移動平均加重標準偏差取引戦略

概要

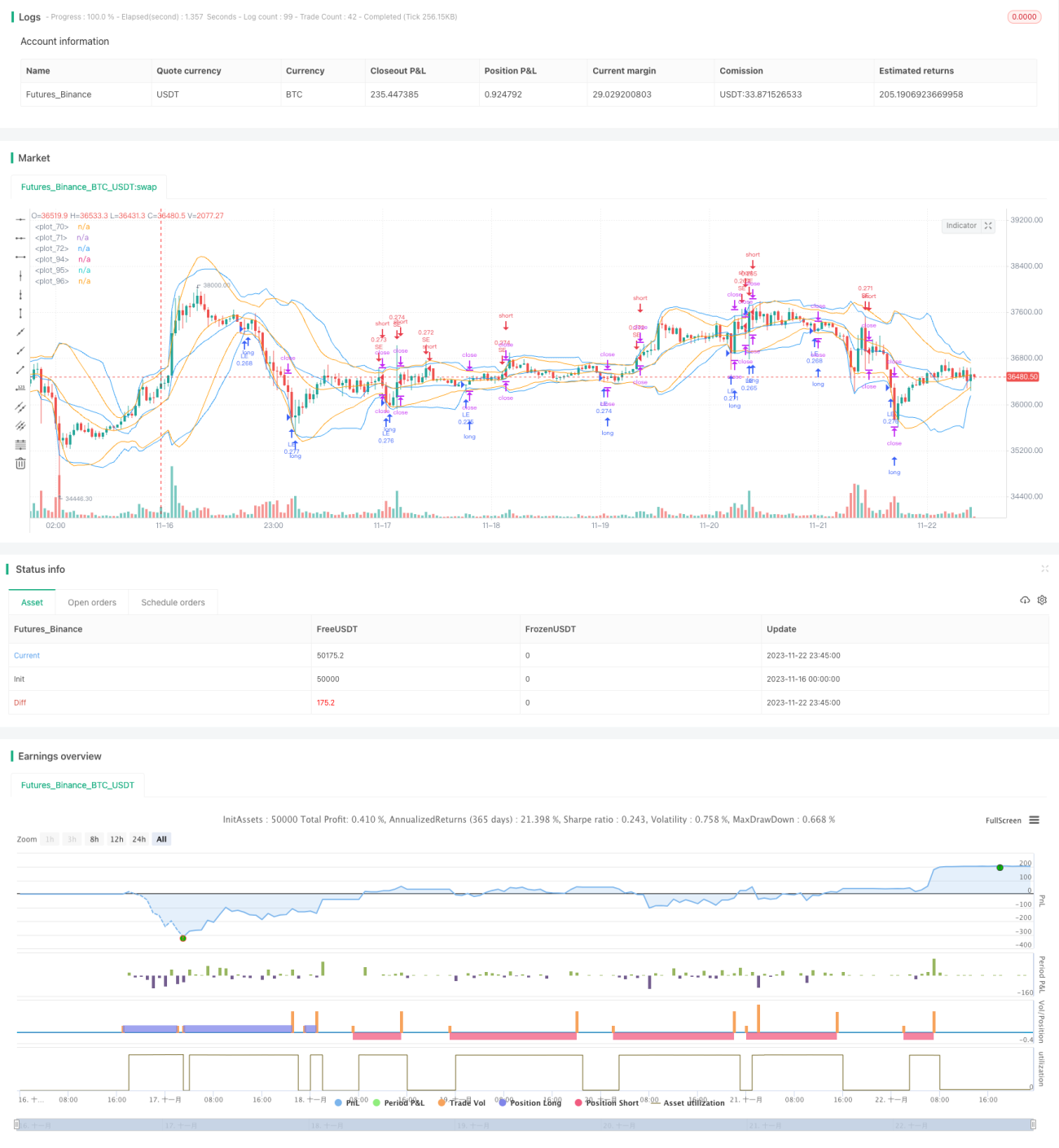

本戦略は加重標準偏差指標と移動平均線を組み合わせ、暗号通貨のトレンド取引を実現します。戦略は一定期間の終値と出来高に基づき、価格の加重標準偏差チャネルを算出します。価格がチャネルの上下バンドをブレイクした際にロングまたはショートを行います。同時に、損切り・利確条件を設定し、1回あたりの損失を抑制します。

戦略の原理

コード内では、時系列データと配列から加重標準偏差を計算する2つのカスタム関数が定義されています。主な手順は次のとおりです。

- 終値と出来高に基づき、加重平均価格を計算

- 各ローソク足と平均価格との誤差の二乗を計算

- サンプル数と重みで調整した平均値から分散を計算

- 平方根を取って標準偏差を求める

これにより、中心が加重平均価格、上下の距離が標準偏差1つ分のチャネルが得られます。価格が下からチャネル底部をブレイクした場合はロング、上からチャネル天井をブレイクした場合はショートとなります。

優位性分析

本戦略の最大の強みは、移動平均線とボラティリティ分析を融合している点です。移動平均線で市場トレンドの方向性を判断し、標準偏差で合理的な価格帯を定義するため、相互に検証でき信頼性が高いです。また、出来高の重み付けにより偽のブレイクをフィルタリングでき、実際のブレイク確率が向上します。

さらに、損切り・利確ポイントを設定しているため、トレンドを捉えやすく、反転による過大な損失を防げます。これは多くの初心者が習得できない重要なポイントです。

リスク分析

主なリスクは、市場が急激に変動した場合に標準偏差チャネルも大きく変動し、判断が難しくなることです。また、周期が短すぎるとノイズに影響されやすく、誤判定の確率が高まります。

対策としては、周期パラメータを適宜調整して曲線を平滑化することや、RSIなどの他のインジケーターを併用してブレイクの確認を強化することが考えられます。

最適化の方向性

- 周期パラメータの最適化:5分、15分、30分など異なる周期をテストし、最適な組み合わせを探す

- 損切り・利確比率の最適化:異なる損切り・利確ポイントをテストし、最大のリターン率を得る

- フィルター条件の追加:出来高などを組み合わせ、偽のブレイクによる損失を回避

- ローソク足指標の追加:終値の位置やヒゲの長さなどでローソク実体を確認し、誤判定を低減

まとめ

本戦略は加重標準偏差指標と移動平均線による方向性判断を組み合わせ、暗号通貨のトレンド追跡に成功しています。また、適切な損切り・利確設定により市場のリズムを掴みやすく、過度な反転による損失を防ぎます。パラメータ調整と複数インジケーターの検証により、さらに最適化し信頼性の高い定量取引戦略へと発展させることができます。

/*backtest

start: 2023-11-16 00:00:00

end: 2023-11-23 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © rumpypumpydumpy © cache_that_pass

//@version=4- 1