ノロ波動チャネルスキャルピング戦略

1

Follow

1802

Followers

概要

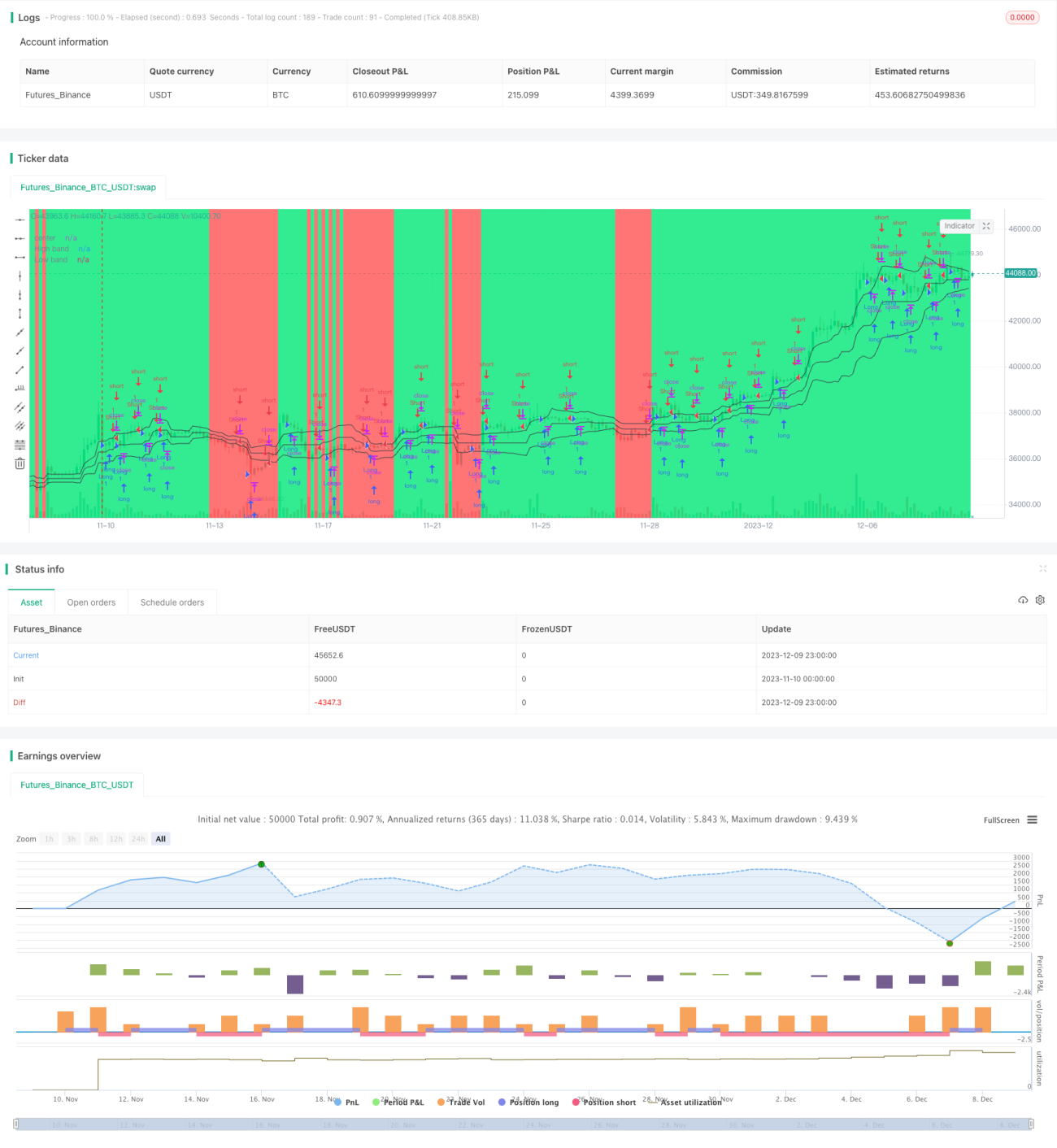

ノロ波動チャネルスキャルピング戦略(Noro's Price Channel Scalping Strategy)は、価格チャネルと価格波動帯を基にしたスキャルピング取引戦略です。この戦略は、価格チャネルと価格波動帯を用いて市場のトレンドを識別し、トレンド方向が転換した時点でエントリーを行います。

戦略の原理

まず、価格の最高値チャネル(lasthigh)と最安値チャネル(lastlow)を計算し、価格チャネルの中線(center)を求めます。次に、価格と中線の距離(dist)およびその距離の単純移動平均(distsma)を計算します。これにより、中線から1倍(hdおよびld)および2倍(hd2およびld2)の価格波動帯を導き出します。

価格が中線から1倍の波動帯を上抜けた場合を強気、下抜けた場合を弱気と判断します。この戦略は、トレンドが弱まった兆候が見られた時点で逆張りでポジションを取ります。例えば、強気トレンド下で2本の陽線が出現した場合、2本目の陽線の終値で空売りします。弱気トレンド下で2本の陰線が出現した場合、2本目の陰線の終値で買いを行います。

戦略のメリット

- 価格チャネルを利用して市場トレンドの方向を判断し、誤取引を回避

- 価格波動帯に基づいてトレンドの弱まりを判断し、転換点を正確に捉える

- スキャルピング方式の取引により、迅速に利益を獲得

戦略のリスク

- 価格の変動が大きい場合、価格チャネルや波動帯が機能しなくなる可能性がある

- スキャルピング取引は高い取引頻度を必要とし、取引コストやスリッページのリスクが増加しやすい

- 損失リスクを管理するために、ストップロス戦略を十分に考慮する必要がある

戦略の最適化

- 価格チャネルと波動帯のパラメータを最適化し、より多くの市場状況に対応

- 他のインジケーターと組み合わせてトレンドや転換点を判断

- ストップロス戦略を追加

- 取引コストとスリッページの影響を考慮

まとめ

ノロ波動チャネルスキャルピング戦略は、全体的にスキャルピング取引に非常に適した戦略です。価格チャネルと波動帯を利用して市場の動きを判断し、天井や底の兆候が見られた時点で逆張りでポジションを取ります。この戦略は取引頻度が高く、迅速に利益を得られますが、一定のリスクも伴います。さらなる最適化により、この戦略をより多くの異なる市場で適用できるようになります。

Source

Pine

/*backtest

start: 2023-11-10 00:00:00

end: 2023-12-10 00:00:00

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Scalper Strategy v1.0", shorttitle = "Scalper str 1.0", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1