漸進的要素加重DCA定量取引戦略

概要

プログレッシブ要素加重DCA定量取引戦略は、移動平均線指標によるトリガーシグナルとプログレッシブ加重ドルコスト平均法(DCA)メカニズムを組み合わせた定量取引戦略です。この戦略は、トレンド判断とコスト平均化を通じて、トレンド方向性の強い市場で安定した収益を得ることを目的としています。

原理

本戦略は主に以下の3つの部分で構成されています。

-

エントリーシグナルの判断

短期移動平均線と長期移動平均線のクロスをエントリーシグナルとして使用します。ユーザーの設定に応じて、SMA、EMA、またはHMAを短期・長期の移動平均線として選択できます。短期線が長期線を下から上に抜けた場合、買いシグナルが発生します。短期線が上から下に長期線を割り込んだ場合、売りシグナルが発生します。

-

プログレッシブ加重DCA

買いシグナルがトリガーされた後、戦略は直ちにポジションを開き、ベースポジションを構築します。その後、価格がさらに下落した場合、戦略はプログレッシブ加重方式で後続の安全ポジションを追加します。新たな安全ポジションの価格は、直前の安全ポジションの価格から一定幅ずつ引き下げられます。同時に、新たな安全ポジションの資金量も順次拡大されます。

このように段階的にポジションを追加することで、ある程度のコスト平均化が実現され、取引リスクを管理可能に保ちながら、より有利なコスト価格を得ることができます。

-

利益確定と損切り

価格が上昇して利益確定ラインを突破した場合、戦略は利益確定を選択します。価格が下落して損切りラインを突破した場合、戦略は損切りを選択します。

利益確定ラインは、ベースポジションの平均約定価格に固定比率を加えたものに固定されます。

損切りラインは、最後の安全ポジションの価格に応じて変動します。最後の安全ポジションの約定価格から一定の下方比率に基づいて、損切りシグナルが確定されます。

優位性

-

トレンド判断とコスト平均化の組み合わせにより、戦略がより安定

トレンド判断により方向性のないレンジ相場を回避でき、コスト平均化によりトレンド中でより有利なコストを得られます。

-

段階的なポジション追加によりリスクを管理

各均等ポジションの規模には一定の幅があり、後続のポジションには一定のドローダウンが要求されるため、リスクを管理できます。

-

戦略の使用資金をリアルタイムで監視

コードにリアルタイム監視タグを追加することで、ユーザーは戦略の使用資金上限を明確に把握でき、過剰使用によるポジションの強制決済を回避できます。

-

各ポジションの利益確定・損切りが柔軟

ベースポジションと安全ポジションはそれぞれ利益確定・損切りが可能で、利益の確定とリスクの管理を両立できます。

リスクと最適化

-

激しい価格変動により複数回のポジション追加が発生する可能性

価格が激しく変動する場面では、複数回のポジション追加がトリガーされ、損失が拡大する可能性があります。後続の安全ポジション間のドローダウン要件を適切に拡大することで、追加回数を減らすことができます。

