市場潜在力イチモク買い雲戦略

1

Follow

1802

Followers

概要

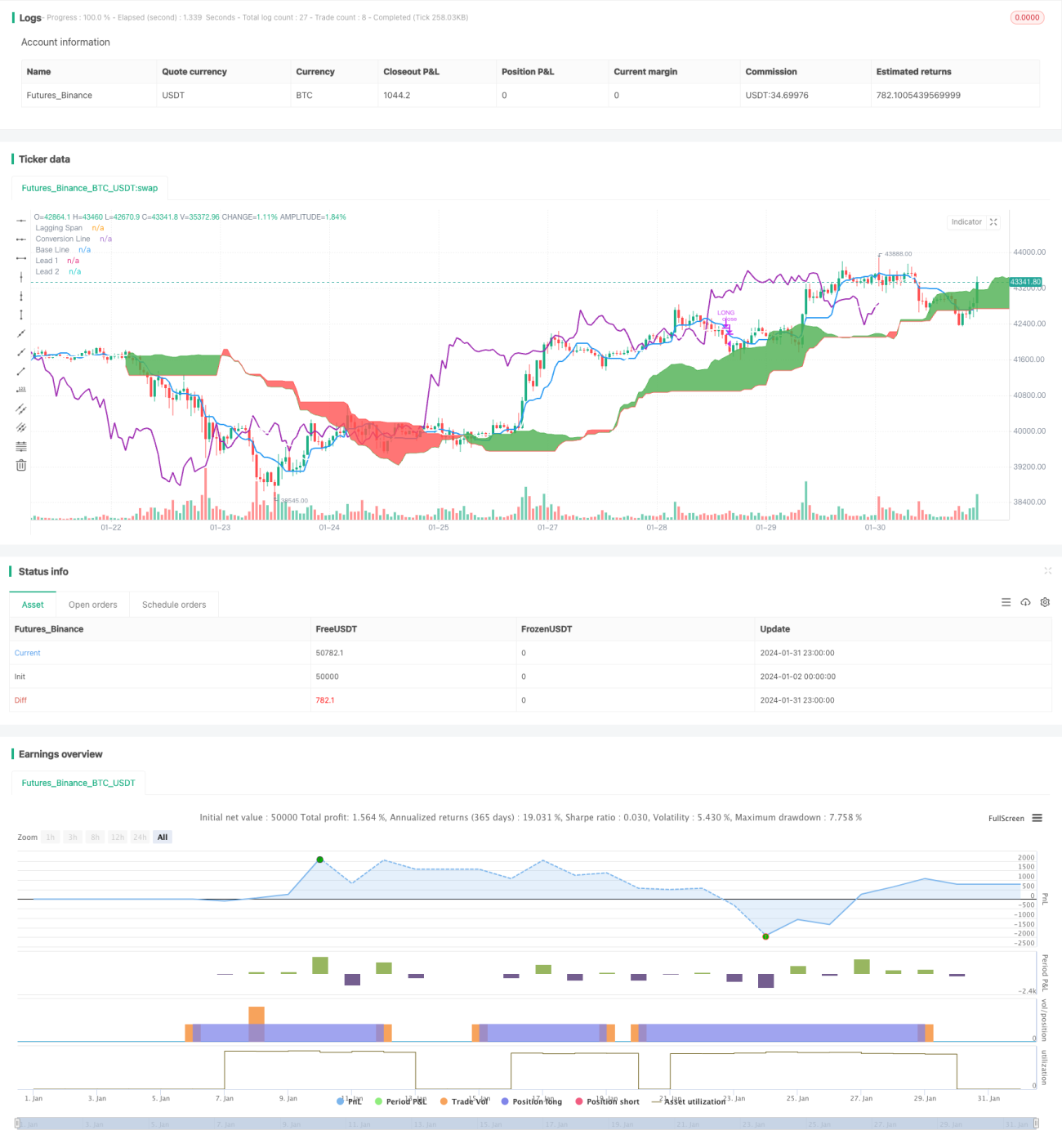

本戦略はロング専用の一目均衡表(Ichimoku)クラウド取引戦略です。転換線が基準線を上抜けた時にロングポジションを建て、基準線が転換線を下抜けた時に決済します。また、建玉時と決済時には遅行スパン(Chikou Span)も確認し、遅行スパンが雲の上にある場合は建玉、雲の下にある場合は決済を行います。

戦略の原理

本戦略は一目均衡表の複数のラインを使用します。具体的には以下の通りです。

- 転換線:過去9日間の最高値と最安値の平均値。一定期間のトレンド転換を表します。

- 基準線:過去26日間の最高値と最安値の平均値。一定期間内の平均価格変動を表します。

- 先行スパンA:転換線と基準線の平均値。

- 先行スパンB:過去52日間の最高値と最安値の平均値。中期から長期のトレンド先行指標です。

- 遅行スパン:当日の終値を26日遅らせたもの。トレンドの強さを表します。

建玉時には、転換線が基準線を上抜け、かつ遅行スパンが雲の上にあるという条件を同時に満たす必要があります。これは短期トレンドと中期トレンドの両方が上昇方向であることを示します。

決済時には、基準線が転換線を下抜け、かつ遅行スパンが雲の下にあるという条件を同時に満たす必要があります。これはトレンドが反転したことを示し、ポジションをクローズすべきタイミングです。

戦略のメリット

- 一目均衡表の雲指標でトレンドを判断するため、精度が高い。

- 複数のラインを組み合わせることで、偽のシグナルを抑制できる。

- ロング専用であるため、多くのデジタル通貨の長期的な上昇トレンドに適している。

- 条件フィルターが比較的厳格で、質の高いシグナルを実現できる。

戦略のリスク

- ポジションはフルサイズか空売りのみで、ポジションサイズを調整できない。

- 強気相場では好成績だが、弱気相場では損失リスクが大きい。

- パラメーターのデフォルト設定は暗号通貨向けであり、他の銘柄に適応させるには調整が必要。

- 取引シグナルが少なく、一部の機会を逃しやすい。

戦略の最適化

- ポジション調整機能を追加し、損失が一定割合に達したら一部ポジションをクローズする。

- 売りシグナルを追加し、重要なサポートラインを下回った場合に損切りする。

- パラメーター設定を最適化し、より多くの銘柄に適応させ、安定性を高める。

- ストップロス機能を追加し、損失が閾値に達したら自動的に損切りする。

まとめ

本戦略はロング専用の一目均衡表クラウド取引戦略であり、トレンド判断の精度が高いです。複数の一目均衡ラインをフィルター条件として組み合わせることで、トレンド転換点を比較的信頼性高く判断できます。特に、長期上昇トレンドにある暗号通貨などの銘柄に適しています。ストップロスやポジション調整機能をさらに充実させることで、リスク管理能力が向上し、より多くの銘柄や幅広い市場環境に適応できるようになります。

Source

Pine

/*backtest

start: 2024-01-02 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Simple long-only Ichimoku Cloud Strategy

// Enter position when conversion line crosses base line up, and close it when the opposite happens.

// Additional condition for open / close the trade is lagging span, it should be higher than cloud to open position and below - to close it.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1