1-3-1 빨간색-초록색 캔들 반전 전략

개요

1-3-1 빨강-초록 캔들 반전 전략은 캔들 패턴을 기반으로 매매 신호를 판단하는 전략입니다. 이 전략은 1개의 빨간 캔들이 3개의 초록 캔들에 의해 반전되는지 관찰하여 매수 기회를 찾습니다.

원리

해당 전략의 핵심 로직은 다음과 같습니다:

- 현재 캔들이 빨간 캔들인지, 즉 종가가 시가보다 낮은지 확인

- 이전 3개의 캔들이 모두 초록 캔들인지, 즉 종가가 시가보다 높은지 확인

- 마지막 초록 캔들의 종가가 앞의 2개 초록 캔들보다 높은지 확인

- 위 조건을 만족하면 빨간 캔들 종가에서 시장가로 매수

- 손절가는 빨간 캔들의 최저가로 설정

- 익절가는 진입가에 진입가와 손절가의 차이를 더한 값으로 설정

이 전략을 통해 빨간 캔들이 반전되는 상황에서 매수할 수 있으며, 이후 추세가 상승할 가능성이 높습니다. 동시에 손절과 익절을 설정하여 리스크를 관리하고 수익을 확정합니다.

장점 분석

1-3-1 빨강-초록 캔들 반전 전략은 다음과 같은 장점이 있습니다:

- 전략 로직이 단순하고 명확하여 이해와 구현이 용이

- 캔들 패턴 특성을 활용하며 어떤 지표에도 의존하지 않아 과도한 최적화 문제를 피함

- 명확한 진입 및 청산 규칙으로 객관적 실행 가능

- 손절과 익절 설정으로 각 거래의 위험-수익 비율 통제 가능

- 백테스트 결과가 양호하며 실전 적용 가능성이 높음

위험 분석

해당 전략에는 다음과 같은 위험도 존재합니다:

- 캔들 패턴이 미래 추세를 100% 예측할 수 없어 일정한 불확실성 존재

- 한 번만 매수하므로 개별 종목 특성으로 인해 승률이 낮을 수 있음

- 시장 전반의 흐름을 고려하지 않아 지수가 지속 하락할 때 보유 리스크가 큼

- 거래 비용과 슬리피지를 고려하지 않아 실전 효과가 다를 수 있음

대책:

- 이동평균선 등의 지표를 결합하여 신호를 필터링해 매수 성공률을 높일 수 있음

- 포지션 관리를 조정하여 분할 매수

- 지수 상황에 따라 손절 위치를 동적으로 조정하거나 거래 중단

- 다양한 손절 및 익절 비율 설정을 테스트

- 거래 비용을 포함한 실전 효과 테스트

최적화 방향

해당 전략은 다음 측면에서 최적화할 수 있습니다:

-

지수 기반 필터링. 지수의 단기 및 중기 추세에 따라 거래 신호를 필터링하여 지수 상승 시 매수, 하락 시 거래 중단.

-

거래량 확인. 초록 캔들의 거래량을 추가로 판단하여 거래량이 증가한 경우에만 매수.

-

손절 및 익절 비율 최적화. 다양한 손절 및 익절 비율을 테스트하여 최적의 파라미터 조합을 찾음. 동적 손절 또는 트레일링 스탑도 설정 가능.

-

포지션 관리 최적화. 분할 매수 후 조건 충족 시 추가 매수하여 단일 거래 리스크를 낮춤.

-

추가 필터 조건 도입. 이동평균선, 변동성 등의 지표를 고려하여 추세가 더 명확해질 때 매수.

-

빅데이터 학습을 통한 최적 파라미터 탐색. 대량의 과거 데이터를 수집하고 머신러닝 등의 기술을 사용하여 최적의 파라미터 임계값을 학습.

