多因子適応モメンタム追跡戦略

概要

マルチファクター適応型モメンタム追跡戦略は、複数のテクニカル指標を統合して市場トレンドと主要なサポート・レジスタンスラインを識別し、暗号通貨などの高変動資産の自動売買を実現します。この戦略は、RSI、MACD、ストキャスティクスなどの指標を総合的に活用して売買タイミングを判断するとともに、価格変動率を組み合わせることでより正確なパターン認識を実現します。

戦略の原理

マルチファクター適応型モメンタム追跡戦略の中核は、複数のテクニカル指標の統合活用にあります。本戦略は主に以下の要素で構成されています。

-

RSI指標による買われすぎ・売られすぎの判断。異なるパラメータを組み合わせることで、標準的なRSIシグナルまたは改良版のコナーRSIシグナルを識別し、反転の機会を判断します。

-

MACD指標によるトレンド方向の判断。MACDラインがシグナルラインを上抜けまたは下抜けした際に買い・売りシグナルを生成します。

-

ストキャスティクス指標による買われすぎ・売られすぎゾーンの識別。%K線と%D線のゴールデンクロス・デッドクロスの組み合わせシグナルで反転を判断します。

-

価格変動率による真のブレイクアウトの検証。一定期間における最高値、最安値、終値などの変化率を計算し、真のブレイクアウトが発生したかどうかを判断します。

-

EMA指標による大きな時間軸での強気・弱気の判断。短期線が長期線を上抜けした場合は強気シグナル、下抜けした場合は弱気シグナルとなります。

本戦略は市場の強気・弱気状態に応じてロングまたはショートのポジションを取り、ポジションに入った後はストップロスとテイクプロフィットを設定してリスクを効果的にコントロールします。反転シグナルが発生した場合はポジションを決済します。意思決定プロセス全体で複数のファクターを総合的に判断することで、より正確な判断を実現します。

優位性分析

本戦略には以下の利点があります。

-

マルチファクター駆動により判断の優位性がある。単一指標と比較して、複数の指標を組み合わせることで相互検証が可能となり、結果の精度と信頼性が向上し、不必要な取引コストを削減できます。

-

条件が厳格で誤った取引を回避できる。売買条件に厳しい要件を設定し、複数の指標が同時にシグナルを発する必要があるため、大量のノイズをフィルタリングし、誤った取引の発生を防ぎます。

-

適応型ハイパーパラメータにより人為的介入を低減。戦略内で指標パラメータを動的に計算する機能を備えているため、ハイパーパラメータの主観的な選択を回避し、戦略パラメータをより科学的かつ客観的にします。

-

ストップロス・テイクプロフィット機構によりリスクを管理。ポジションを開いた後、リアルタイムでストップロスとテイクプロフィットの位置を計算・描画し、1回の取引での損失を効果的に抑制し、ロスカットの発生を防ぎます。

リスク分析

本戦略には以下のリスクも存在するため注意が必要です。

-

指標の誤ったシグナル発生の可能性。複数指標による検証で誤シグナル率を大幅に低減できますが、発生する可能性は依然としてあります。これにより不必要な損失が生じる可能性があります。

-

ストップロスが突破されるリスク。極端な相場では価格が急落し、設定したストップロスが容易に突破され、大きな損失が発生する可能性があります。

-

パラメータ最適化による過学習。動的パラメータは人為的な選択の主観性を回避しますが、パラメータが過度に最適化され、汎化能力が失われる可能性もあります。

対応策:

- シグナルフィルタリング条件の厳格化を強化し、誤シグナル率を低減する。

- 分割建て方式を採用し、1回のストップロス幅が大きくなりすぎないようにする。

- テストサンプル量を増やし、パラメータの安定性を厳格に評価する。

戦略の最適化方向

マルチファクター適応型モメンタム追跡戦略には、以下の最適化可能な次元があります。

-

判断ファクターの数の増加。ボラティリティや出来高など、より多くの異なるタイプの指標シグナルを組み合わせて補助判断に活用する。

-

ストップロス機構アルゴリズムの最適化。トレーリングストップやボラティリティストップなど、より高度なストップロスアルゴリズムを導入し、ストップロス突破の確率をさらに低減する。

