개요

라이온 크랙 균형 전략은 이동평균선 교차를 기반으로 한 간단한 단기 트레이딩 전략입니다. 이 전략은 주로 두 개의 이동평균선을 사용하며, 빠른 이동평균선이 느린 이동평균선을 아래에서 위로 교차할 때 매수하고, 빠른 이동평균선이 느린 이동평균선을 위에서 아래로 교차할 때 포지션을 청산합니다. 전략명은 트레이딩 업계에서 유행하는 "라이온 크랙"이라는 용어에서 유래했으며, 단기 가격의 미세한 움직임을 포착하여 좁은 이동평균선 크랙에서 수익을 얻는 것을 의미합니다.

전략 원리

이 전략은 두 개의 이동평균선을 사용합니다: 빠른 이동평균선 smallMAPeriod와 느린 이동평균선 bigMAPeriod입니다. 두 이동평균선은 가격 채널을 형성하며, 채널 하단은 빠른 이동평균선, 채널 상단은 느린 이동평균선입니다. 가격이 아래에서 위로 채널 하단(빠른 이동평균선)을 돌파할 때 매수하고, 가격이 위에서 아래로 채널 상단(느린 이동평균선)을 하향 돌파할 때 청산합니다.

구체적으로, 전략은 먼저 빠른 이동평균선 smallMA와 느린 이동평균선 bigMA를 계산합니다. 그런 다음 채널 하단 매수선 buyMA를 계산하는데, 이는 느린 이동평균선의 (100 - percentBelowToBuy)%입니다. 빠른 이동평균선 smallMA가 아래에서 위로 매수선 buyMA를 돌파할 때 매수하고, 수익이 1%에 도달하거나 수익이 없지만 포지션을 7개 캔들 동안 보유한 후 청산합니다.

종합하면, 이 전략은 이동평균선의 "라이온 크랙", 즉 채널 하단 돌파 기회를 포착하여 단기 수익을 실현하려고 합니다. 동시에 이익 실현 및 손절 조건을 설정하여 각 거래의 위험을 통제합니다.

장점 분석

이 전략의 장점은 다음과 같습니다:

-

개념이 간단하여 이해하고 구현하기 쉽습니다. 이중 이동평균선 교차는 가장 기본적인 기술 지표 전략입니다.

-

백테스트가 쉽습니다. 이 전략은 TradingView의 자체 백테스트 기능을 직접 사용하므로 별도 구현이 필요 없습니다.

