二重移動平均線とボラティリティに基づく株式投資戦略

1

Follow

1797

Followers

概要

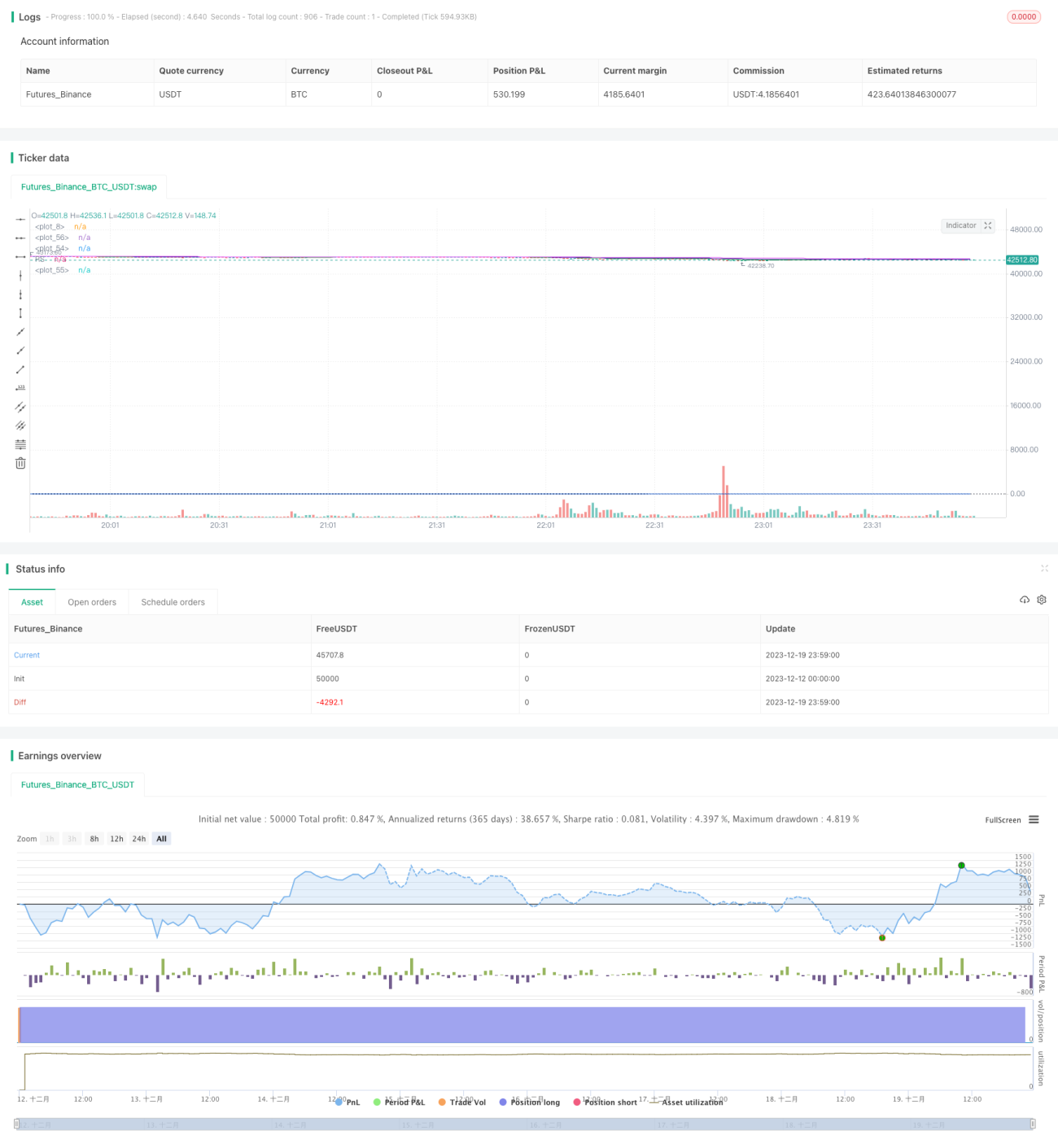

本戦略は、ダブル移動平均線と相対強度指標を基に、銘柄の過去のボラティリティを組み合わせて、自動売買を実現する。長期的な視点と短期的な視点を組み合わせ、リスクを効果的にコントロールできる点がメリットである。ただし、ストップロスメカニズムの追加など、改善の余地もある。

戦略の原理

週足150期間の長期移動平均線と日足50期間の短期移動平均線からなるダブル移動平均線システム、さらに日足20期間の最短期移動平均線を使用する。価格が週足150期間線を上抜けた場合に上昇トレンドの開始とみなし、日足50期間線を下抜けた場合に下降トレンドの開始とみなす。これにより、上昇トレンドでは買いと売りを繰り返し、下降トレンドでは随時ストップロスを実行することができる。

また、年率換算ボラティリティによる最高価格と相対強度指標を用いて具体的な買いタイミングを判断する。終値が年率換算ボラティリティで計算された最高価格を超え、かつ相対強度指標がプラスの場合にのみ買いシグナルを出す。

戦略のメリット

- ダブル移動平均線システムにより、主要トレンドの変化を効果的に捉え、トレンドフォローが可能。

- ボラティリティ指標と強度指標を加えることで、レンジ相場での無駄な売買を回避。

- 20日最短期移動平均線により、より早いストップロスが可能。

戦略のリスク

- 遅延が生じるため、迅速なストップロスが困難。

- ストップロスラインが設定されていないため、大きな損失が発生する可能性がある。

- パラメータの最適化が行われておらず、パラメータ設定が主観的である。

リスクを軽減するには、ストップロスラインの設定やATR指標の倍数をストップロス幅として利用することが考えられる。また、より厳格なバックテストによるパラメータの最適化も有効である。

戦略の最適化方向

- ストップロスメカニズムの追加

- パラメータ最適化手法を用いて最適なパラメータを発見する

- 出来高指標など他の指標によるシグナルのフィルタリングの検討

- マルチファクターモデル化し、より多くの指標を組み合わせる

まとめ

本戦略は総じて保守的な株式投資戦略である。ダブル移動平均線で主要トレンドを判断し、ボラティリティと強度指標でエントリーすることで、偽のブレイクアウトを効果的にフィルタリングできる。最短期移動平均線の追加によりストップロスも迅速に行える。ただし、ストップロスメカニズムの追加やパラメータ最適化など、さらなる改善の余地がある。全体として、長期的に株式を保有する投資家に適した戦略である。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1