モメンタム・プルバック戦略

概要

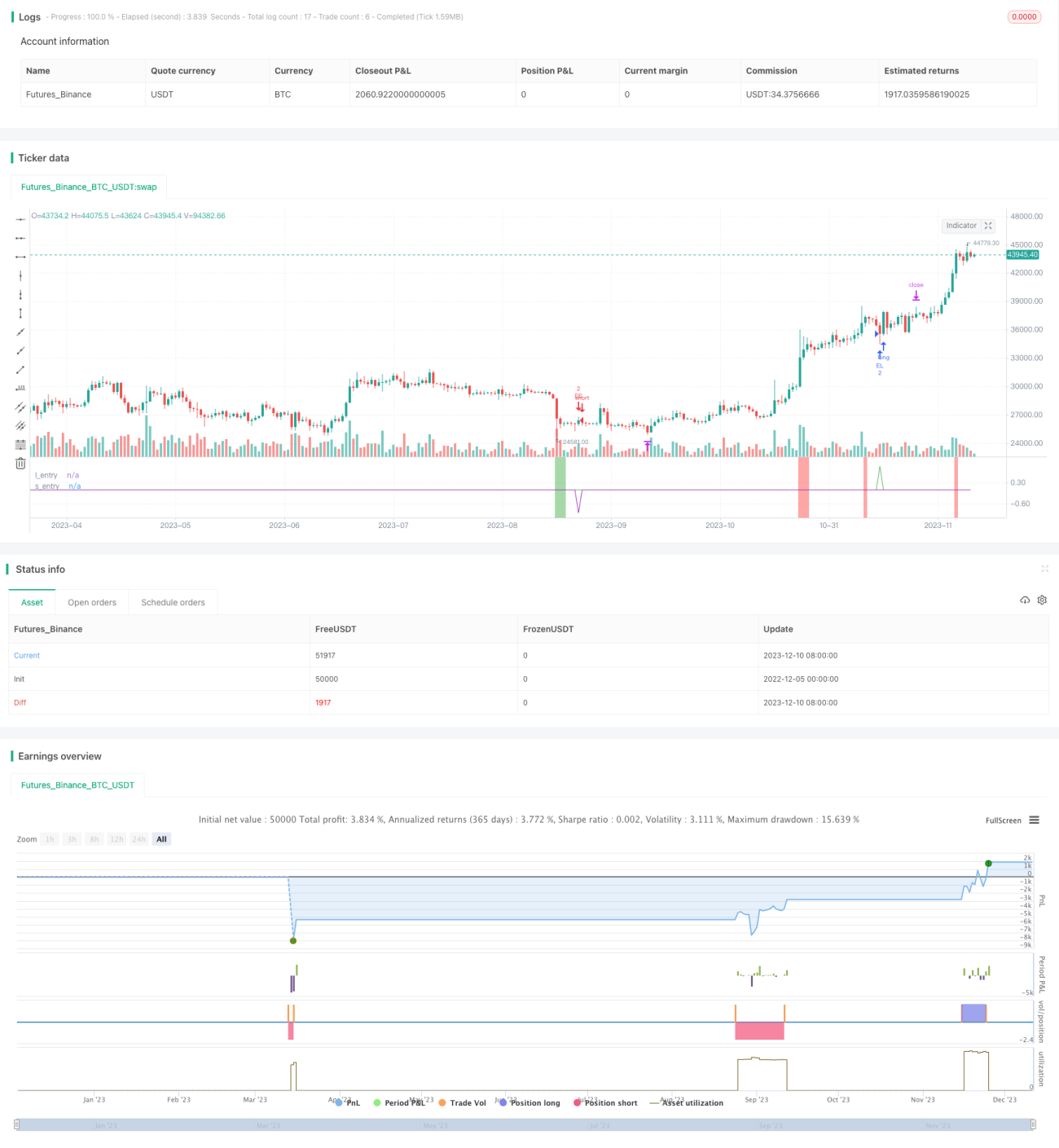

モメンタム・プルバック戦略(Momentum Pullback Strategy)は、RSIの極端値をモメンタムシグナルとして認識するロング・ショート両建て戦略です。ほとんどのRSI戦略とは異なり、本戦略は極端なRSI数値の方向に対して最初のプルバックをエントリーポイントとして活用します。

5日間EMA(最安値)/5日間EMA(最高値)への最初のプルバック地点でロング/ショートを行い、ローリング12本のローソク足の最高値/最安値で決済します。このローリング高値/安値メカニズムにより、価格が長期レンジ相場に入ると、利確目標は新しいローソク足が出現するたびに低下します。最良のトレードは通常2〜6本のローソク足内で完了します。

推奨ストップロス距離はエントリー価格のX倍ATR(ユーザー入力パラメータで調整可能)です。

本戦略は様々な時間軸と市場に対して堅牢性が高く、勝率は60%~70%、利益取引の規模は大きめです。重要な経済ニュースによるボラティリティの中でシグナルが発生するのは避ける必要があります。

戦略の原理

-

6日間RSIを計算し、90超(買われ過ぎ)および10未満(売られ過ぎ)の極端なポイントを探します。

-

RSIが買われ過ぎの場合、6本のローソク足以内に5日間EMA(最低ライン)までプルバックした地点でロングエントリー。

-

RSIが売られ過ぎの場合、6本のローソク足以内に5日間EMA(最高ライン)までプルバックした地点でショートエントリー。

-

エグジット戦略は移動利確。ロングポジションは過去12本のローソク足の最高値を最初の出口目標とし、新しいローソク足が出現するたびに新たな12本ローソク足最高値に更新することでローリング退出を実現。ショートはその逆で、ローリング12本ローソク足最安値でストップロス。

-

ストップロス距離はエントリー価格×X倍ATR。カスタマイズ可能。

優位性分析

本戦略はRSIの極値を勢いのシグナルとし、プルバックエントリーを組み合わせることで、トレンド中の潜在的な反転ポイントを捉え、勝率が高くなっています。

移動利確メカニズムにより、実際の価格動向に応じて利益の一部を確定し、ドローダウンを軽減できます。

ATRストップロスは1回あたりの損失を効果的にコントロールします。

堅牢性が高く、様々な市場やパラメータ組み合わせに適用可能で、実戦での再現が容易です。

リスク分析

ATR数値が大きすぎる場合、ストップロス距離が遠くなり、1回の損失が拡大する可能性があります。

██╗もみ合い相場が発生した場合、移動利確メカニズムにより利益幅が縮小されます。

プルバックの距離が深すぎて6本のローソク足を超えると、エントリーチャンスを逃します。

重大な経済イベントに遭遇した場合、スリッページやフェイクブレイクが発生する可能性があります。

最適化の方向性

エントリーに使用するローソク足の本数を短縮(例:6本から4本に変更)することで、エントリー成功率を高めるテストが可能。

ATR倍率を増やし、1回あたりのストップロスをさらにコントロールするテストが可能。

出来高指標と組み合わせることで、レンジ相場での逆行による損失を回避できる可能性。

プルバックが60分足レベルのミドルラインを突破した後にエントリーすることで、ノイズを一部フィルタリングできる。

まとめ

モメンタム・プルバック戦略は、全体的に見て非常に実用的な短期キャッチ戦略です。トレンド、反転、ストップロスの複数の側面を組み合わせ、実戦での運用が容易であると同時に、一定のアルファを備えています。パラメータ調整や他の指標との組み合わせにより、さらに安定性を向上させることができます。総じて、本戦略は定量取引の大きな福音であり、学習・活用する価値があります。

- 1