-

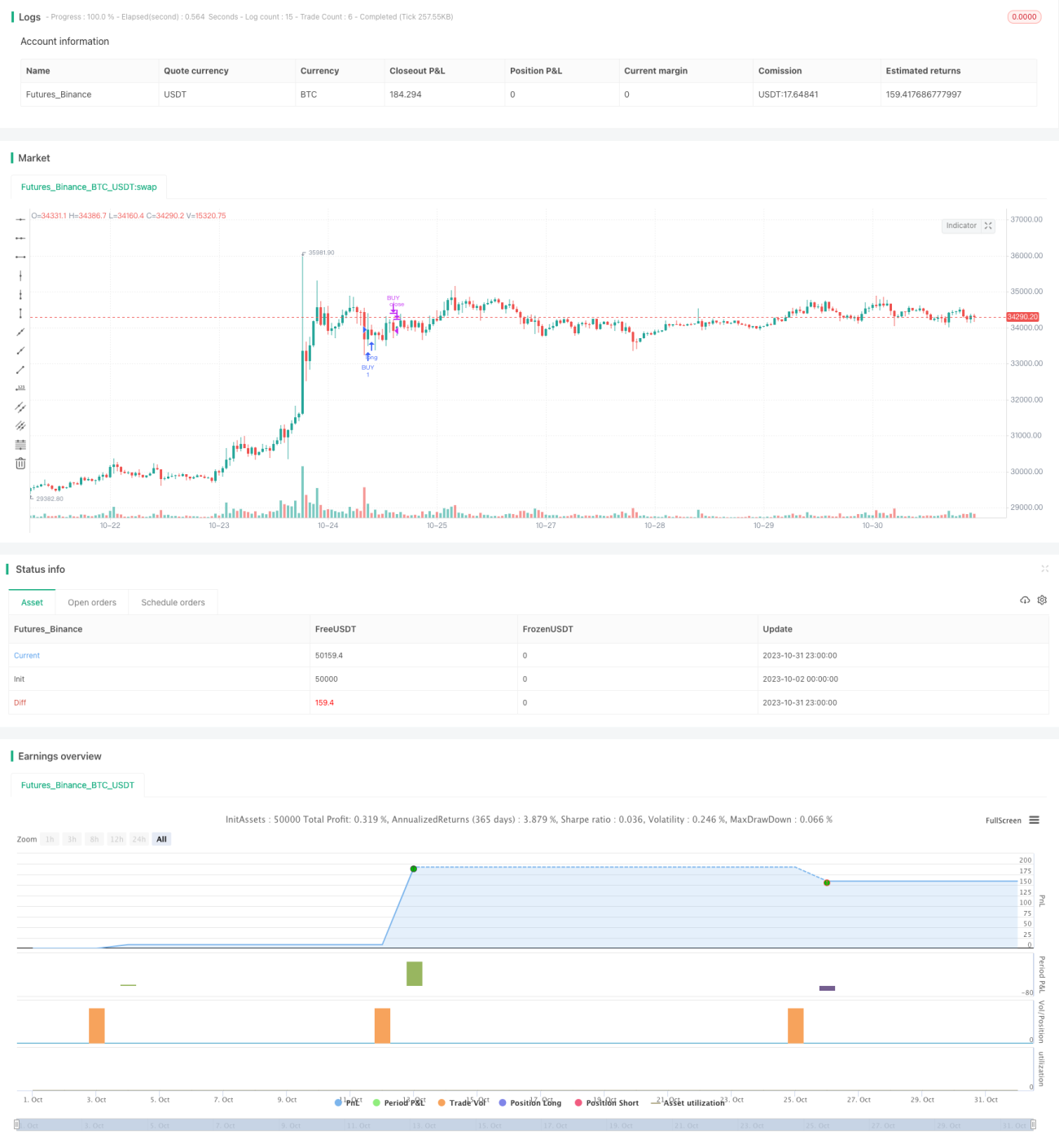

시각화가 뛰어납니다. TradingView를 사용하면 차트에 거래 신호 지점과 백테스트 통계 데이터를 직접 표시할 수 있습니다.

-

위험 통제가 가능합니다. 전략에 이익 실현 및 손절 조건이 설정되어 있어 각 거래의 손실을 효과적으로 통제할 수 있습니다.

-

유연한 조정이 가능합니다. 사용자는 자신의 필요에 따라 이동평균선 매개변수 및 기타 기술 지표를 조정하여 전략을 다양한 상품과 트레이딩 스타일에 맞출 수 있습니다.

위험 분석

이 전략에는 다음과 같은 위험도 존재합니다:

-

과도한 신호가 발생할 수 있습니다. 이중 이동평균선 전략은 횡보장에서 여러 번의 잘못된 신호를 생성하기 쉽습니다.

-

단일 지표에 의존합니다. 이동평균선 교차만을 의사 결정에 사용하고 다른 요소를 무시하므로 신호 품질이 낮을 수 있습니다.

-

매개변수 최적화가 어렵습니다. 이동평균선 주기 매개변수 조합을 최적화하려면 많은 계산이 필요하며, 최적의 매개변수를 찾기 어렵습니다.

-

백테스트 편향이 있습니다. 단순한 이중 이동평균선 전략의 백테스트 결과는 실제 거래보다 좋은 경우가 많습니다.

-

손절이 어렵습니다. 고정된 손절 지점을 설정하면 시장 변화에 대응하기 어렵습니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

-

다른 지표(예: 거래량, 변동성 등)를 결합하여 신호를 필터링하고 횡보장에서 무효 신호가 발생하는 것을 방지합니다.

-

추세 기반 판단을 추가하여 역추세 거래를 피합니다. 더 긴 주기의 이동평균선을 도입하여 추세 방향을 판단할 수 있습니다.

-

머신러닝을 사용하여 최적의 매개변수를 찾습니다. 순차적 매개변수 최적화 또는 유전 알고리즘을 사용하여 더 나은 매개변수 조합을 자동으로 탐색합니다.

-

손절 전략을 추가합니다. 예를 들어 트레일링 스탑, 이동 스탑 등을 사용하여 손절에 탄력성을 부여합니다.

-

진입 타이밍을 최적화합니다. 다른 지표를 사용하여 더 효과적인 진입 시점을 식별할 수 있습니다.

-

정량적 연구를 통해 매개변수 조합을 백테스트 최적화하여 안정성을 높입니다.

-

자동 매매 시스템을 개발하여 프로그래밍 방식 거래로 매개변수 조합 최적화 및 전략 평가를 수행합니다.

요약

라이온 크랙 균형 전략은 초보자가 학습하기에 매우 적합한 입문 전략입니다. 간단한 이중 이동평균선 교차 원리를 사용하고 이익 실현 및 손절 규칙을 설정하여 단기 가격 변동을 포착할 수 있습니다. 이 전략은 이해하고 구현하기 쉬우며 백테스트 결과도 좋습니다. 하지만 최적화 난이도가 높고 실제 거래 효과는 의문입니다. 다른 기술 지표 도입, 매개변수 최적화, 자동 매매 시스템 개발 등을 통해 이 전략을 개선할 수 있습니다. 전반적으로 라이온 크랙 균형 전략은 정량적 트레이딩 초보자에게 매우 좋은 학습 플랫폼을 제공합니다.

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TraderHalai

// This script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

//- 1