を捉えることができます。この戦略は理解・実装が容易で、バックテストの効果も良好です。しかし、最適化の難易度は高く、実運用の効果には疑問が残ります。他のテクニカル指標の導入、パラメータの最適化、自動売買システムの開発などを通じて、この戦略を改善することが可能です。総じて、ライオンクラック均衡戦略は、定量トレードの初心者にとって非常に優れた学習プラットフォームを提供します。

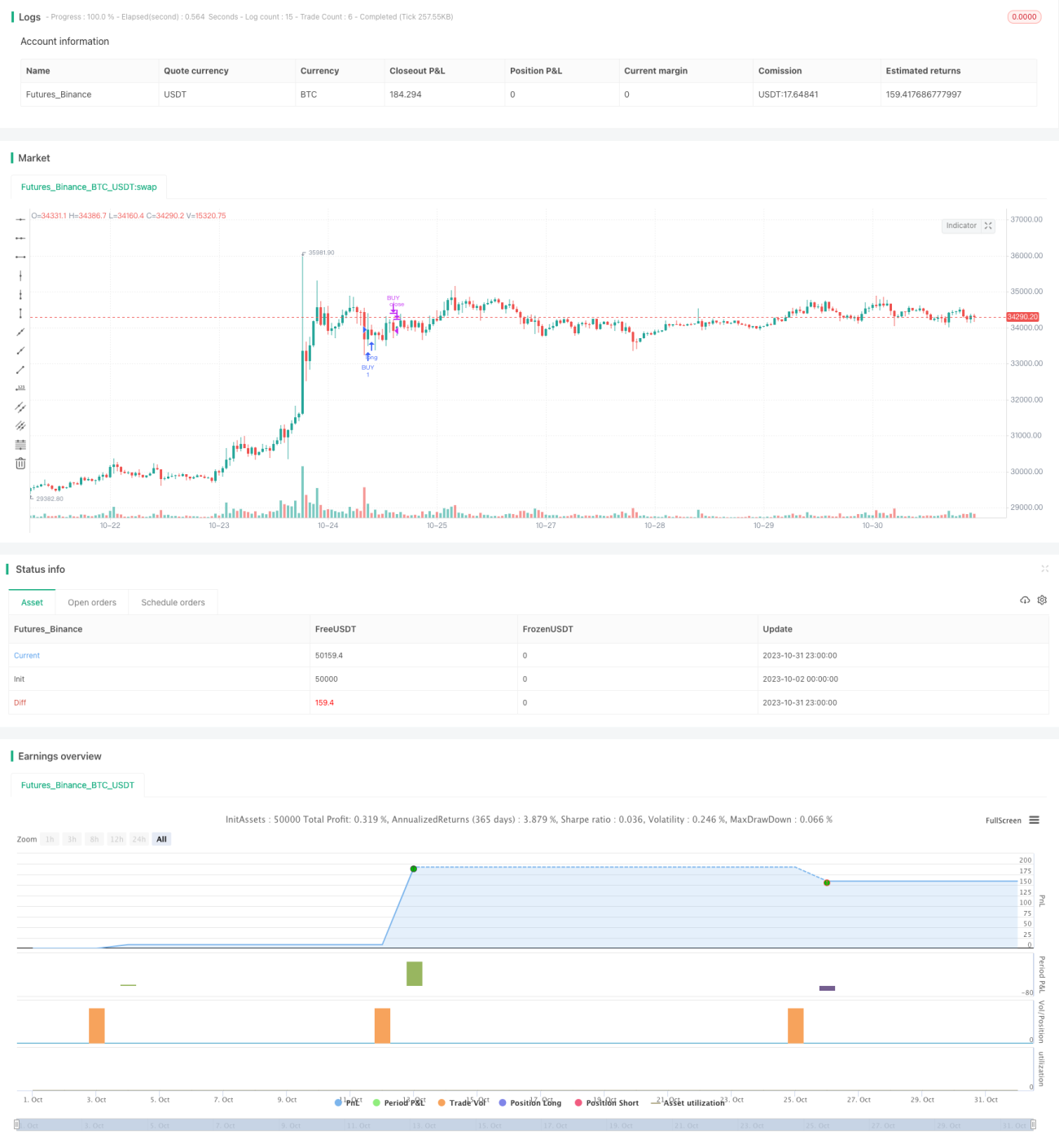

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TraderHalai

// This script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

//- 1