-

機械学習モデルの導入。RNN、LSTMなどのモデルを使用して過去のデータをモデリングし、売買判断の補助とする。

-

戦略のアンサンブル。複数のサブ戦略を採用し、アンサンブル学習手法で統合することで、より安定した総合パフォーマンスを得ることができる。

まとめ

マルチファクター適応型モメンタム追跡戦略は、複数のテクニカル指標を統合活用して売買タイミングを識別します。単一指標と比較して、本戦略はより正確な判断が可能であり、同時にパラメータの適応機構とストップロス機構を内蔵してリスクを管理します。今後、より多くの補助判断ファクター、高度なストップロスアルゴリズム、機械学習などの手法を導入することで、本戦略の効果をさらに強化することができます。

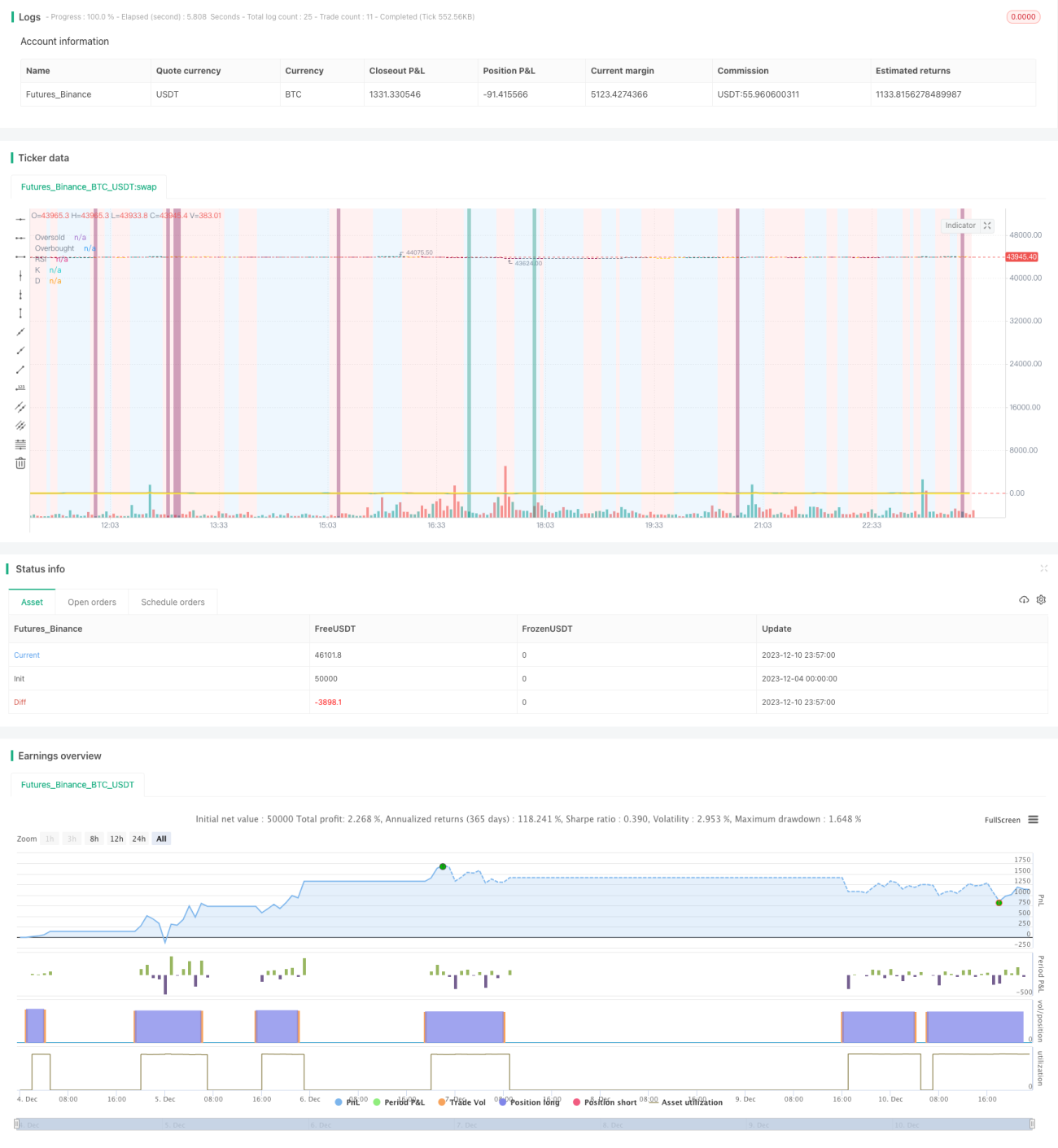

/*backtest

start: 2023-12-04 00:00:00

end: 2023-12-11 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

// ██████╗██████╗ ███████╗ █████╗ ████████╗███████╗██████╗ ██████╗ ██╗ ██╗ - 1