EMA平均線に基づく両方向ダイナミックストップロスのクロス相場トレンド追随戦略

1

Follow

1802

Followers

概要

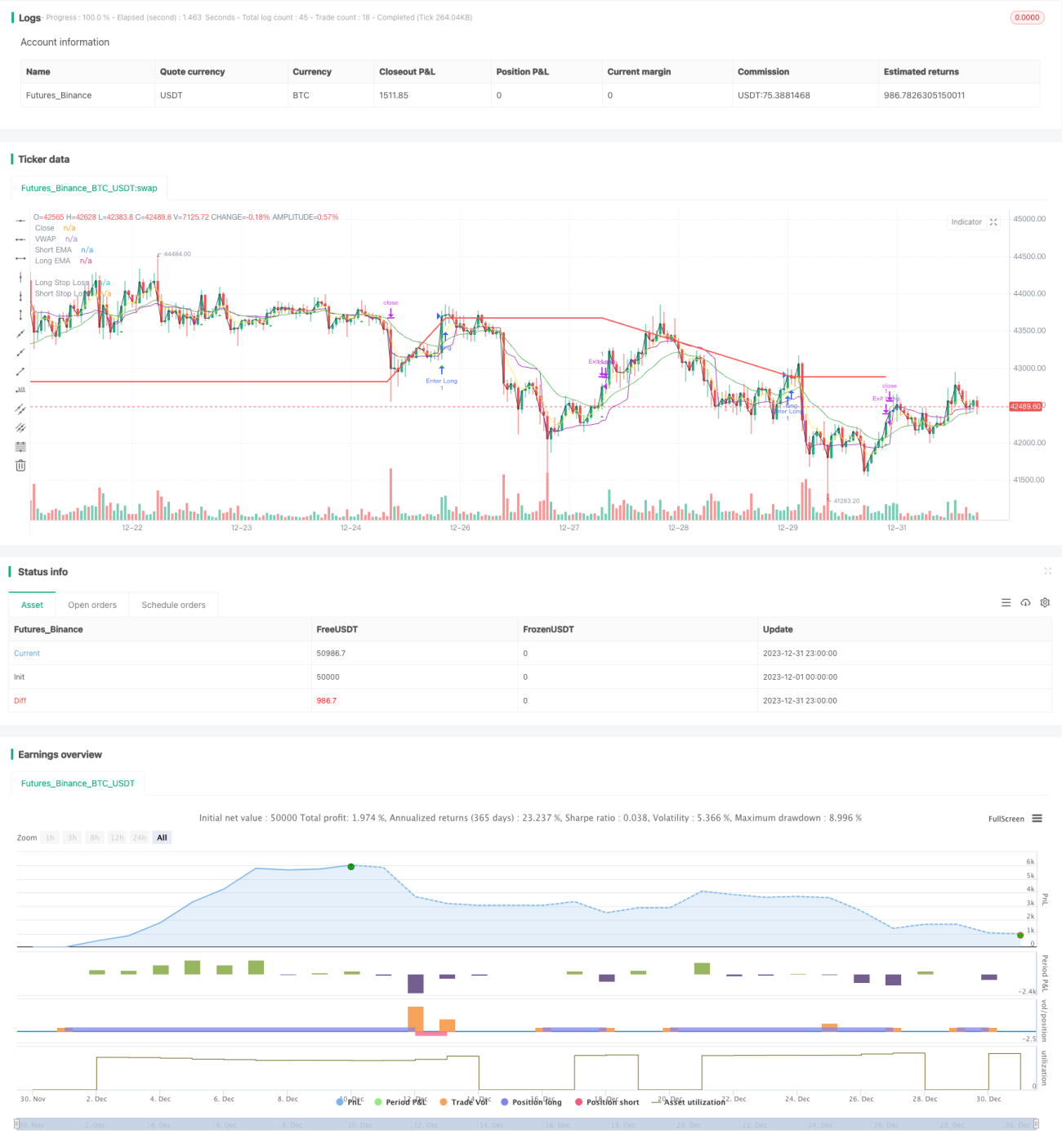

本戦略は、EMA平均線のゴールデンクロス・デッドクロスに基づいて双方向に追跡し、動的なロング・ショートのストップロスラインを設定することで、トレンド相場を捉えることを目的としています。

戦略原理

- 短期EMA線(5日)と長期EMA線(20日)を計算します。

- 短期線が下から上に長期線をクロスした場合に買い(ロング)、短期線が上から下に長期線をクロスした場合に売り(ショート)を行います。

- 買いポジション後、動的ストップロスラインをエントリー価格×(1-ロングポジションのストップロス率)に設定します。売りポジション後は、エントリー価格×(1+ショートポジションのストップロス率)に設定します。

- 価格が対応するストップロスラインに触れた場合、ストップロスで決済します。

優位性分析

- EMA平均線はトレンドを追跡する能力が高く、双方向のクロスがタイマーとして機能するため、トレンドの機会を効果的に捉えることができます。

- ストップロスラインを動的に計算し、利益が出た後に相場に追随することで、トレンド利益を最大限に確保できます。

- 追加フィルター条件としてVWAPを採用することで、損失を回避し、シグナルの質を向上させます。

リスク分析

- 純粋なトレンド戦略であり、レンジ相場では損失を被る可能性があります。

- ストップロスが緩すぎると、損失が拡大する恐れがあります。

- EMA平均線のシグナルに遅延が生じるため、最適なエントリーポイントを逃す可能性があります。

ATRを用いたリスク管理、短期ストップロス戦略の最適化、または他の指標を組み合わせたノイズ除去などにより改善可能です。

最適化の方向性

- ATRやDONCHなどの動的ストップロス指標を組み合わせ、市場に適応したストップロスラインを設定します。

- MACDやKDJなど、他のテクニカル指標を追加してシグナルをフィルタリングし、誤ったエントリーやエグジットを減らします。

- パラメータを最適化し、最適な短期・長期移動平均線の組み合わせを模索します。

- 機械学習を用いて最適なパラメータを探索する方法も試すことができます。

まとめ

本戦略は、全体的に見て非常に典型的なトレンドフォロー戦略です。2本のEMAによるゴールデンクロス・デッドクロスと動的ストップロスにより、トレンドの利益を効果的に確保できます。一方で、遅延リスクやストップロスが広すぎるリスクも存在します。パラメータ最適化、リスク管理、シグナルフィルタリングなどを通じて、より優れた戦略パフォーマンスを得ることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1