RSIと取引量に基づく陰陽二重トレンド取引戦略

1

Follow

1802

Followers

概要

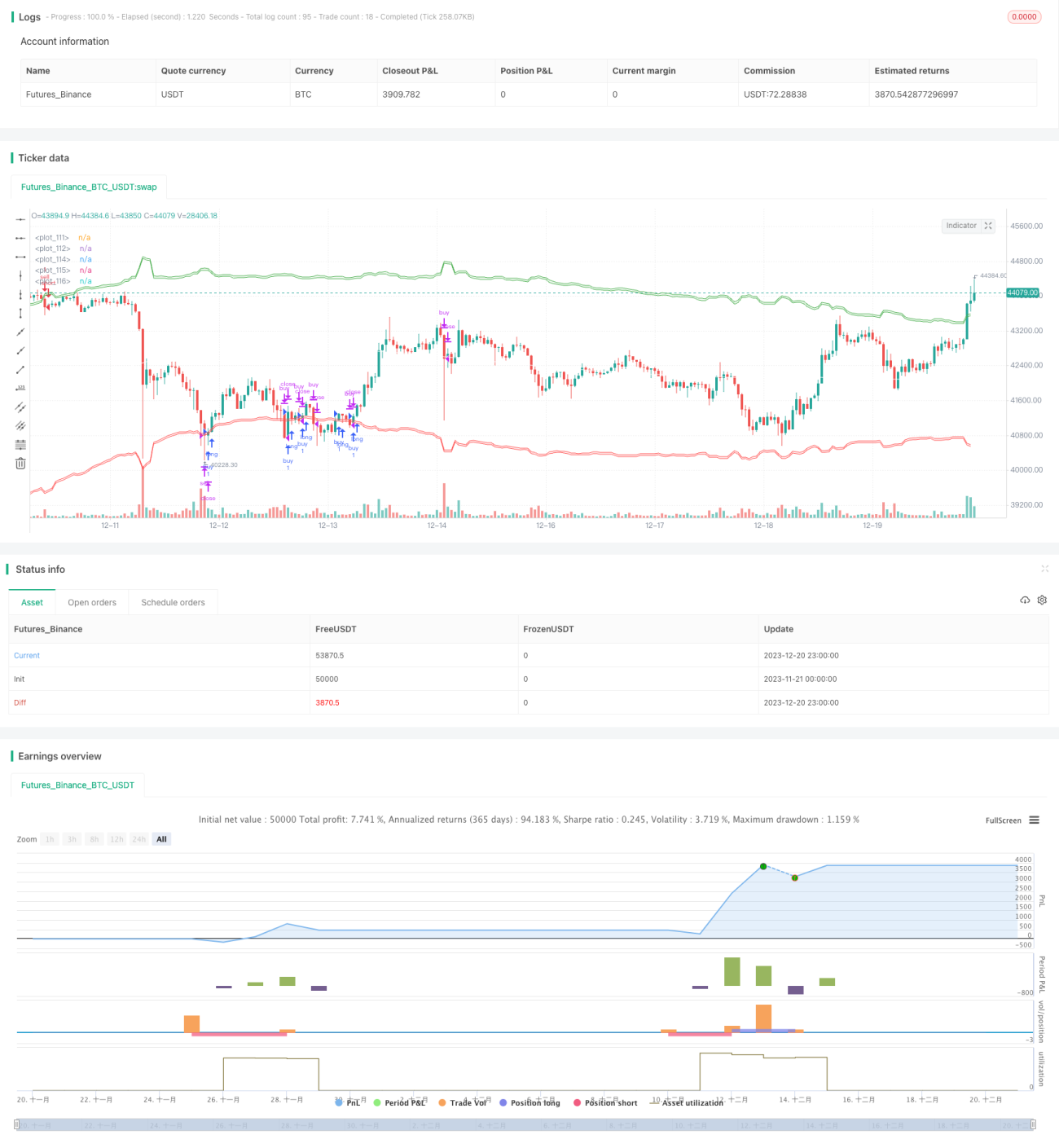

本戦略は、相対力指数(RSI)と取引量を組み合わせた指標を用いてトレンド方向を識別し、トレンド追跡を行う戦略です。主なポイントは以下の通りです。

- 加重移動平均線を使用して中心線を計算し、取引量情報を組み合わせてトレンドの中心を判断します。

- 中心線に基づいて買いゾーン、売りゾーンを設定します。

- RSI情報を使用して買いゾーンと売りゾーンの範囲を調整します。

- 買いゾーンに入った後にストップロスラインと利益確定ラインを設定します。

- 再エントリーの仕組みを備えています。

戦略の原理

本戦略では以下の指標とパラメータを使用します。

- 中心線:一定期間の最高値と最安値の加重移動平均線を計算し、取引量を重みとして使用してトレンドの中心方向を判断します。

- RSI:一定期間の相対力指数を計算し、0~1の範囲の数値に変換します。

- 買いゾーン:中心線にRSI調整量の一定割合を加えたもので、買いゾーンに入ると買いポジションを持つことができます。

- 売りゾーン:中心線からRSI調整量の一定割合を減じたもので、売りゾーンに入ると売りポジションを持つことができます。

- 利益確定ライン:中心線

- ストップロスライン:買いゾーン下方/売りゾーン上方に一定のパーセンテージで設定します。

価格が買いゾーンまたは売りゾーンに入ると、対応する方向でポジションを開きます。その後、利益確定ラインとストップロスラインを設定し、いずれかに達した場合にポジションをクローズします。同時に再エントリーの仕組みも設けられており、設定で許可されていれば、再度エントリーシグナルが発生した場合に再びポジションを持つことができます。

戦略の優位性

本戦略には以下の利点があります。

- RSIと取引量の二重指標でトレンドを識別し、判断精度を向上させます。

- RSIをパラメータ化して買いゾーンと売りゾーンの範囲を調整し、実際のトレンドに合わせやすくします。

- 取引量情報により価格変動の重みが増し、中心線の精度が向上します。

- ストップロス機構によりリスクを管理します。

- 再エントリーが可能で、偽のブレイクアウトによるリスクを低減します。

