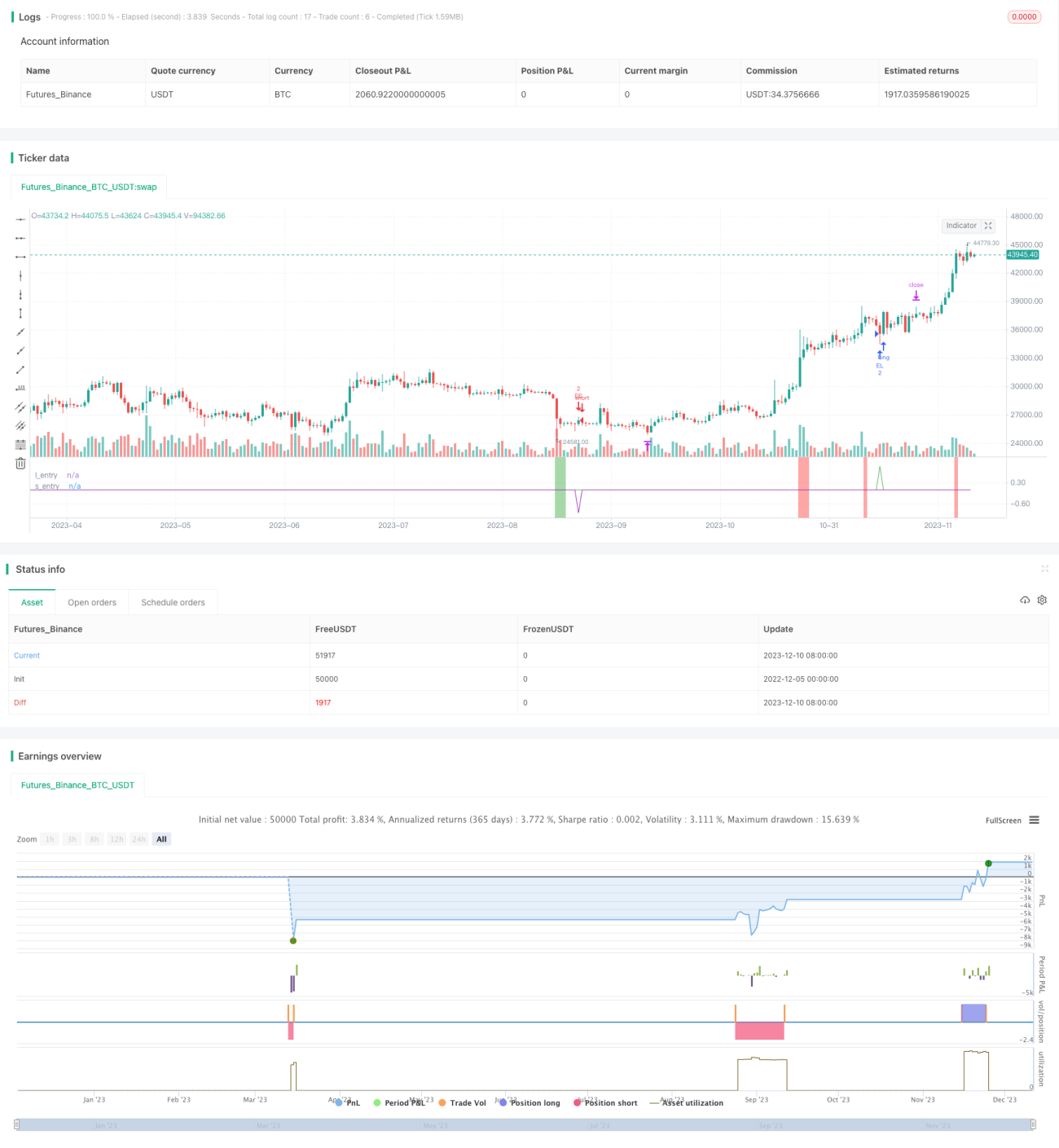

개요

모멘텀 풀백 전략(Momentum Pullback Strategy)은 RSI 극단값을 모멘텀 신호로 식별하는 롱/숏 포지션 전략입니다. 대부분의 RSI 전략과 달리, 이 전략은 극단적인 RSI 수치 방향으로 첫 번째 풀백을 찾아 진입합니다.

