多指標テクニカル定量取引戦略

1

Follow

1802

Followers

概要

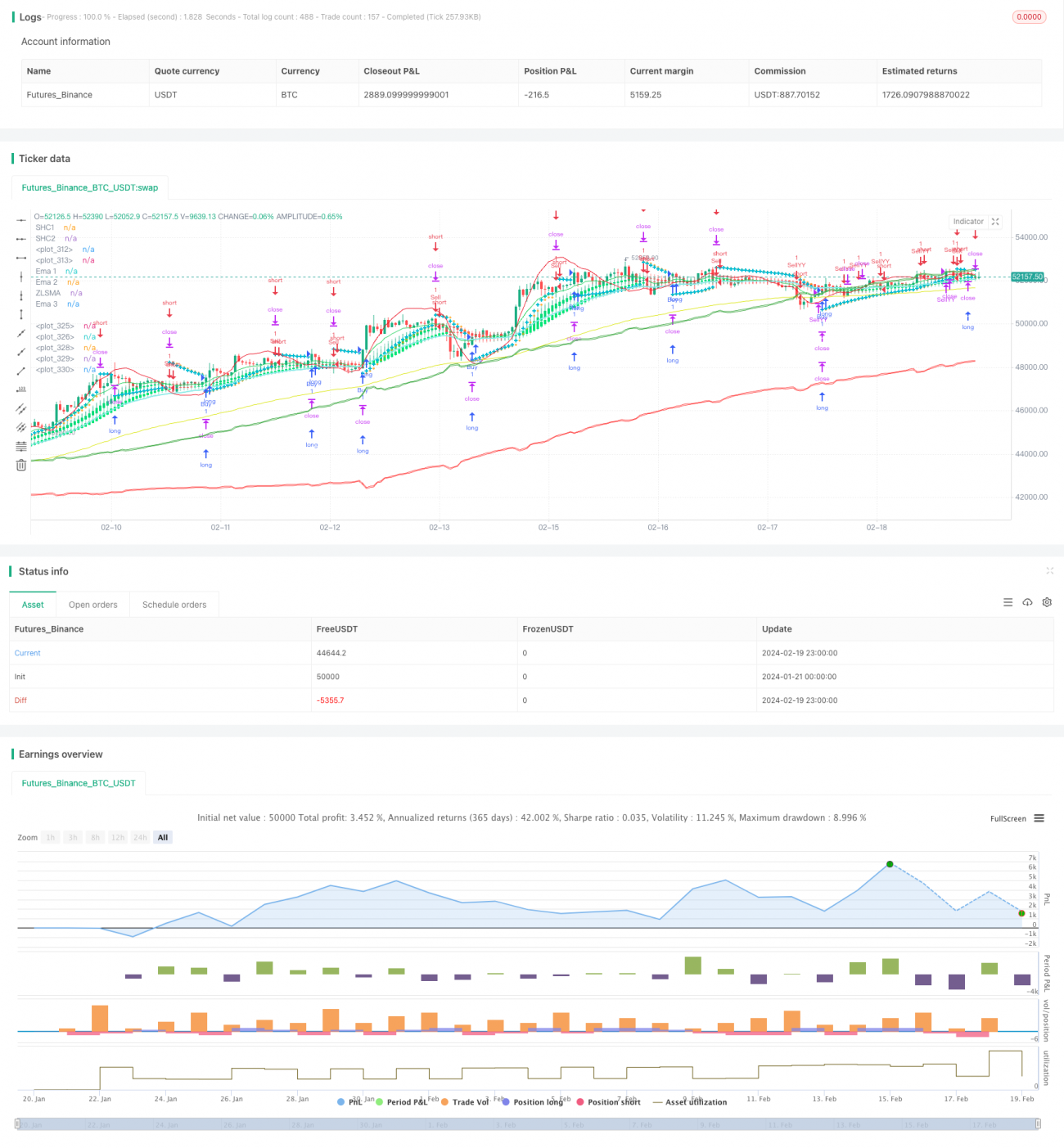

本戦略は、パラボリックSAR(放物線状転換システム)、纏論出口(チャン理論エグジット)、ゼロラグ単純移動平均線、指数移動平均線、順応移動平均線など、複数のテクニカル指標を総合的に活用し、チャート上での潜在的な買いシグナルと売りシグナルを特定します。

戦略の原理

主な指標

- パラボリックSAR(放物線状転換システム):ストップロス水準と潜在的エントリーポイントの決定に使用

- 纏論出口戦略(チャン理論エグジット):トレンド方向の特定に使用

- ゼロラグ単純移動平均線:低ラグの移動平均線を提供

- 指数移動平均線:価格トレンドと変動を追跡

- 平滑移動平均線:より平滑化された移動平均線を生成

取引シグナル

- パラボリックSARが上昇トレンドを示し、価格が第99指数移動平均線を上回った場合にロング(買い)。下降トレンドを示し、価格が第99指数移動平均線を下回った場合にショート(売り)。

- 纏論出口戦略のシグナルと組み合わせ、トレンド方向をさらに確認。

- 平滑移動平均線をパラボリックシグナルと組み合わせ、偽のブレイクアウトを回避。

リスク管理

- ストップロスとテイクプロフィットの設定。

- 購入条件のリセットを考慮し、ポジションを柔軟に調整。

優位性分析

本戦略の最大の強みは、指標の組み合わせが包括的であり、トレンド方向を効果的に識別できる点です。パラボリックシステムは潜在的反転ポイントを特定し、纏論出口戦略は主要トレンドを判断し、移動平均線は偽シグナルをフィルタリングします。複数の指標が相互に検証することで、シグナルの正確性が大幅に向上します。

さらに、戦略にはリスクをコントロールするためのストップロスとテイクプロフィットの仕組みが組み込まれています。平滑移動平均線は短期ノイズの干渉も回避します。これらの要因により、本戦略は非常に安定性の高いものとなっています。

リスク分析

多くの指標判断に依存するため、これらの指標から矛盾するシグナルが発せられた場合、本戦略は困難に直面する可能性があります。また、パラメータ設定が適切でない場合、取引に悪影響を及ぼす可能性もあります。

さらに、テクニカル面での取引自体に一定のリスクが伴い、損失を完全に回避することはできません。慎重に操作し、盲目的に追随することは避けるべきです。

最適化の方向性

- 指標パラメータのテストと最適化を実施し、最適な組み合わせを見つける。

- 機械学習アルゴリズムを導入し、ビッグデータを活用したモデルトレーニングにより、シグナルの正確性をさらに向上させる。

- 感情指標やニュースなどの情報を組み合わせて市場状況を判断し、ポジションサイズやストップロスラインを動的に調整する。

- 購入条件リセットのロジックを最適化し、シグナル検出をより柔軟かつ一貫性のあるものにする。

まとめ

本戦略は複数のテクニカル指標を統合し、指標の組み合わせにより取引シグナルを識別します。シグナルの正確性が高く、安定性に優れていることが強みです。同時に、リスク管理策も適切に整備されています。総じて、検討に値する取引アプローチです。今後、パラメータ最適化、モデルトレーニング、感情指標の導入などを通じて、さらに改善が可能です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1