ダブルボトム反転移動平均線DCAグリッド戦略

概要

ダブルボトム反転移動平均線DCAグリッド戦略は、主に移動平均線による価格反転とDCA戦略を活用し、グリッド状に段階的にポジションを構築します。ダブルボトム反転の形状に基づいて反転の機会を判断します。反転形状が発生した後、複数の異なる価格の注文を用いて、DCAを組み合わせて段階的にグリッドポジションを構築します。

戦略の原理

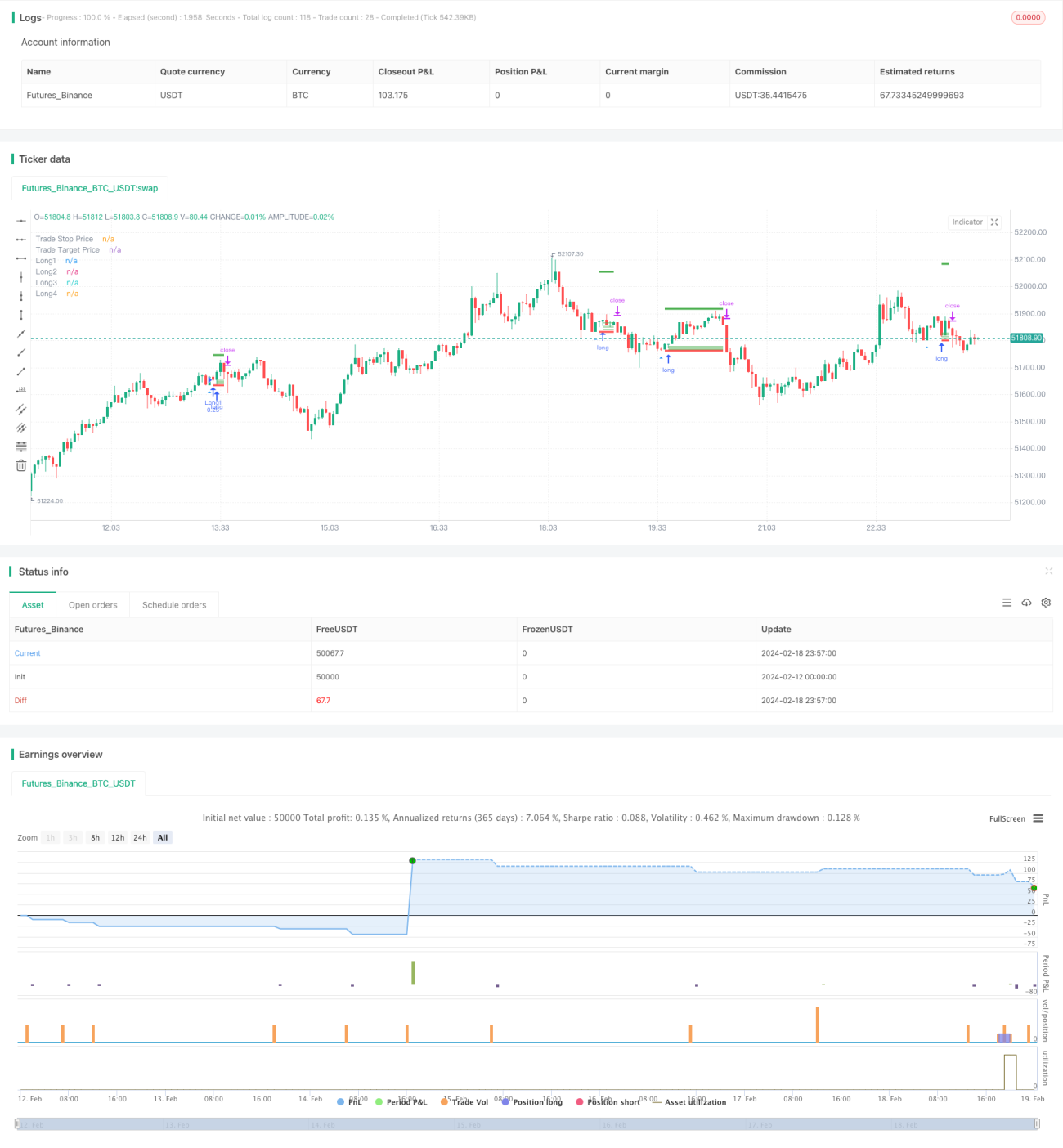

本戦略はまず、ローソク足に連続して2本の終値が等しい底(いわゆる「ダブルボトム」)が出現するかを判定します。ダブルボトムが検出された場合、価格が反転する可能性があると判断します。このとき、戦略は底値付近に複数の指値注文を設定します。これらの指値注文の価格はATRとボラティリティに基づいて計算され、グリッド区間を形成します。これによりDCAの効果が得られ、トレーダーは反転後の異なる価格帯で段階的にポジションを構築できます。

具体的には、まずta.atrで直近14本のローソク足のATR指標を計算し、直近5本のローソク足で価格ボラティリティを計算します。これらがグリッド区間を決定する主要パラメータです。グリッド区間は4つの価格ポイントで構成され、それぞれ底値+ボラティリティ、底値+0.75倍ボラティリティ、…と続きます。ダブルボトム条件がトリガーされた後、この計算式に従い対応する価格に4つの指値注文を設定します。各注文の数量は均等です。約定しなかった注文は、設定されたローソク足数経過後に自動的にキャンセルされます。

さらに、戦略はストップロスと利確ラインも設定します。ストップロス価格はダブルボトムの最安値から最小ティックを引いた値、利確価格はエントリー価格+ATR指標の5倍です。ポジションが0でない場合、これらの価格はリアルタイムで更新されます。

優位性分析

本戦略には以下の優位性があります:

- ダブルボトムを利用して反転タイミングを判断することで、ダマシのブレイクアウトを効果的に回避できます。

