忍耐強くトレンドに追従する戦略

概要

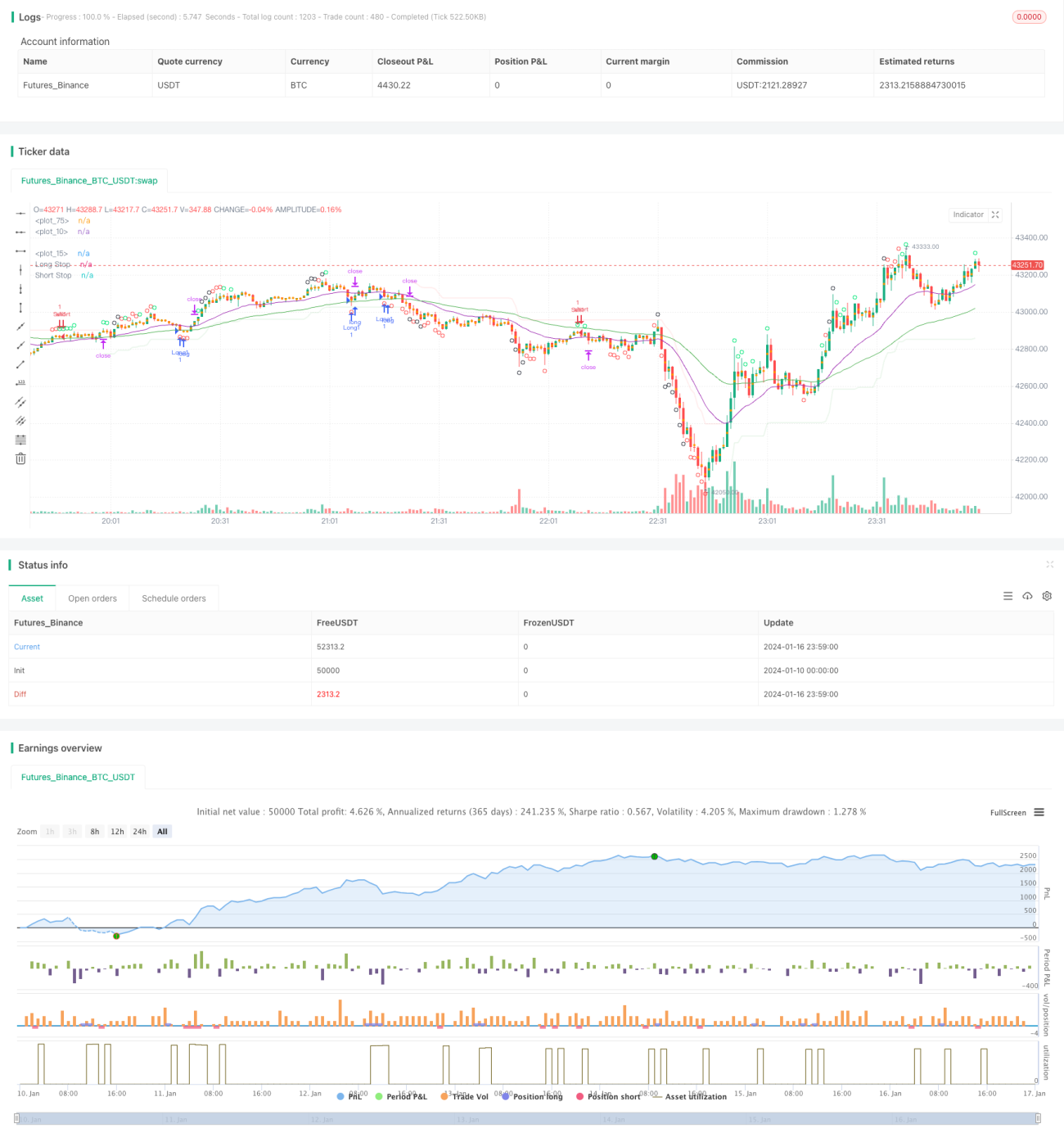

「耐心追踪趋势策略」はトレンドフォロー型の戦略です。移動平均線の組み合わせでトレンド方向を判断し、オーバーボート/オーバーソールの指標であるCCIを利用して取引シグナルを生成します。大きなトレンドを狙い、レンジ相場ではポジションが拘束されるのを効果的に回避できます。

戦略の原理

本戦略は21期間と55期間のEMAの組み合わせでトレンド方向を判断します。短期EMAが長期EMAより上にある場合は上昇トレンド、下にある場合は下降トレンドと定義します。

CCIインジケーターはオーバーボート/オーバーソールの状態を判断するために使用します。CCIが-100ラインを上抜けると底値のオーバーソールシグナル、100ラインを下抜けると天井のオーバーボートシグナルとなります。CCIの異なるオーバーボート/オーバーソールラインに応じて、戦略は3段階の取引シグナル強度レベルに分けられます。

上昇トレンドと判断された場合、CCIが強い底値のオーバーソールシグナルを発したときにロングエントリーします。下降トレンドと判断された場合、CCIが強い天井のオーバーボートシグナルを発したときにショートエントリーします。

ストップロスラインはSuperTrendインジケーターで設定し、目標利益は固定のポイント数とします。

優位性分析

本戦略には主に以下の優位性があります。

- 大きなトレンドを追跡し、ポジション拘束を回避

- CCIインジケーターで反転ポイントを効果的に判断可能

- SuperTrendによるストップロスラインの設定が適切

- 固定ストップロスと固定利確により、リスクをコントロール可能

リスク分析

本戦略には主に以下のリスクがあります。

- 大きなトレンド判断を誤る確率

- CCIインジケーターが偽シグナルを発する確率

- ストップロスが浅すぎたり深すぎたりして不要な損切りが発生する確率

- 固定利確ではトレンドに沿って利益を伸ばせない確率

これらのリスクに対し、EMA期間パラメータ、CCIパラメータ、ストップロス・利確ポイントの調整により最適化可能です。また、より多くのインジケーターを導入して戦略シグナルを検証することも重要です。

最適化の方向性

本戦略の最適化の方向性は主に以下の通りです。

-

より多くのインジケーターの組み合わせをテストし、より優れたトレンド判断およびシグナル検証インジケーターを見つける。

-

ATRによる動的ストップロス・利確を採用し、トレンド追跡とリスク管理を向上させる。

-

過去データで学習した機械学習モデルを導入し、トレンド確率を判断する。

-

異なる銘柄に応じてパラメータを調整・最適化する。

まとめ

「耐心追踪趋势策略」は全体的に非常に実用的なトレンドフォロー戦略です。移動平均線で大きなトレンド方向を判断し、CCIインジケーターで反転ポイントのシグナルを発見し、スーパートレンドストップロスラインを適切に設定します。パラメータ調整と複数インジケーターの組み合わせ検証により、本戦略はさらなる最適化が可能であり、長期の実運用での追跡検証に値します。

- 1