動的傾斜トレンドライン取引戦略

概要

本戦略の核となる考え方は、動的な傾き(ダイナミックスロープ)を用いて価格のトレンド方向を判断し、ブレイクアウト判定を組み合わせて取引シグナルを生成することです。具体的には、価格の新高値・新安値をリアルタイムで追跡し、異なる時間帯の価格変化から動的傾きを計算し、さらに価格がトレンドラインをブレイクしたかどうかを基にロング/ショートのシグナルを判断します。

戦略の仕組み

本戦略は主に以下のステップで構成されています。

-

高値・安値の判定:一定期間(例:20本のローソク足)内の最高値・最安値を追跡し、新高値・新安値かどうかを判定します。

-

動的傾きの計算:新高値または新安値を付けたローソク足の番号を記録し、その高値・安値から一定期間(例:9本のローソク足)後の高値・安値までの動的傾きを計算します。

-

トレンドラインの描画:動的傾きに基づいて上昇トレンドラインと下降トレンドラインを描画します。

-

トレンドラインの延長・更新:価格がトレンドラインをブレイクした場合、トレンドラインを延長・更新します。

-

取引シグナル:価格がトレンドラインをブレイクしたかどうかを基に、ロングとショートのシグナルを判断します。

戦略の利点

本戦略には以下の利点があります。

-

トレンドの方向を動的に判断するため、市場の変化に柔軟に対応できる。

-

ストップロスを適切に管理でき、ドローダウンが小さい。

-

ブレイクアウトによる取引シグナルが明確で、実装が簡単。

-

パラメータをカスタマイズでき、適応性が高い。

-

コード構造が明確で、理解や二次開発が容易。

リスクと対策

本戦略には以下のリスクがあります。

-

トレンドがレンジ相場の場合、ダマシが多くなる可能性があるため、フィルター条件を追加することを推奨。

-

ブレイクアウトの偽シグナルが多い可能性があるため、パラメータの調整やフィルター条件の追加で対応可能。

-

急激な値動き時にストップロスのリスクがあるため、ストップロス幅を広げることができる。

-

最適化の余地が限られ、収益性が制限されるため、短期取引に適している。

最適化の方向性

本戦略の最適化可能な点は以下の通りです。

-

より多くのテクニカル指標を追加してシグナルをフィルタリングする。

-

パラメータの組み合わせを最適化し、最適なパラメータを探す。

-

ストップロス戦略の改良を試み、リスクを低減する。

-

自動でエントリー幅を調整する機能を追加する。

-

他の戦略と組み合わせて、さらなる機会を発掘する。

まとめ

本戦略は全体として、動的傾きに基づいてトレンドを判断し、ブレイクアウトで取引する効率的な短期戦略です。判断精度が高く、リスクは管理可能で、市場における短期のチャンスを捉えるのに適しています。パラメータのさらなる最適化やフィルター条件の追加により、勝率と収益性を向上させることができます。

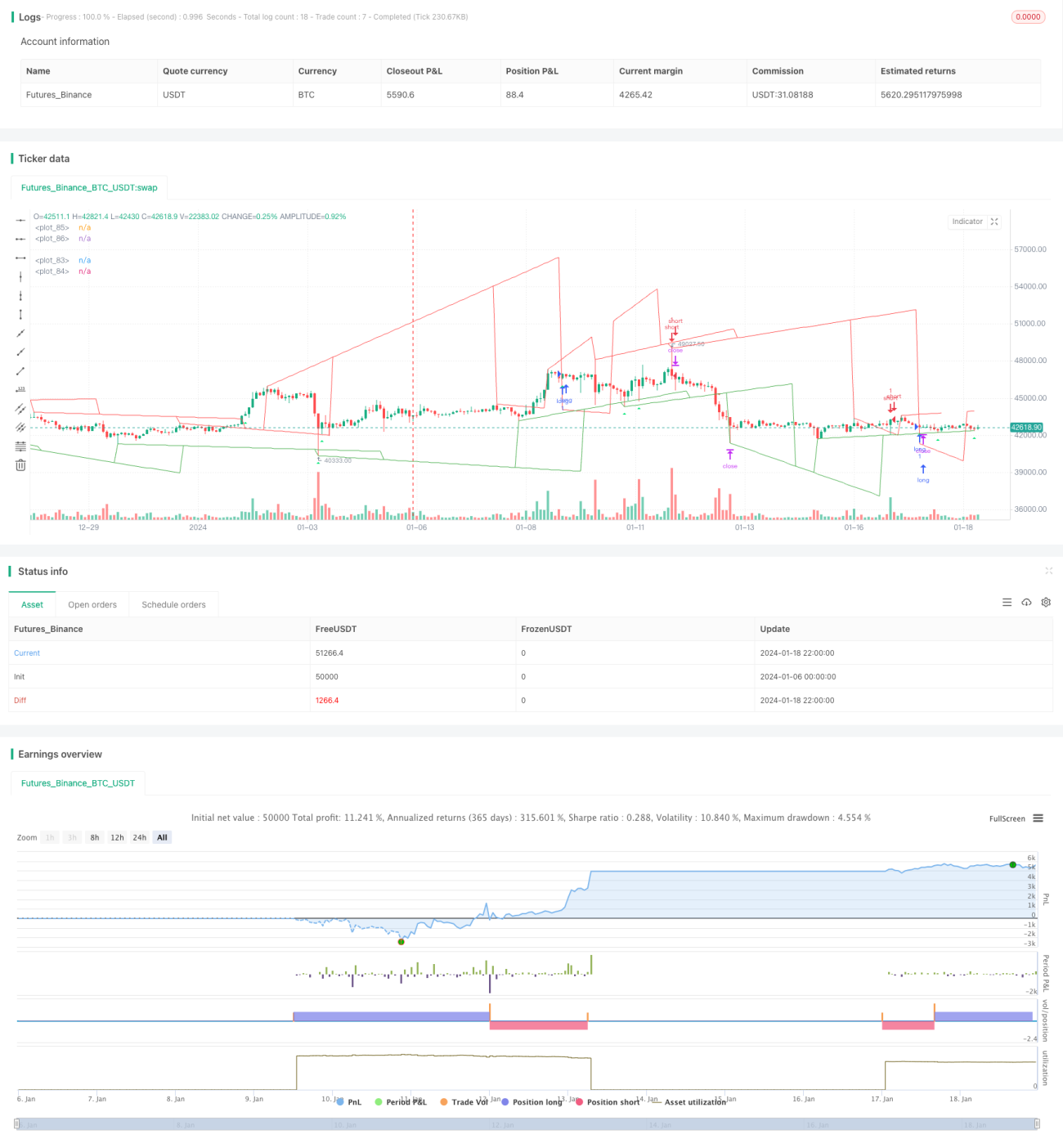

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1