요약

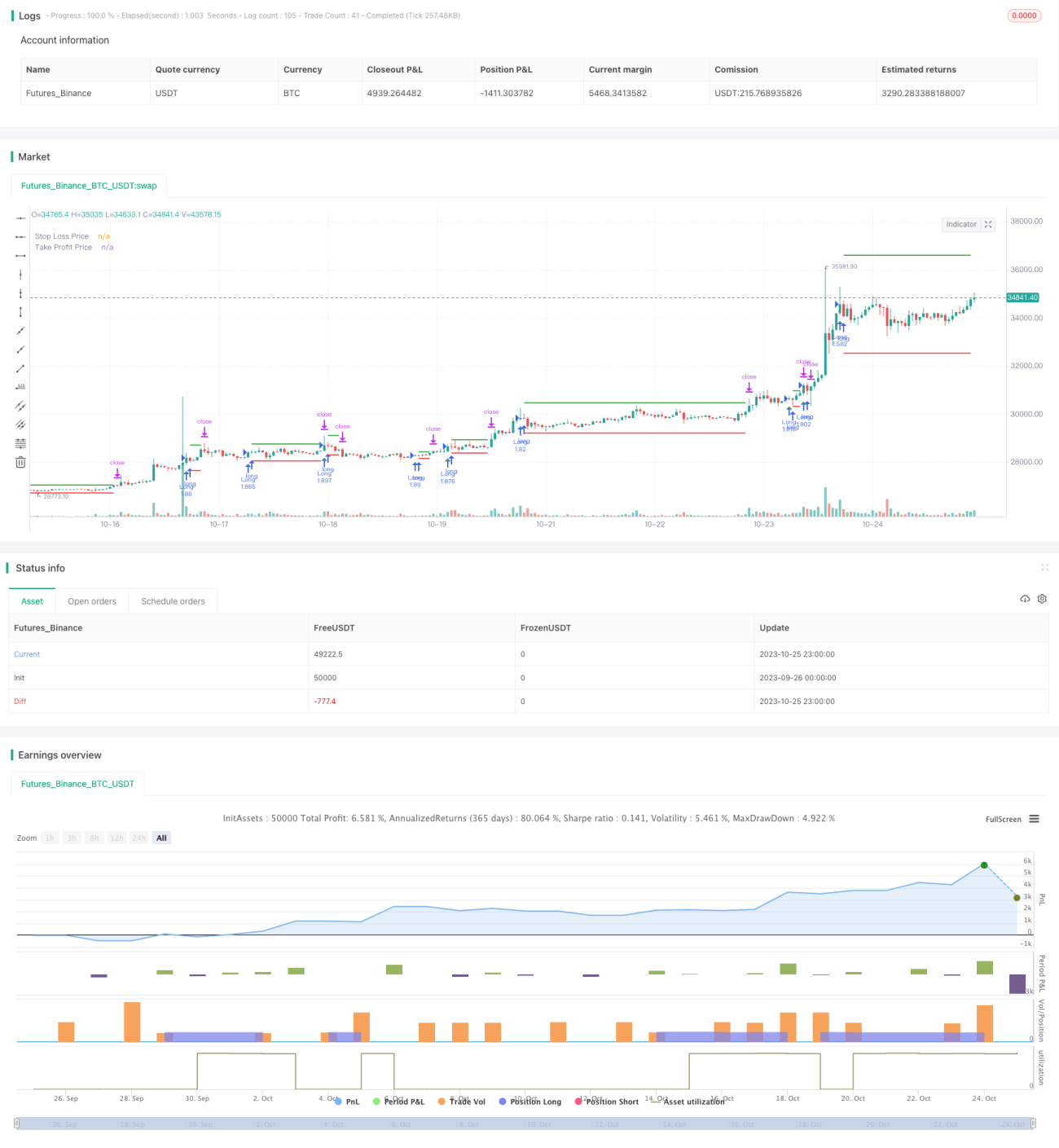

1-3-1 빨강-초록 캔들 반전 전략은 전반적으로 단순하고 실용적인 단기 매매 전략입니다. 명확한 진입 및 청산 규칙을 가지고 있으며 백테스트 성과가 양호합니다. 몇 가지 최적화 조치를 통해 실전 효과를 향상시켜 신뢰할 수 있는 퀀트 매매 전략으로 만들 수 있습니다. 동시에 위험 관리를 주의하고 자금을 적절히 운용해야 합니다.

/*backtest

start: 2023-09-26 00:00:00

end: 2023-10-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//by Genma01

strategy("Stratégie tradosaure 1 Bougie Rouge suivi de 3 Bougies Vertes", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1