双方向適応ボリンジャーバンドトレンドフォロー戦略

1

Follow

1802

Followers

概要

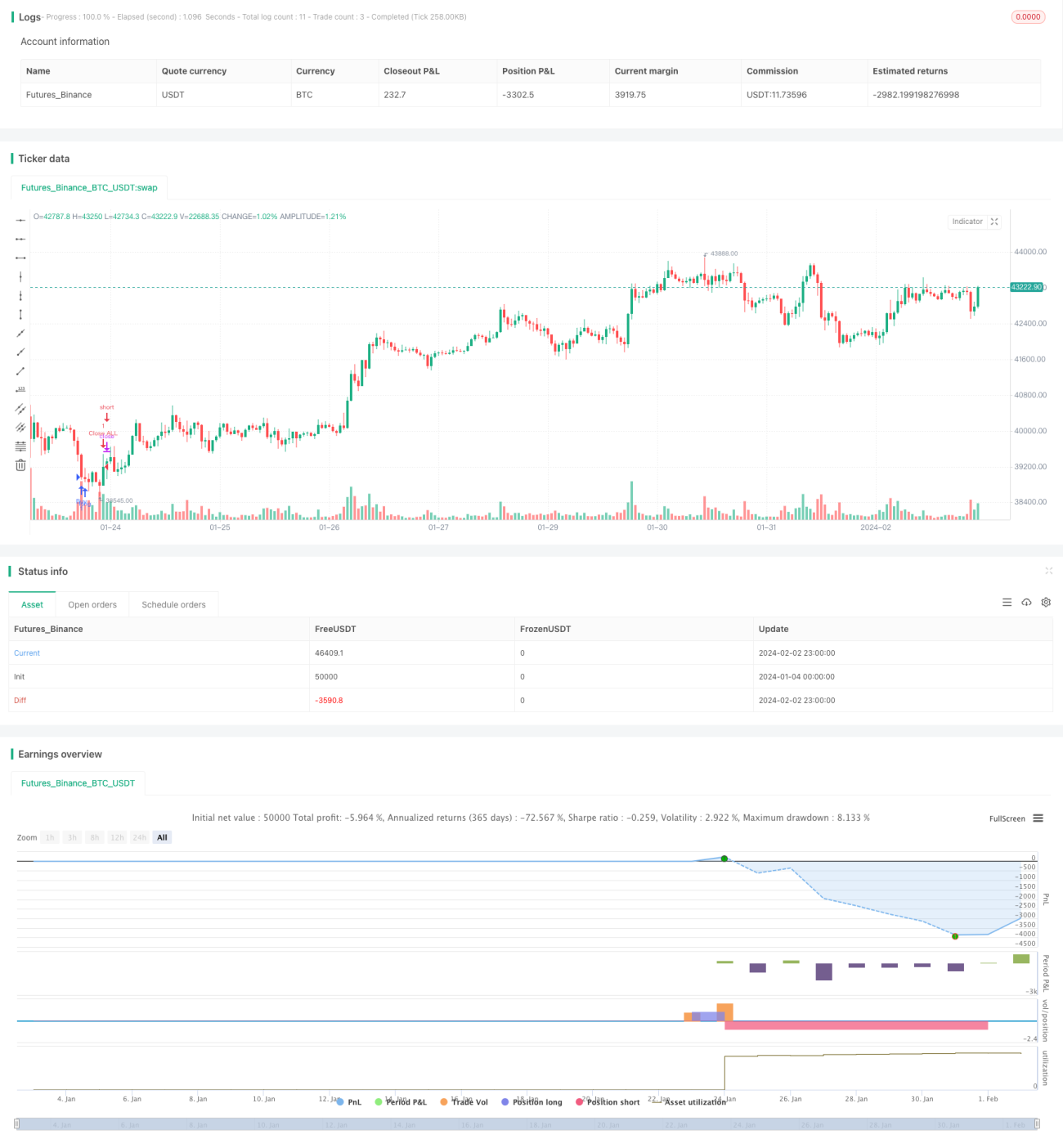

本戦略は、双方向適応型ボリンジャーバンド指標を用いてトレンド方向を識別し、成行注文によるトレーリングストップを組み合わせることで、高効率なトレンドトレードを実現します。

戦略の原理

- 一定期間に基づきボリンジャーバンドの中央線、上限線、下限線を算出

- 価格が上限線を突破した場合はロング方向のトレーリング、下限線を突破した場合はショート方向のトレーリングを開始

- 成行注文で迅速にポジションを構築

- 損切りラインと利確ラインを設定しポジション管理

優位性分析

- 適応型ボリンジャーバンド指標は市場の変動に敏感で、トレンド転換を迅速に判断可能

- 成行注文で素早くエントリーし、スリッページリスクを低減

- 自動で損切り・利確を行い、リスクを厳格に管理し利益を確定

リスク分析

- ボリンジャーバンドは本質的に遅行性があり、偽のブレイクアウトを完全には回避できない

- 成行注文では約定価格をコントロールできない

- 損切りラインと利確ラインの適切な設定が必要

最適化の方向性

- ボリンジャーバンドのパラメータを調整し、トレンド判断の感度を最適化

- 出来高やMACDなどの指標を追加し、偽のブレイクアウトをフィルタリング

- 損切りラインと利確ラインの設定を最適化

まとめ

本戦略は、ボリンジャーバンドによるトレンド方向と変化の判断力を最大限に活用し、迅速な成行注文による双方向トレーリングを組み合わせることで、リスクを管理しながら超過収益を獲得します。ボリンジャーバンドのパラメータをさらに最適化し、補助フィルター指標を追加し、損切り・利確ロジックを調整することで、より優れた戦略パフォーマンスが期待できます。この戦略は明確で実装が容易であり、効率的で信頼性の高いトレンドトレード戦略です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1