リスク分析

本戦略には以下のリスクも存在します。

- RSIと取引量のパラメータ設定が不適切だと、売買ゾーンの範囲判断の精度に影響を与える可能性があります。

- 中心線ではトレンドを完全に正確に判断できず、誤ったブレイクアウトが発生する可能性があります。

- ストップロスの設定が広すぎると、より大きな損失が発生する可能性があります。

- 再エントリーの仕組みにより、過剰な取引につながる可能性があります。

対応策:

- RSI期間や取引量期間のパラメータを市場状況に合わせて調整します。

- 他の指標と組み合わせて売買シグナルを検証し、誤ったブレイクアウトを回避します。

- ストップロスを適切に引き締め、1回の損失をコントロールします。

- 1日の取引回数を制限し、過剰取引を防ぎます。

戦略の最適化方向

本戦略は以下の点で最適化が可能です。

- ローソク足パターンやボラティリティ指標など、他の指標で売買シグナルを検証します。

- ポジション管理の仕組みを追加します(例えば、利益確定後にポジションを増やすなど)。

- 機械学習アルゴリズムを導入してトレンドの精度を判断し、売買ゾーンの設定精度を高めます。

- ストップロス・利益確定ラインの最適なパラメータを評価します。

- 銘柄ごとにパラメータが異なるため、個別にテスト・最適化を行う必要があります。

まとめ

本戦略は全体的に、RSIと取引量の指標を用いてトレンドを追跡する定量戦略です。トレンドシグナルを二重に検証する仕組みがあり、ストップロスと利益確定でリスクをコントロールし、再エントリーの仕組みで利益機会を高めています。パラメータ調整やアルゴリズムの最適化により、非常に実用的なトレンド追跡取引戦略となります。

Source

Pine

/*backtest

start: 2023-11-21 00:00:00

end: 2023-12-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@

// @@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@@ ,@@@@@@@@@@@@@@@@@@@@@@@Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1