점진적 축적 돌파 거래 전략

개요

점진적 축적 돌파 거래 전략은 시장의 축적 및 분배 단계를 식별하고, 빅터 분석 원리를 사용하며, 새총 패턴 및 반전 패턴 판단을 보조로 하여 잠재적인 매수 및 매도 기회를 찾습니다.

전략 원리

-

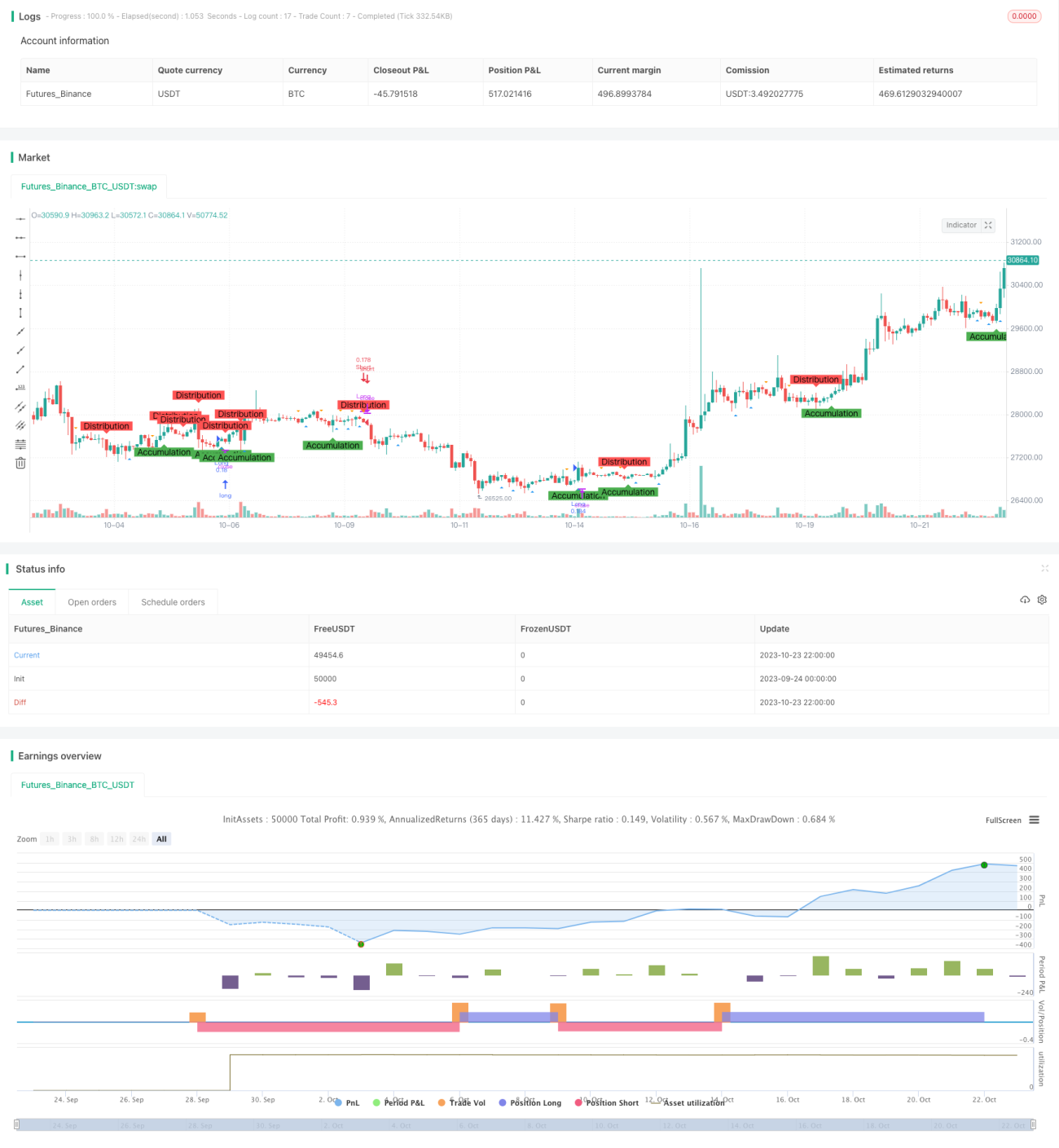

서로 다른 길이의 이동평균선 교차를 사용하여 축적 및 분배 단계를 식별합니다. 종가가 AccumulationLength 길이의 이동평균선을 상향 돌파하면 축적 단계로 판단하고, 종가가 DistributionLength 길이의 이동평균선을 하향 돌파하면 분배 단계로 판단합니다.

