ドンチアンチャネルブレイクアウトトレンドフォロー戦略

概要

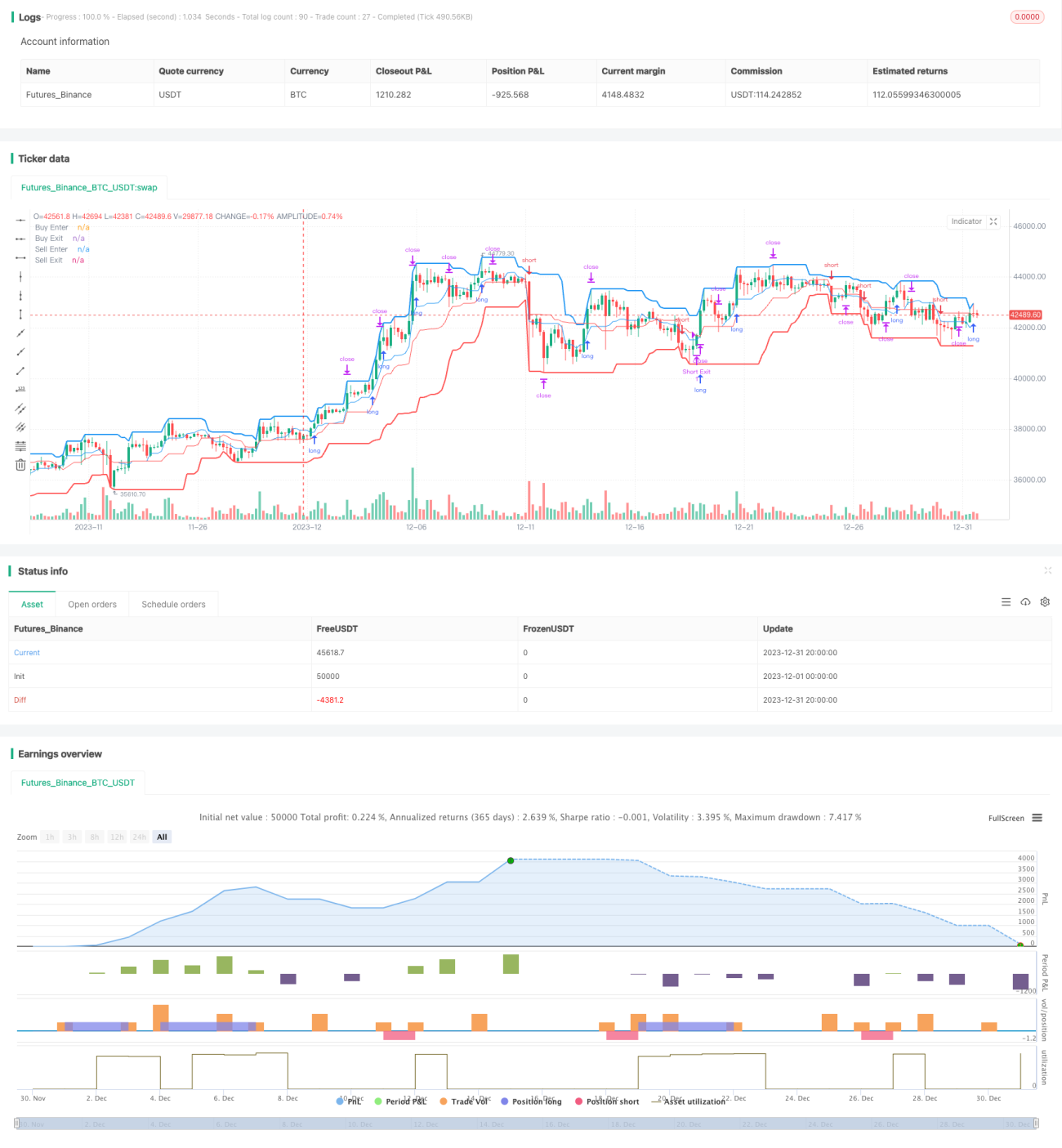

ドンチアンチャネルブレイクアウト戦略は、トレンドフォロー戦略の一種であり、一定期間の最高値と最安値を計算して価格チャネルを形成し、チャネルの境界を買いと売りのシグナルとして利用します。価格が上限を突破したらショート、下限を突破したらロングのポジションを取ります。この戦略は、ボラティリティの高い暗号通貨取引に適しています。

