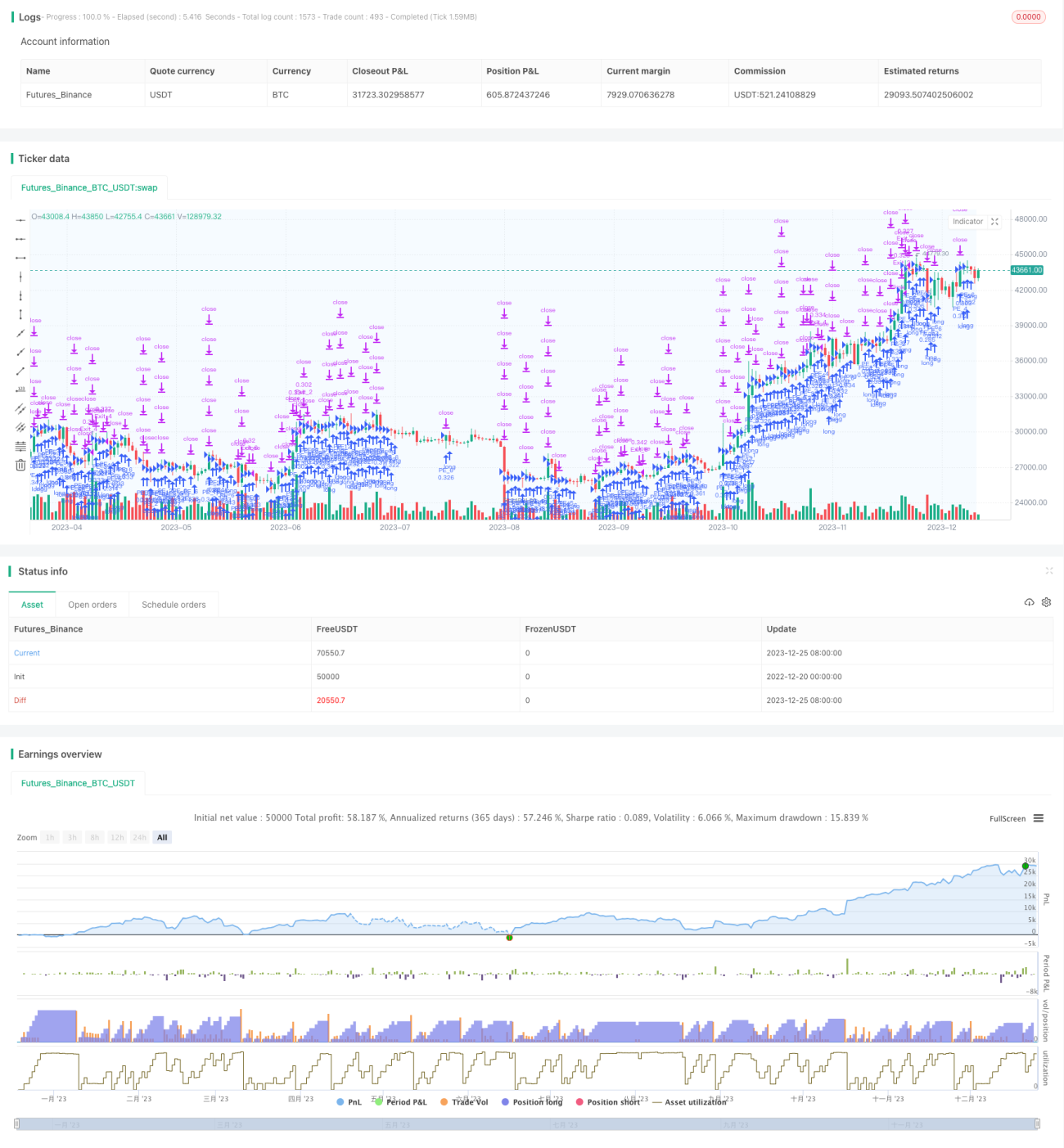

時間の階段状追加投資に基づくシンプルな定量取引戦略

概要

本戦略は、時間の階段状ポジション追加を利用した簡単な定量取引戦略です。基本的な考え方は、毎日決まった時間にロングポジションを建て、各ポジションに異なる利益確定・損切り条件を設定することで、分割して利益確定または損切りを行うことです。

戦略の仕組み

本戦略は主に3つの重要なロジックに基づいています。

-

時間階段状ポジション追加

sessionTimeパラメータで日内の取引時間帯を設定します。この時間帯において、毎日取引開始時に固定の階段状にポジションを追加します。追加数量は資金プールの最大ポジション数量を均等に割り当てたものです。 -

個別の利益確定・損切り

各取引注文に対して、それぞれ利益確定点

takeProfitと損切り点stopLossを設定します。これにより、各注文が独立した利益確定・損切りのロジックを持ち、分割での利益確定・損切りが可能になります。 -

時間帯終了時の決済

日内取引時間帯が終了した時点で、その時間帯に利益確定・損切りされていない全ての注文を決済するかどうかを選択できます。

戦略の利点

本戦略には以下の利点があります。

-

リスク分散:資金プール内の資金を均等に異なる注文に割り当て、単一注文の損失を効果的に抑止します。

-

分割利益確定・損切り:各注文が独立した利益確定・損切りロジックを持ち、全注文が同時に損切りされるのを防ぎます。

-

柔軟な設定:最大ポジション追加回数、毎日の取引時間帯、利益確定・損切りの比率などをカスタマイズできます。

-

理解しやすい:戦略ロジックがシンプルで明確です。

戦略のリスク

本戦略には以下のリスクも存在します。

-

含み損リスク:全ての注文が利益確定ラインに達する前に、対応する損切りラインをトリガーすると、大きな損失が発生する可能性があります。適切な損切り比率を設定することで回避できます。

-

1日の総建て玉高の制限不可:特殊な相場の状況で、過剰な注文が同時にポジション追加されると、資金の許容範囲を超える可能性があります。1日の総ポジション追加額に上限を設けることを検討できます。

-

時間帯設定のミスによる機会損失:取引時間帯の設定が適切でないと相場のチャンスを逃す可能性があります。取引時間帯は対象とする取引商品の活発な時間帯を参考にして設定することを推奨します。

戦略の最適化

本戦略は以下の方向で最適化できます。

-

建玉条件判断ロジックの追加:特定のテクニカル指標シグナルが満たされた場合のみ建玉し、盲目的なポジション追加を避けます。

-

1日の総ポジション追加額の上限設定:資金プールの許容範囲を超えるのを防ぎます。

-

異なる注文に異なる利益確定・損切り比率を設定:差額を持たせた利益確定・損切りを実現します。

-

注文数と資金プール残高の連動ロジック追加:注文数と利用可能資金を連動させます。

まとめ

本戦略は、時間の階段状ポジション追加という考え方を利用した非常にシンプルな定量取引戦略テンプレートです。戦略ロジックは明確で、一定のリスクと最適化の余地があります。開発者はこれを基に適切に最適化することで、より安定した信頼性の高い定量戦略にすることができます。

- 1