5일 EMA(최저가)/5일 EMA(최고가)의 첫 번째 풀백 지점에서 매수/매도 포지션을 취하고, 롤링 12개 캔들의 최고점/최저점에서 청산합니다. 이 롤링 고점/저점 메커니즘은 가격이 장기 횡보에 진입하면, 새로운 캔들이 나타날 때마다 이익 실현 목표가 낮아짐을 의미합니다. 최적의 거래는 일반적으로 2-6개 캔들 내에서 완료됩니다.

권장 손절 거리는 진입 가격의 X배 ATR(사용자 입력 매개변수에서 조정 가능)입니다.

이 전략은 다양한 시간 프레임과 시장에 대해 강건성이 높으며, 승률은 60%-70% 사이이고 수익 거래 규모가 상대적으로 큽니다. 중요 경제 뉴스로 인한 변동성에서 신호가 생성되지 않도록 주의해야 합니다.

전략 원리

-

6일 RSI 값을 계산하여 90 이상(과매수) 및 10 이하(과매도)의 극단점을 찾습니다.

-

RSI가 과매수일 때, 6개 캔들 내에서 5일 EMA(최저선)로 풀백하여 매수 진입합니다.

-

RSI가 과매도일 때, 6개 캔들 내에서 5일 EMA(최고선)로 풀백하여 매도 진입합니다.

-

출구 전략은 이동 이익 실현입니다. 롱 포지션은 과거 12개 캔들의 최고점을 첫 번째 출구 목표로 하고, 이후 새로운 캔들이 나타나면 새로운 12개 캔들 최고점으로 업데이트하여 롤링 출구를 구현합니다. 숏 포지션은 반대로 롤링 12개 캔들 최저점으로 손절합니다.

-

손절 거리는 진입 가격의 X배 ATR이며, 사용자 정의 가능합니다.

장점 분석

이 전략은 RSI 극단값을 모멘텀 신호로 활용하고 풀백 진입을 결합하여 추세의 잠재적 반전 지점을 포착할 수 있으며 승률이 높습니다.

이동 이익 실현 메커니즘을 활성화하여 실제 가격 움직임에 따라 일부 이익을 고정하고 하락 폭을 줄일 수 있습니다.

ATR 손절은 단일 거래 손실을 효과적으로 제어할 수 있습니다.

강한 강건성으로 다양한 시장과 매개변수 조합에 적용 가능하며 실제 거래에 쉽게 복제할 수 있습니다.

위험 분석

ATR 값이 너무 크게 설정되면 손절 거리가 너무 멀어져 단일 손실이 확대될 수 있습니다.

만약 ██╗ 횡보가 발생하면, 이동 이익 실현 메커니즘이 수익 공간을 축소시킵니다.

풀백 거리가 너무 깊어 6개 캔들을 초과하면 진입 기회를 놓칠 수 있습니다.

중요 경제 이벤트가 발생하면 거래가 슬리피지나 가짜 돌파를 겪을 수 있습니다.

최적화 방향

진입 캔들 수를 줄이는 것을 테스트할 수 있습니다. 예를 들어 6개에서 4개 캔들로 조정하여 진입 성공률을 높입니다.

ATR 배수를 늘리는 것을 테스트하여 단일 손절을 더욱 제어할 수 있습니다.

거래량 지표를 결합하여 횡보 다이버전스로 인한 손실을 피할 수 있습니다.

풀백이 60분 차트의 중앙선을 돌파한 후에 진입하여 일부 노이즈를 걸러낼 수 있습니다.

요약

모멘텀 풀백 전략은 전반적으로 매우 실용적인 단기 캐치 전략입니다. 이 전략은 추세, 반전, 손절 등 다양한 측면을 결합하여 편리한 실전 운영이 가능하면서도 일정한 알파를 가지고 있습니다. 매개변수 조정과 다른 지표 결합을 통해 안정성을 더욱 향상시킬 수 있습니다. 전반적으로 이 전략은 퀀트 트레이딩의 큰 축복이며 배우고 활용할 가치가 있습니다.

- 1