モメンタム反転デュアルトラックペア戦略

1

Follow

1802

Followers

概要

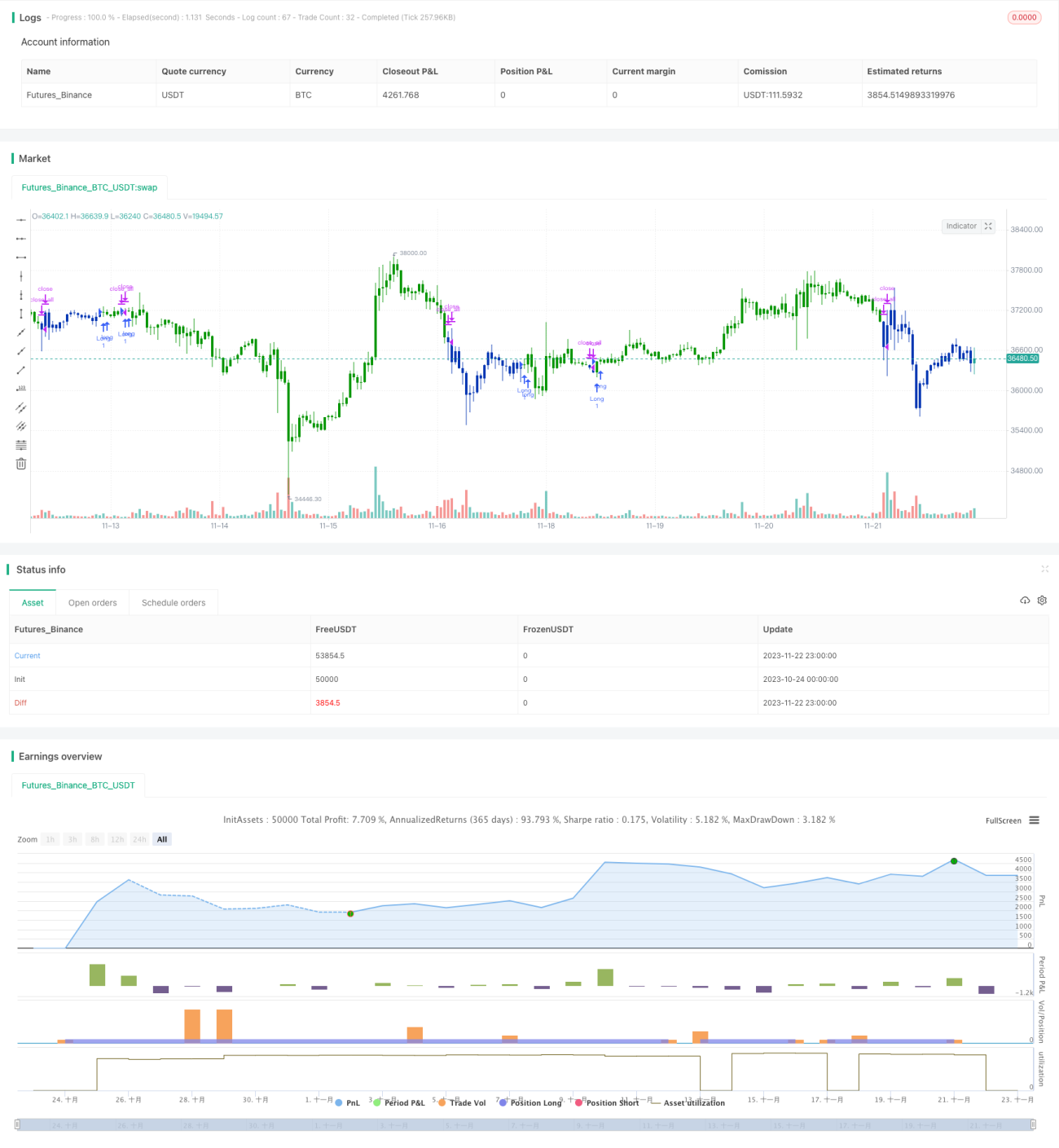

本戦略は複数のテクニカル指標を組み合わせ、モメンタム反転と二重軌道ペアリングを実現し、取引シグナルを生成します。戦略では123フォーメーションを使用して反転ポイントを判断し、ergodic CSIインジケーターとペアシグナルを形成することでトレンドフォローを行います。この戦略は中短期トレンドを捉え、高い収益性を目指します。

戦略の原理

本戦略は以下の2つの部分で構成されます。

- 123フォーメーションによる反転ポイントの判断

- ergodic CSIインジケーターによるペアシグナルの生成

123フォーメーションは、直近3本のローソク足の終値関係を用いて価格反転を判断します。具体的な判断ロジックは以下の通りです。

- 前2本のローソク足で後に終値が上昇し、かつ現在のFastおよびSlowストキャスティクスが両方とも50未満であれば買いシグナル。

- 前2本のローソク足で後に終値が下落し、かつ現在のFastおよびSlowストキャスティクスが両方とも50超であれば売りシグナル。

ergodic CSIインジケーターは価格、真のレンジ、トレンド指標などの複数の要素を考慮し、相場の動きを総合的に判断して買い・売りゾーンを生成します。

指標が買いゾーンを上回ると買いシグナル、売りゾーンを下回ると売りシグナルが発生します。

最後に、123フォーメーションの反転シグナルとergodic CSIの軌道シグナルをAND演算することで、最終的な戦略シグナルを得ます。

戦略のメリット

- 中短期トレンドを捉え、収益の可能性が高い

- 反転フォーメーションにより転換点を効果的に捉えられる

- 二重軌道ペアリングにより偽シグナルを低減できる

戦略のリスク

- 個別銘柄で相場が乖離し、損切りが発生する可能性がある

- 反転フォーメーションはレンジ相場の影響を受けやすい

- パラメータ最適化の余地が限られ、効果の変動が大きい

最適化の方向性

- パラメータの最適化により収益効果を向上

- 損切りロジックを追加し、1回あたりの損失を低減

- マルチファクターモデルを組み合わせ、銘柄選択の質を向上

まとめ

本戦略は反転フォーメーションと二重軌道ペアリングにより、中短期トレンドを効果的に追跡します。単一のテクニカル指標と比較して、より高い安定性と収益性を有します。次のステップでは、さらにパラメータを最適化し、損切りおよび銘柄選択モジュールを追加することで、ドローダウンを低減し、全体的な効果を高めます。

Source

Pine

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/07/2020

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1