動的トレーリングストップロス戦略

概要

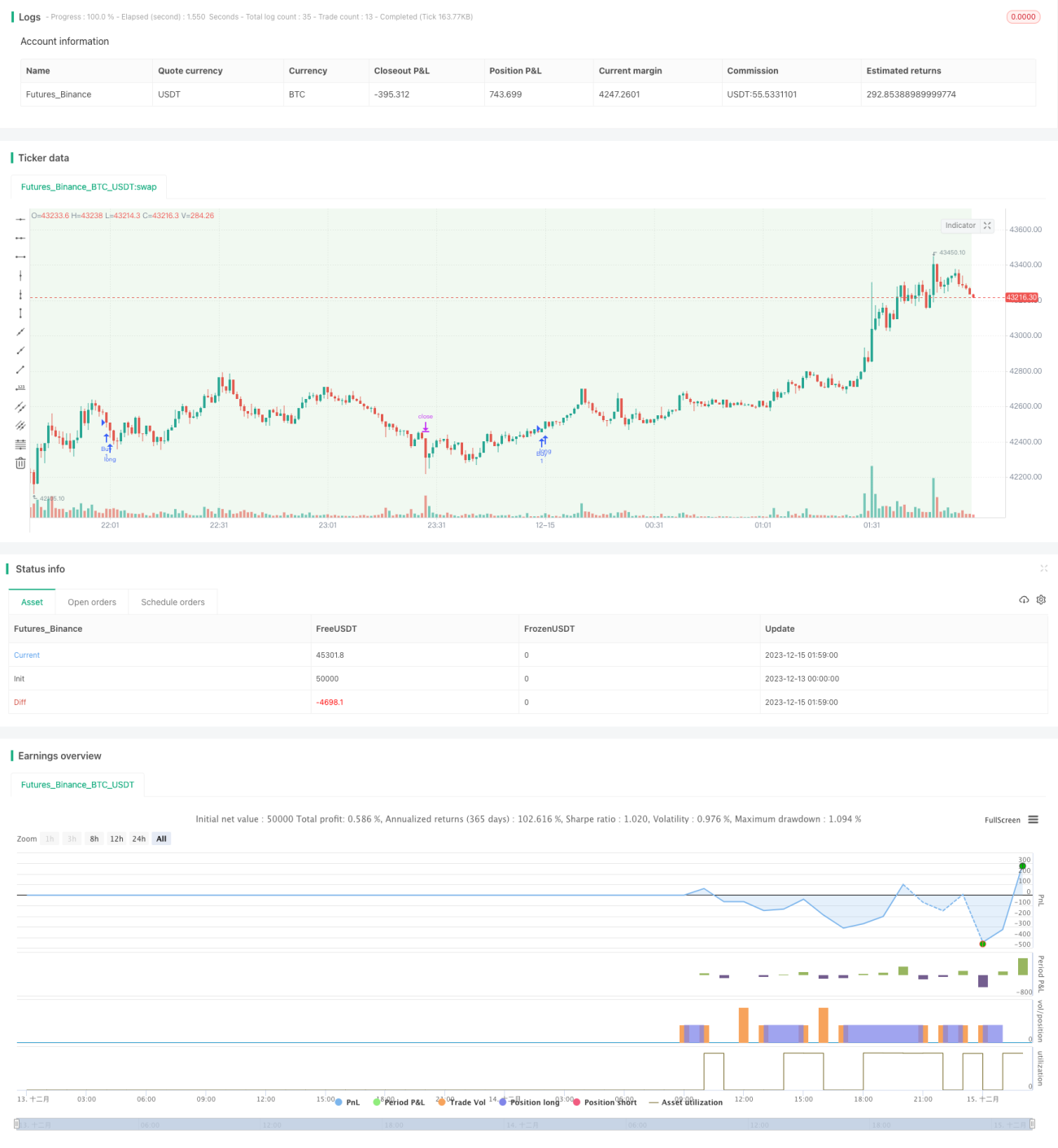

本戦略は日足でトレンド方向を判断し、15分足のローソク足で形成された新高値または新安値を損切りラインまたはトレーリングストップラインとして用いることで、動的に損切りラインを調整し、より多くの利益を確定する戦略です。

戦略の原理

-

日足の終値と前日の最高値・最安値を比較し、トレンド方向を判断します。終値が前日の最高値を上回った場合は上昇トレンド、終値が前日の最安値を下回った場合は下降トレンドと定義します。

-

上昇トレンド中、15分足の終値が前の15分足の最高値を上回った場合に買い建てます。下降トレンド中、15分足の終値が前の15分足の最安値を下回った場合に売り建てます。

-

買い建て後、前の15分足の最安値を損切りラインとします。売り建て後、前の15分足の最高値を損切りラインとします。

-

15分足が再び新高値または新安値を更新した場合、損切りラインを調整します。買い建ての場合は新たな安値に、売り建ての場合は新たな高値に調整し、動的なトレーリングストップを実現します。

優位性分析

本戦略の最大の利点は、損切りラインを動的に調整できることであり、リスク管理を確保しつつ、最大限に利益を確定し、損切りがヒットする確率を低減できる点です。

具体的な優位性は以下の通りです。

- トレンドに基づいて演算するため、市場の動きを適時に判断し、正しい取引方向を選択できます。

- 15分足での取引により、頻繁にエグジット・エントリーを行い、多くの機会を捉えることができます。

- 動的な損切り調整戦略により、新高値・新安値に基づいて損切りがヒットするリスクを低減できます。

- 損切りの位置が合理的に設定されており、無駄な損失を最大限回避できます。

リスク分析

本戦略の主なリスクは、トレンド判断の誤りに起因します。具体的なリスクポイントは以下の通りです。

- 日足のトレンド判断を誤ると、取引方向が逆になる可能性があります。

- 相場が短期的に激しく変動した場合、15分足の損切りラインが突破される確率が高くなります。

- トレンド転換点の認識を誤ると、損失が発生する可能性があります。

それぞれの解決方法は以下の通りです。

- 他の時間軸の指標を追加して総合的に判断し、単一の時間軸のみに依存した誤りを回避します。

- 市場のボラティリティを評価し、変動が大きい場合には損切り範囲を適度に緩和します。

- トレンド転換点を判断する仕組みを追加し、転換前に早期にポジションをクローズします。

最適化の方向性

本戦略にはさらなる最適化の余地があります。

- 他の時間軸の指標を追加して判断し、トレンド把握を最適化します。

- 異なる損切り比率の設定をテストし、最適なパラメータを選択します。

- 出来高指標を追加し、出来高のダイバージェンスによる誤った取引を回避します。

- トレンド転換メカニズムを追加し、エグジットポイントを最適化します。

- トレーリングストップの幅を評価・追加し、損切りがヒットする確率をさらに低減します。

まとめ

本戦略は全体的に良好な実行結果を示し、考え方が明確で理解しやすく、損切りの動的調整、頻繁な取引、順張りなどの利点を持ち、リスクを効果的に管理し利益を確定できるため、さらなるテストと最適化の適用に値します。しかし、改善の余地もあり、多角的な総合判断、パラメータ設定の最適化、トレンド転換の判別追加などの観点から取り組み、戦略の安定性と収益率をさらに高めることを推奨します。

- 1