ウェーブトレンド・マルチストップロス・マルチテイクプロフィット戦略

1

Follow

1802

Followers

概要

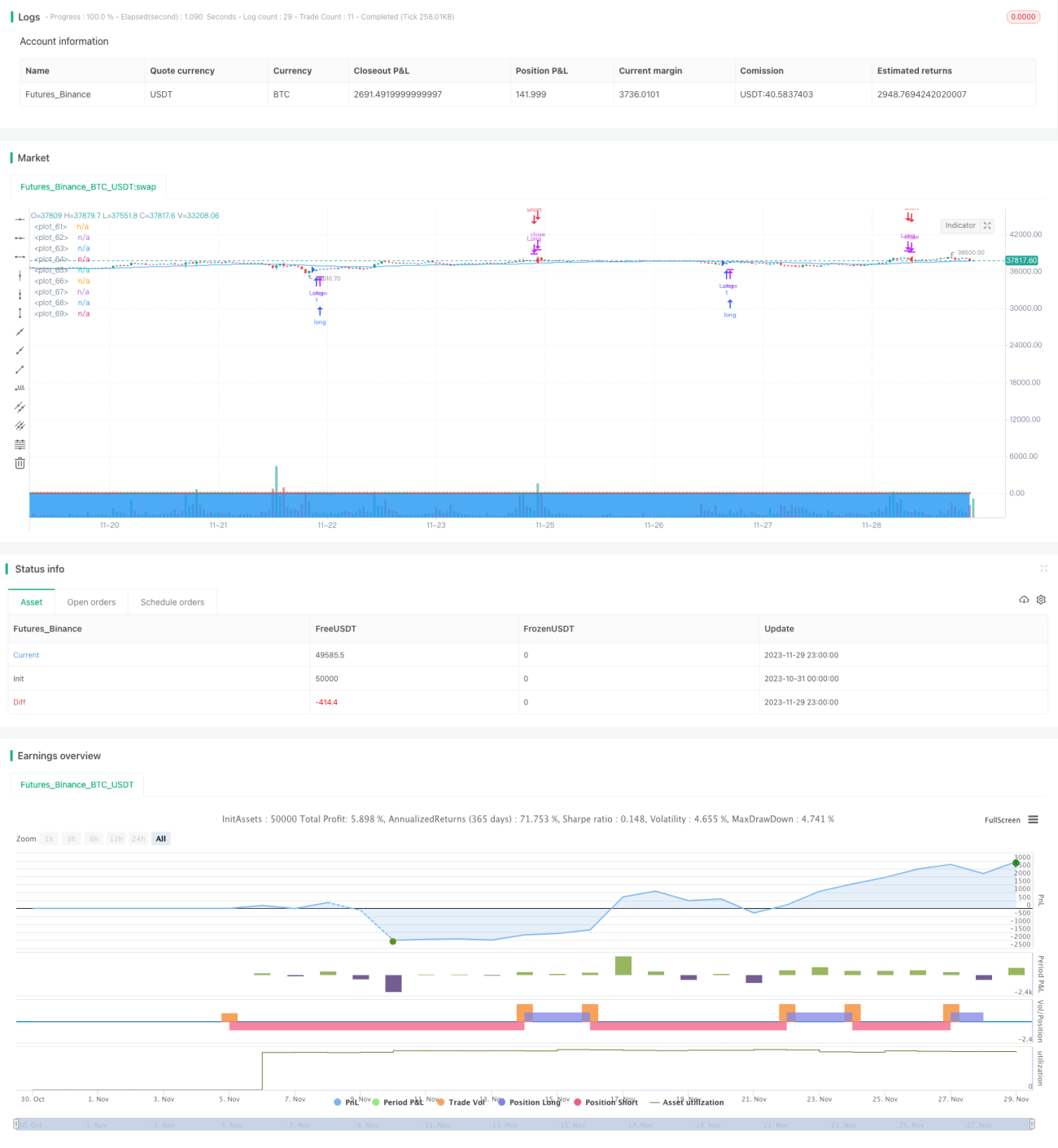

この戦略はLazyBearのオリジナルウェーブトレンド戦略に、第二のストップロス、複数の利益確定価格、および高時間足EMAフィルターを追加したものです。ウェーブトレンド指標を使用して取引シグナルを生成し、EMAフィルターとストップロス・利益確定管理を組み合わせることで、自動化されたトレンド追従取引を実現します。

戦略の原理

この戦略のコア指標はウェーブトレンド指標(WaveTrend)であり、以下の3つの部分から構成されます。

- AP:平均価格 = (高値 + 安値 + 終値) / 3

- ESA:APのn1期間EMA

- CI:(AP - ESA) / (0.015 × (AP - ESA)のn1期間EMAの絶対値)のn1期間EMA

- TCI:CIのn2期間EMA、すなわちウェーブトレンドライン1(WT1)

- WT2:WT1の4期間SMA

WT1がWT2を上抜けた場合(ゴールデンクロス)にロング、WT1がWT2を下抜けた場合(デッドクロス)にポジションをクローズします。

また、戦略は高時間足EMAをフィルターとして導入し、価格がEMAを上回っている場合のみロング、下回っている場合のみショートを許可することで、一部の偽シグナルを除外します。

戦略の優位性

- ウェーブトレンド指標を使用してトレンドを自動追跡し、人為的な判断ミスを回避

- 第二のストップロスを追加し、単一取引の損失を効果的に抑制

- 複数の利益確定価格を設定し、利益を最大限に確保

- EMAフィルターにより偽シグナルを除外し、勝率を向上

戦略のリスクと最適化

- トレンド反転をフィルターできないため、損失が発生する可能性がある

- パラメータ設定が不適切な場合、取引頻度が高くなりすぎる可能性がある

- 異なるパラメータの組み合わせをテストし、最適化が可能

- 他の指標と組み合わせてトレンド反転を判断することも検討可能

まとめ

この戦略は、トレンド追従、リスク管理、利益最大化など複数の側面を総合的に考慮しています。ウェーブトレンド指標で自動的にトレンドを捉え、EMAフィルターで取引効率を向上させ、トレンドを捉えつつリスクを管理する、効率的で安定したトレンド追従戦略です。さらなるパラメータ最適化と反転判断の追加により、この戦略の適用範囲をさらに拡大することができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1