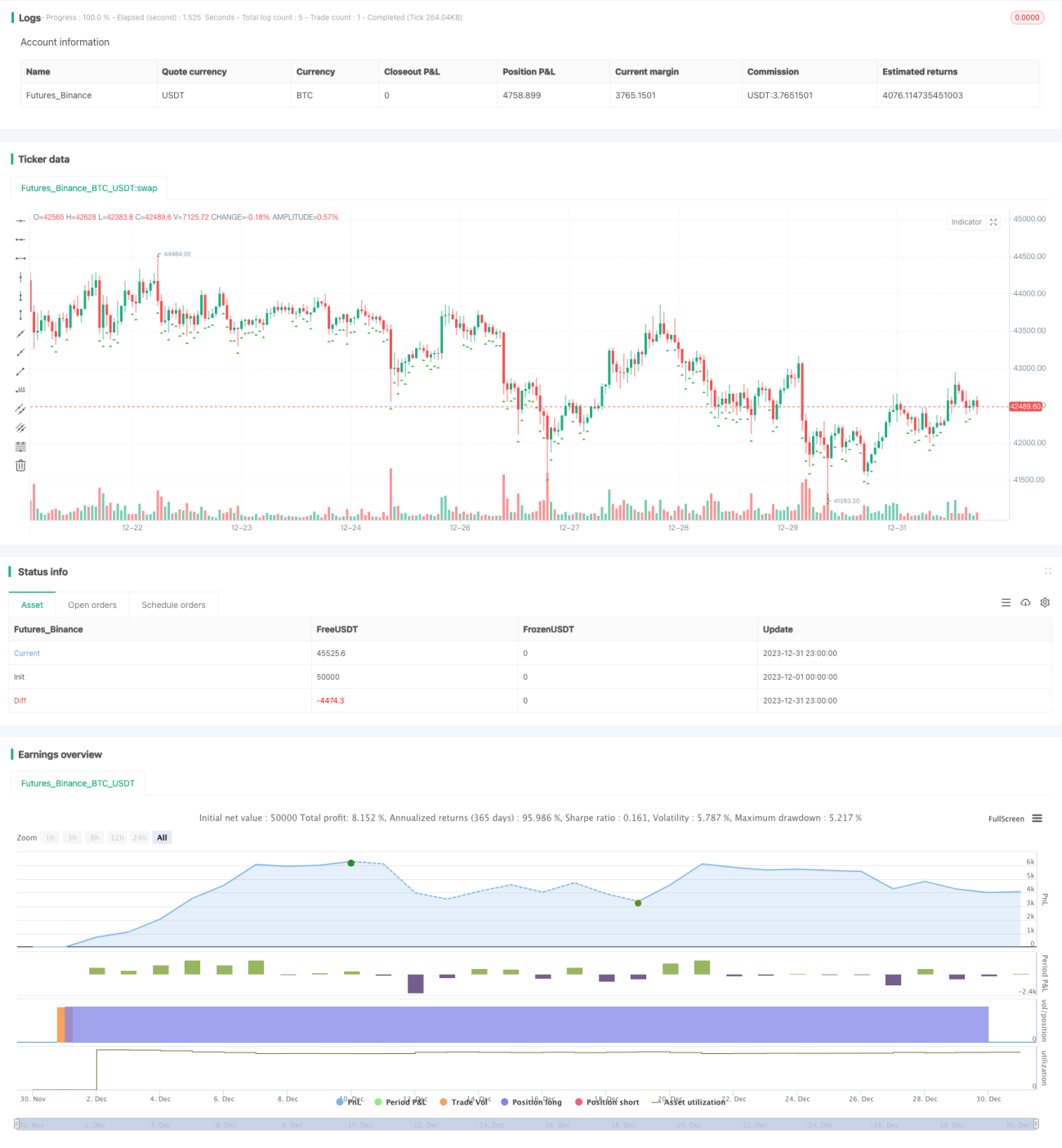

RSI指標のダマシ取引戦略

概要

RSI指標吸盤取引戦略は、RSIとCCIテクニカル指標を統合した固定グリッド取引手法です。この戦略は、RSIとCCI指標の値に基づいてエントリーのタイミングを判断し、固定利益率と固定グリッド数を使って利確注文と追加注文を設定します。また、ブレイクアウト的な価格変動に対するヘッジメカニズムも組み込まれています。

戦略の原理

エントリー条件

5分足と30分足のRSI指標が共に設定された閾値を下回り、かつ1時間足のCCI指標も設定値より低い場合に、買いシグナルが発生します。この時点の終値をエントリー価格として記録し、口座残高とグリッド数に基づいて最初のポジションサイズを計算します。

利確条件

エントリー価格を基準に、設定された目標利益率に従って利益確定価格を算出し、その価格帯に利確注文を設定します。

追加注文条件

最初の注文以外の残りの固定グリッド追加注文は、エントリーシグナル後に1つずつ発出され、設定されたグリッド数に達するまで続きます。

ヘッジメカニズム

エントリー価格から設定されたヘッジ閾値のパーセンテージ以上に価格が上昇した場合、全ポジションをヘッジクローズします。

反転メカニズム

エントリー価格から設定された反転閾値のパーセンテージ以上に価格が下落した場合、すべての未約定注文をキャンセルし、次のエントリーチャンスを待ちます。

優位性分析

- RSIとCCIの2つの指標を組み合わせることで、収益確率を向上

- 固定グリッドによる目標利益の設定で、収益の確実性を増加

- ヘッジメカニズムの統合により、急激な価格変動リスクを効果的に防止

- 反転メカニズムの導入により、損失を軽減可能

リスク分析

- 指標が誤ったシグナルを発する確率

- 急激な価格変動がヘッジ閾値を突破するリスク

- 反転後に再びトレンドが戻った場合に再エントリーできなくなるリスク

これらのリスクは、指標パラメータの調整、ヘッジ幅の拡大、反転幅の縮小によって低減できます。

最適化の方向性

- より多様な指標の組み合わせをテスト可能

- 適応型利確メカニズムの研究

- 追加注文ロジックの最適化

まとめ

RSI指標吸盤取引戦略は、指標によってエントリータイミングを判断し、固定グリッドでの利確と追加注文によって安定した利益を確保します。同時に、大きな変動に対するヘッジや反転後の再エントリーメカニズムを備えています。これらのメカニズムを統合した戦略により、取引リスクを低減し、利益率を向上させることができます。指標やパラメータ設定をさらに最適化することで、より良い実運用効果が得られます。

- 1