戦略の原理

本戦略では、ドンチアンチャネル指標を用いて価格トレンドを判断し、エントリーとイグジットのポイントを計算します。ドンチアンチャネルは上限、下限、中央値から構成されます。上限は一定期間の最高値、下限は最安値、中央値は平均価格です。

エントリーとイグジットの期間は独立して設定可能です。価格が下限を上抜けした場合にロングエントリー、上限を下抜けした場合にショートエントリーとなります。イグジットポイントは、価格が再度それぞれの軌道に接触したときです。また、中央値をストップロスラインとして使用することもできます。

さらに、戦略には利確ポイントが設定されています。ロングポジションの利確価格はエントリー価格の(1+利確率)倍、ショートポジションの場合はその逆です。この機能を有効にすることで、利益を確定し、損失拡大を防ぐことができます。

全体的に、本戦略はトレンドを判断すると同時に、ストップロスと利確の設定に十分な余地を確保します。そのため、暗号通貨などボラティリティの高い銘柄に特に適しています。

優位性分析

本戦略には以下の優位性があります。

- 戦略の判断が明確で、シグナル生成がシンプルかつ信頼性が高い。

- ドンチアンチャネル指標は価格の乱高下に影響されにくく、トレンドを捉えやすい。

- チャネルパラメータをカスタマイズ可能で、さまざまな銘柄や時間足に適応できる。

- ストップロス・利確機能が組み込まれており、リスク管理が効果的に行える。

- 暗号通貨のような高ボラティリティ銘柄に適しており、収益の可能性が大きい。

リスク分析

本戦略には以下のリスクも存在します。

- ストップロス機能はあるものの、急激な大相場を完全に回避できるわけではない。

- パラメータ設定が不適切だと、取引頻度が高くなりすぎ、取引コストやスリッページのリスクが増加する。

- 価格の乱高下に鈍感なため、一部の取引機会を逃す可能性がある。

上記リスクを抑制するために、以下の対策を推奨します。

- 1回の投資金額を適切に小さくし、投資銘柄を分散することで、全体のリスクをコントロールする。

- パラメータを最適化し、最適なパラメータの組み合わせを見つける。機械学習などを用いた自動最適化も検討する。

- 追加の指標を組み合わせてブレイクアウトシグナルの信頼性を判断し、誤取引を回避する。

最適化の方向性

本戦略は以下の観点からさらに最適化が可能です。

- より多くのパラメータ組み合わせをテスト・最適化し、最適なパラメータを探索する。主なパラメータには、チャネル期間、利確率、ロング・ショートの許可有無などがある。

- 機械学習モデルを追加し、最適なパラメータを自動的に識別する。強化学習などの手法を採用できる。

- 移動平均線や出来高など、他の指標を組み合わせてトレンドやシグナルの信頼性を判断する。

- トレーリングストップやChandelier Exitなどのストップロス戦略を開発し、リスクをさらに抑制する。

- より多くの銘柄に拡張し、本戦略に最も適した取引銘柄を探す。

まとめ

ドンチアンチャネルブレイクアウト戦略は、全体的に判断が明確でリスクコントロール可能なトレンドフォロー戦略です。特に暗号通貨のような高ボラティリティ銘柄に適しており、収益の可能性が大きいです。同時に、パラメータの最適化余地や他の指標との組み合わせの可能性もあり、これらは将来の拡張方向です。継続的な最適化と革新により、本戦略は暗号通貨のアルゴリズム取引において重要な選択肢となることが期待されます。

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © algotradingcc

// Strategy testing and optimisation for free trading bot

- 1