- DCAグリッド設計により、トレーダーは異なる価格で段階的にポジションを構築でき、ポジションコストを低減できます。

- ATRとボラティリティのパラメータにより、グリッドと利確の範囲を動的に調整でき、市場の変化に適応できます。

- 自動ストップロス機能により、1回の損失を効果的に抑制できます。

リスク分析

主なリスクは以下の通りです:

- 価格が反転せず、ダブルボトムのサポートラインを直接下回る可能性があります。この場合ストップロスが発動され、損失が発生します。ストップロス幅を適度に拡大することで対策可能です。

- DCAグリッド区間の設定が適切でない場合、ほとんどの注文が約定しない可能性があります。異なるパラメータでテストし、約定率を確保する必要があります。

- 市場が激しく変動する場合、利確が頻繁にトリガーされる可能性があります。利確倍率を適度に拡大することを検討してください。

最適化の方向性

本戦略は以下の方向で最適化が可能です:

- トレンド判断を追加し、上昇トレンドでのみ反転操作を行うことで、大きなトレンドを見逃すのを防ぎます。

- 初回のポジションを大きくし、後続のグリッドポジションを段階的に減らすことで、資金効率を最適化することを検討します。

- 異なるパラメータの組み合わせをテストし、最適なパラメータを見つけます。動的パラメータを設計し、市場の状況に応じてリアルタイムで調整することも可能です。

- 高度なプラットフォームで機械学習を統合し、パラメータの自動最適化を実現することも考えられます。

まとめ

ダブルボトム反転移動平均線DCAグリッド戦略は、価格形状、移動平均線指標、グリッド取引など複数のテクニカル手法を総合的に活用しています。タイミングの正確さ、コストの制御可能性、下落時の保護など多くの利点を持ちます。本戦略にはまだ大きな最適化余地があり、深く研究し応用する価値があります。パラメータを適切に調整すれば、レンジ相場で良好な結果を得ることができます。

- 1