ダブルリバーサルモメンタム指数戦略

1

Follow

1802

Followers

概要

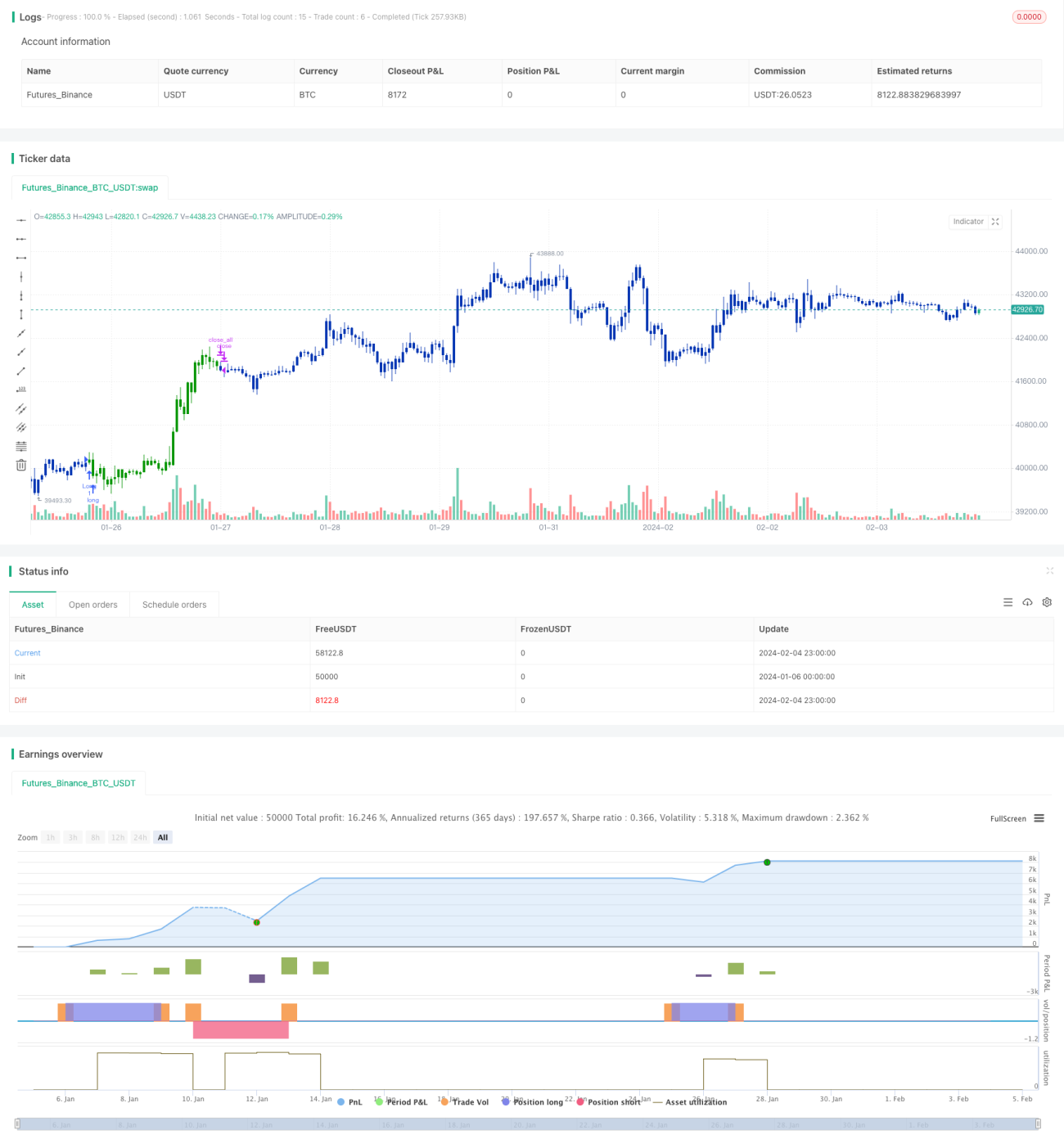

ダブルリバーサルモメンタム指数戦略は、123リバーサル戦略と相対モメンタム指数(RMI)戦略を組み合わせた複合戦略です。二重のシグナルを活用することで、取引判断の精度を高めることを目的としています。

戦略の原理

本戦略は以下の2つの部分で構成されます:

-

123リバーサル戦略

- 前日の終値が前々日より安く、当日の終値が前日より高い、かつ9日スローK線が50未満の場合に買い

- 前日の終値が前々日より高く、当日の終値が前日より安い、かつ9日ファストK線が50超の場合に売り

-

相対モメンタム指数(RMI)戦略

- RMIはRSIにモメンタム要素を加えた変種です。計算式は:RMI = (上昇モメンタムSMA) / (下降モメンタムSMA) * 100

- RMIが買われすぎライン未満の場合に買い、RMIが売られすぎライン超の場合に売り

この複合戦略は、123リバーサルとRMIの二重シグナルが同じ方向を示した場合にのみ取引シグナルを発生させます。これにより誤取引の機会を効果的に減らすことができます。

戦略の優位性分析

本戦略には以下の優位性があります:

- 二重指標の組み合わせによりシグナル精度が向上

- リバーサル戦略を活用し、レンジ相場に適する

- RMI指標は感度が高く、強いトレンドの転換点を識別可能

戦略のリスク分析

本戦略には以下のリスクも存在します:

- 二重フィルターにより一部の取引機会を逃す可能性

- リバーサルシグナルが誤判定される可能性

- RMIパラメータの設定が不適切だと効果が低下

これらのリスクは、パラメータ組み合わせの調整や指標計算方法の最適化により低減できます。

戦略の最適化方向

本戦略は以下の観点からさらに最適化が可能です:

- 異なるパラメータ組み合わせをテストし、最適なパラメータを発見

- KDJ、MACDなど他のリバーサル指標の組み合わせを試す

- RMIの計算式を調整し、より感度を高める

- ストップロス機構を追加し、1回の損失を抑制

- 出来高を組み合わせ、偽シグナルを回避

まとめ

ダブルリバーサルモメンタム指数戦略は、二重シグナルフィルターとパラメータ最適化により、取引判断の精度を効果的に高め、誤シグナルの確率を低減します。レンジ相場に適しており、リバーサル機会を掘り起こせます。本戦略は、パラメータの調整や指標計算の最適化により、効果をさらに強化しリスクを軽減できます。

Source

Pine

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1