-

서로 다른 길이의 이동평균선 교차를 사용하여 새총 패턴과 반전 패턴을 식별합니다. 저점이 SpringLength 길이의 이동평균선을 상향 돌파하면 새총 패턴으로 판단하고, 고점이 UpthrustLength 길이의 이동평균선을 하향 돌파하면 반전 패턴으로 판단합니다.

-

축적 단계에서 새총 패턴이 관찰되면 매수하고, 분배 단계에서 반전 패턴이 관찰되면 매도합니다.

-

손절 수준을 설정합니다. 매수 포지션의 손절가는 종가 × (1 - 손절 비율%), 매도 포지션의 손절가는 종가 × (1 + 손절 비율%)입니다.

-

차트에 축적 단계, 분배 단계, 새총 패턴 및 반전 패턴을 표시하여 패턴 식별을 용이하게 합니다.

장점 분석

-

빅터 분석 방법을 사용하여 시장의 힘을 비축하는 축적 및 분배 단계를 식별함으로써 거래 신호의 신뢰성을 높일 수 있습니다.

-

새총 패턴과 반전 패턴을 결합하여 거래함으로써 거래 신호를 추가로 검증할 수 있습니다.

-

손절 설정을 통해 개별 거래 손실을 효과적으로 통제할 수 있습니다.

-

차트에 표시를 하면 비축(축적) 형성의 전체 과정을 명확하게 관찰할 수 있습니다.

-

이 전략의 매개변수는 조정 가능하므로 다양한 시장 및 거래 주기에 맞게 최적화할 수 있습니다.

위험 분석

-

횡보 장세(집합 시세)로 인해 이동평균선 신호가 잘못된 신호를 보낼 수 있습니다.

-

새총 패턴과 반전 패턴이 실패할 수 있습니다.

-

손절가가 돌파되면 손실이 증가할 수 있습니다.

-

다른 시장에 맞게 매개변수를 조정해야 하며, 부적절할 경우 거래 신호 오류가 발생할 수 있습니다.

-

기계적 거래 시스템의 백테스트 시간이 유연하지 않을 수 있으므로 수동 모니터링이 필요합니다.

최적화 방향

-

다양한 시장 및 주기에서 매개변수의 최적 조합을 테스트할 수 있습니다.

-

거래량 요소를 추가하여 거래 신호를 확인하는 것을 고려할 수 있습니다.

-

동적 손절을 설정하여 시장 변동성에 따라 손절 수준을 조정할 수 있습니다.

-

기본적 요소를 추가하여 중요한 시점에서 잘못된 거래를 피할 수 있습니다.

-

머신러닝 알고리즘을 추가하여 매개변수를 동적으로 최적화할 수 있습니다.

요약

점진적 축적 돌파 거래 전략은 빅터 분석, 이동평균선 지표, 패턴 인식 등 다양한 기술적 분석 방법을 통합하여 시장의 힘 비축을 효과적으로 식별하고 거래 신호를 생성합니다. 이 전략은 신뢰할 수 있는 거래 신호, 통제 가능한 위험, 명확한 시각적 표현 등의 장점이 있습니다. 그러나 기계적 거래 시스템으로서 백테스트 시간과 매개변수 적응성은 아직 개선이 필요합니다. 향후 최적화 방향은 매개변수 조합 최적화, 거래량 확인, 손절 최적화, 주요 기본적 요소 포함 등입니다. 전반적으로 이 전략은 데이 트레이딩(단기 거래)에 효과적인 의사 결정 지원을 제공합니다.

- 1