黄金分割によるレンジ相場戦略

1

Follow

1802

Followers

概要

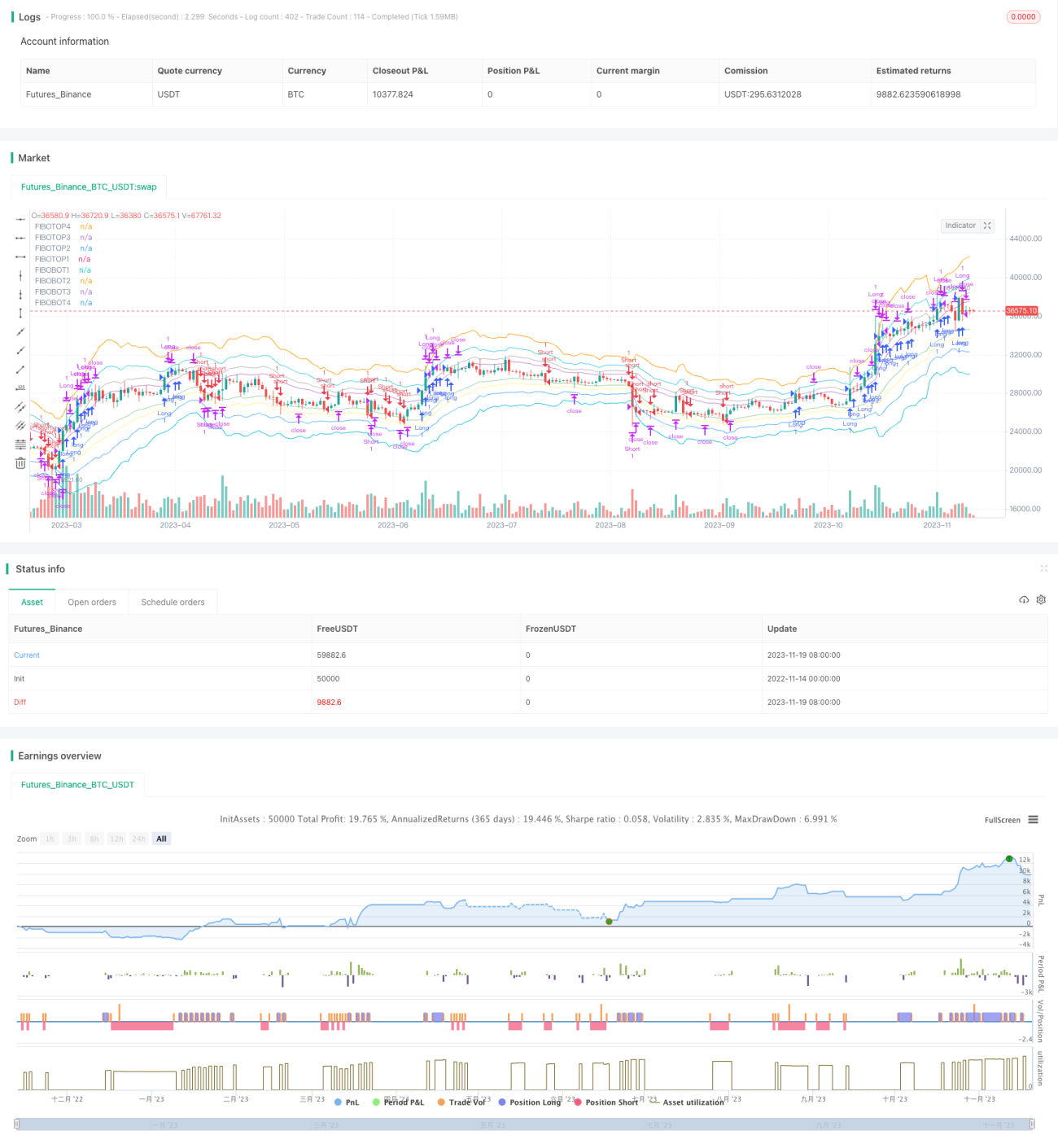

黄金分割バンド・レンジ戦略は、黄金分割理論に基づいて設計された定量戦略です。この戦略は主に黄金分割の法則を利用して複数の価格帯を計算し、上下のバンドを形成します。価格がバンドを突破したときに取引シグナルを発生させ、価格がバンド間で振動する特徴を捉えて利益を得ます。

戦略の原理

コードの核となるロジックは、黄金分割バンドをキーポイントとして計算することです。主な手順は以下の通りです。

- 14期間のEMAを中間軸として計算する。

- ATRと黄金分割比率に基づいて上下4本のバンドラインを計算する。

- 価格が下降バンドを上に突破、または上昇バンドを下に突破したときに取引シグナルを発生させる。

- ストップロスとテイクプロフィットを設定し、価格の振動を追跡して利益を得る。

このキーポイント突破に基づく方法により、市場の短期的な振動を効果的に捉え、バンド間で往復取引を行って利益を得ることができます。

戦略の優位性

この戦略の最大の利点は、黄金分割という重要な理論指標を利用してキー価格ポイントを特定し、利益を得る確率を高めることです。具体的な優位性は主に以下の通りです。

- 黄金分割バンドが明確で、突破口を判断しやすい。

- バンドの範囲が適切で、細かすぎず、広すぎない。

- 複数のバンドから選択可能で、攻撃的な取引も保守的な取引も可能。

- バンドの振動特性が明確で、短期売買戦略の効果が高い。

戦略のリスク

この戦略は短期的な利益を追求するため、注意すべきリスクも存在します。

- 大きなサイクルのトレンドでは利益を得られない。

- 価格が激しく変動する場合、ストップロスのリスクが大きい。

- 突破シグナルが多いため、慎重な選択が必要。

- バンドの振動特性が消失した場合には無効になる。

これらのリスクは、パラメータを適切に調整し、適切なバンドと資金管理方法を選択することで制御できます。

戦略の最適化

この戦略にはさらなる最適化の余地があります。

- トレンド指標を組み合わせて、特定のトレンド方向でのみシグナルを発生させる。

- 特定の時間帯や重要なイベントの前後で戦略を停止する。

- ストップロスの幅を動的に調整し、市場の変動頻度に適応させる。

- 異なる期間のEMAを基準中線として選択するパラメータを最適化する。

まとめ

黄金分割バンド・レンジ戦略は全体的に非常に実用的な短期戦略です。黄金分割理論を利用して価格のキーポイントを設定し、価格がこれらのポイント付近で振動する際に豊富な利益を得ることができます。このレンジ突破に基づく方法は、一定の変動性と特性を持つ市場に適しており、単独で使用することも、他の戦略と組み合わせることもできます。パラメータのチューニングと適切な資金管理により、この戦略は長期的に安定して運用できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1