-

移動平均線パラメータの選択には最適化が必要

移動平均線のパラメータはエントリーのタイミングに直接影響を与えるため、異なる銘柄ごとに適切なパラメータをテストして決定する必要があります。

-

損切り・利益確定比率のテストと最適化が必要

損切り・利益確定比率は収益率とドローダウン管理に影響を与えるため、バックテストデータを通じて設定を最適化する必要があります。

-

ドローダウンや時間に基づく強制決済条件を追加可能

最大ドローダウンや保有時間がしきい値を超えた場合の強制決済条件をテストで追加し、さらにリスクをコントロールできます。

まとめ

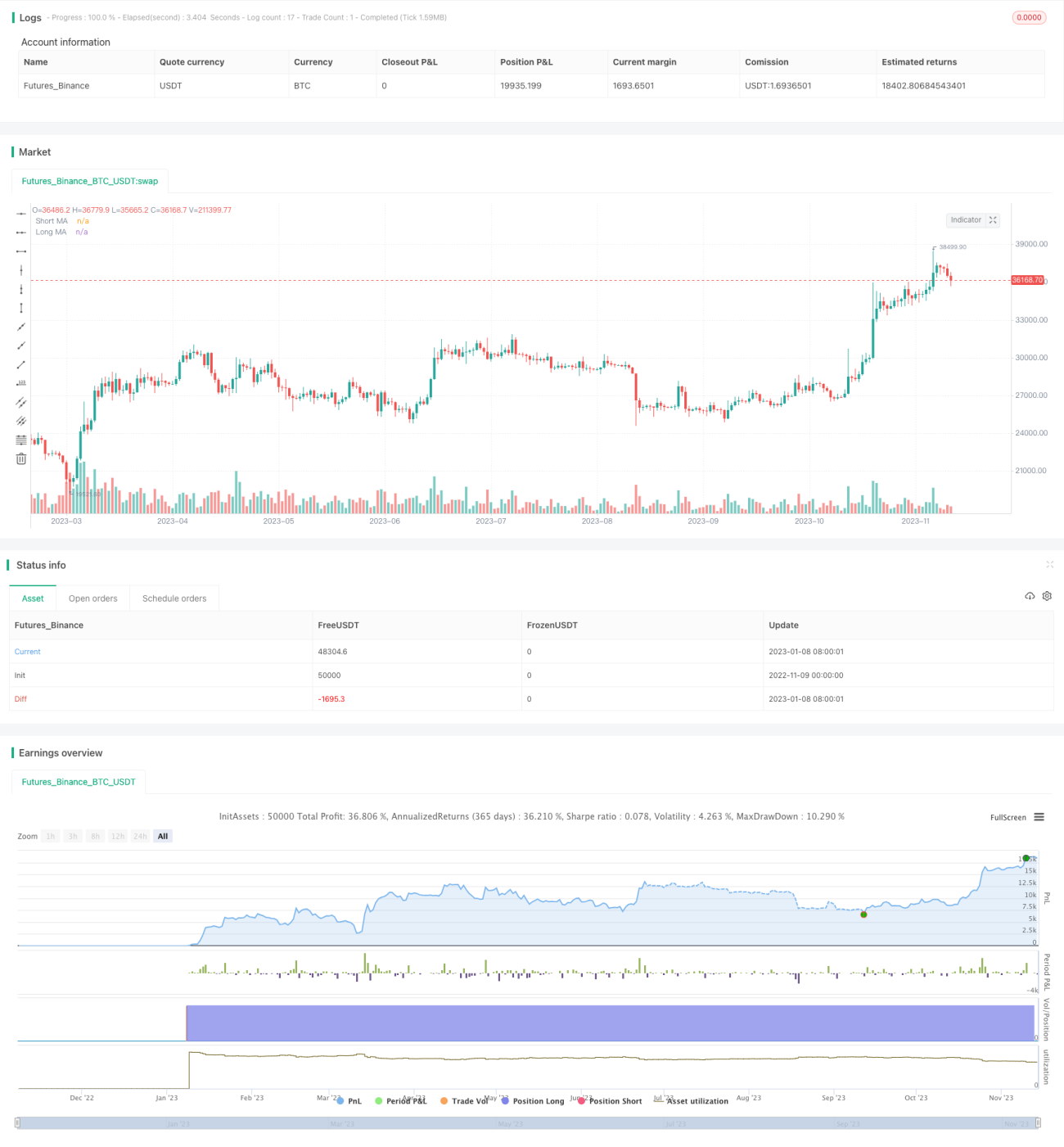

プログレッシブ要素加重DCA定量取引戦略は、トレンド判断とコスト平均化の利点を統合し、強いトレンド相場で安定した収益を得ることができます。パラメータ設定を最適化し、ポジションサイズやポジション間のドローダウン要件を調整することで、リスク管理された安定した取引を実現できます。本戦略は、ヘッジファンド、CTAファンド、および一部の対抗戦略の設計に適用可能です。

- 1