RSIに基づく動的追加ポジション戦略

1

Follow

1802

Followers

概要

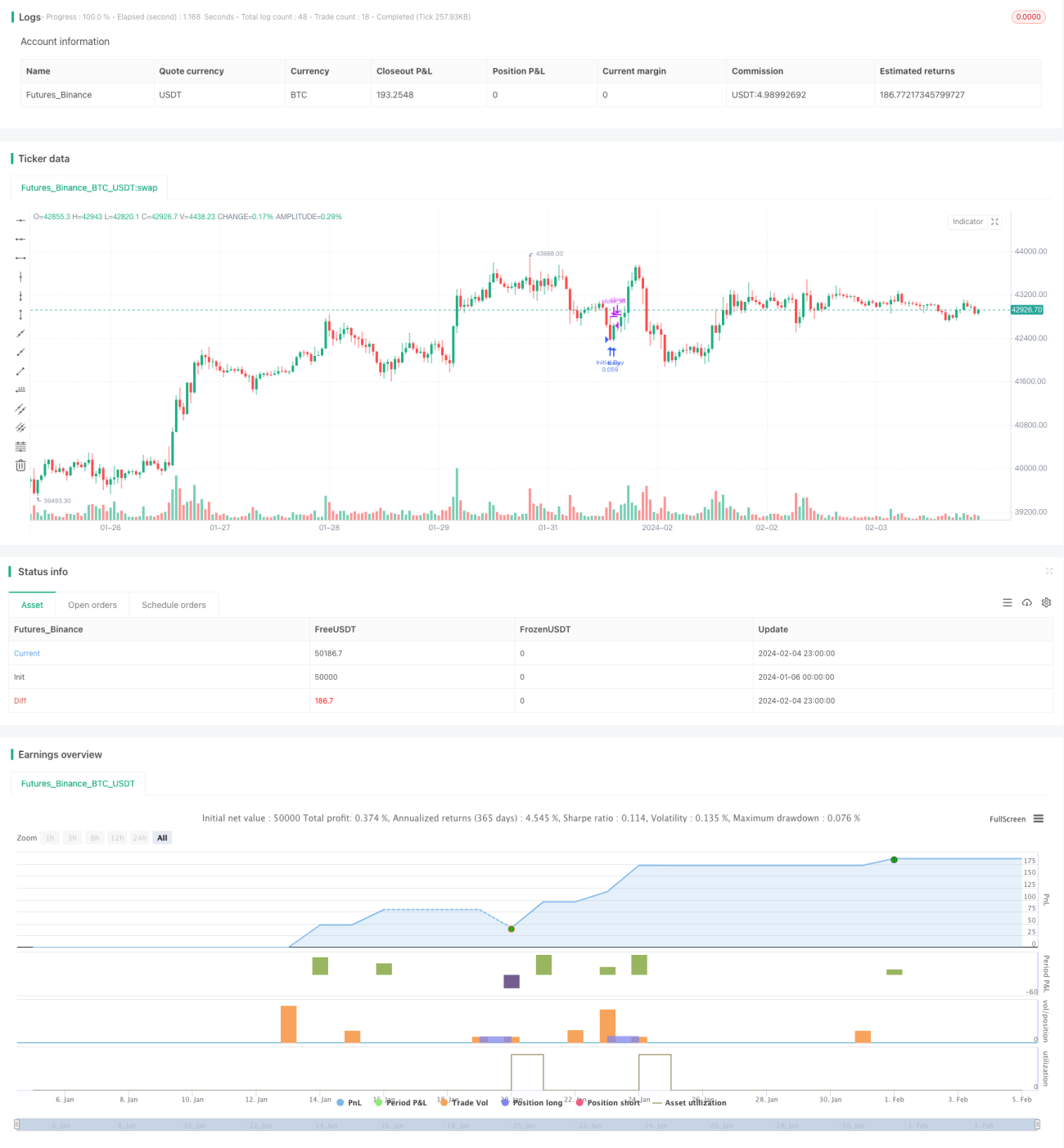

この戦略は、相対力指数(RSI)とマーチンゲールのポジション追加原理を組み合わせたものです。RSIが売られ過ぎラインを下回ったときに初回買い建玉を行い、その後も価格が下落し続ける場合は2の指数でポジションを追加し、利益確定で利食いします。この戦略は高時価総額の仮想通貨の現物取引に適しており、長期的に安定した収益を得ることができます。

戦略の原理

- RSIインジケーターを使用して市場の売られ過ぎを判断し、RSI期間は14、売られ過ぎ閾値は30に設定します。

- RSI < 30の場合、口座残高の5%で初回買い建玉(ロング)を行います。

- 価格が初回エントリー価格より0.5%下落した場合、2倍のロットで買い増し(ロング)します。さらに価格が下落し続ける場合は4倍のロットで再度買い増します。

- 0.5%上昇するごとに、利益確定でポジションをクローズします。

- 上記の手順を繰り返し、サイクル取引を行います。

優位性分析

- RSIを利用して市場の売られ過ぎポイントを判断することで、比較的低い価格でロングエントリーが可能。

- マーチンゲールによるポジション追加により、平均エントリー価格を徐々に下げられる。

- 小さな利確で継続的かつ安定した収益を得られる。

- 高時価総額の仮想通貨の現物取引に適しており、リスク管理が可能。

リスク分析

- 相場が長期低迷した場合、保有ポジションの損失がさらに拡大する可能性がある。

- ストップロスを設定していないため、最大損失を制限できない。

- ポジション追加回数が多すぎると損失がさらに拡大する。

- ロング方向の取引であるため、相場が下落し続けると大きなリスクが残る。

戦略の最適化

- ストップロスポイントを設定し、最大損失を制限することができる。

- RSIのパラメータを最適化し、最適な売られ過ぎ・買われ過ぎシグナルを探す。

- 特定の仮想通貨のボラティリティに応じて適切な利確範囲を設定する。

- 総資産または個別ポジション比率に基づいて追加ロット幅を設定する。

まとめ

本戦略はRSIインジケーターとマーチンゲールのポジション追加原理を組み合わせ、売られ過ぎポイントで適度にポジションを追加してロングし、小さな利確で利益を得ます。継続的で安定した収益を得ることができる一方、一定のリスクも存在します。ストップロスの設定やパラメータ調整などにより、さらに最適化することができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1