인내심 있는 추세 추종 전략

개요

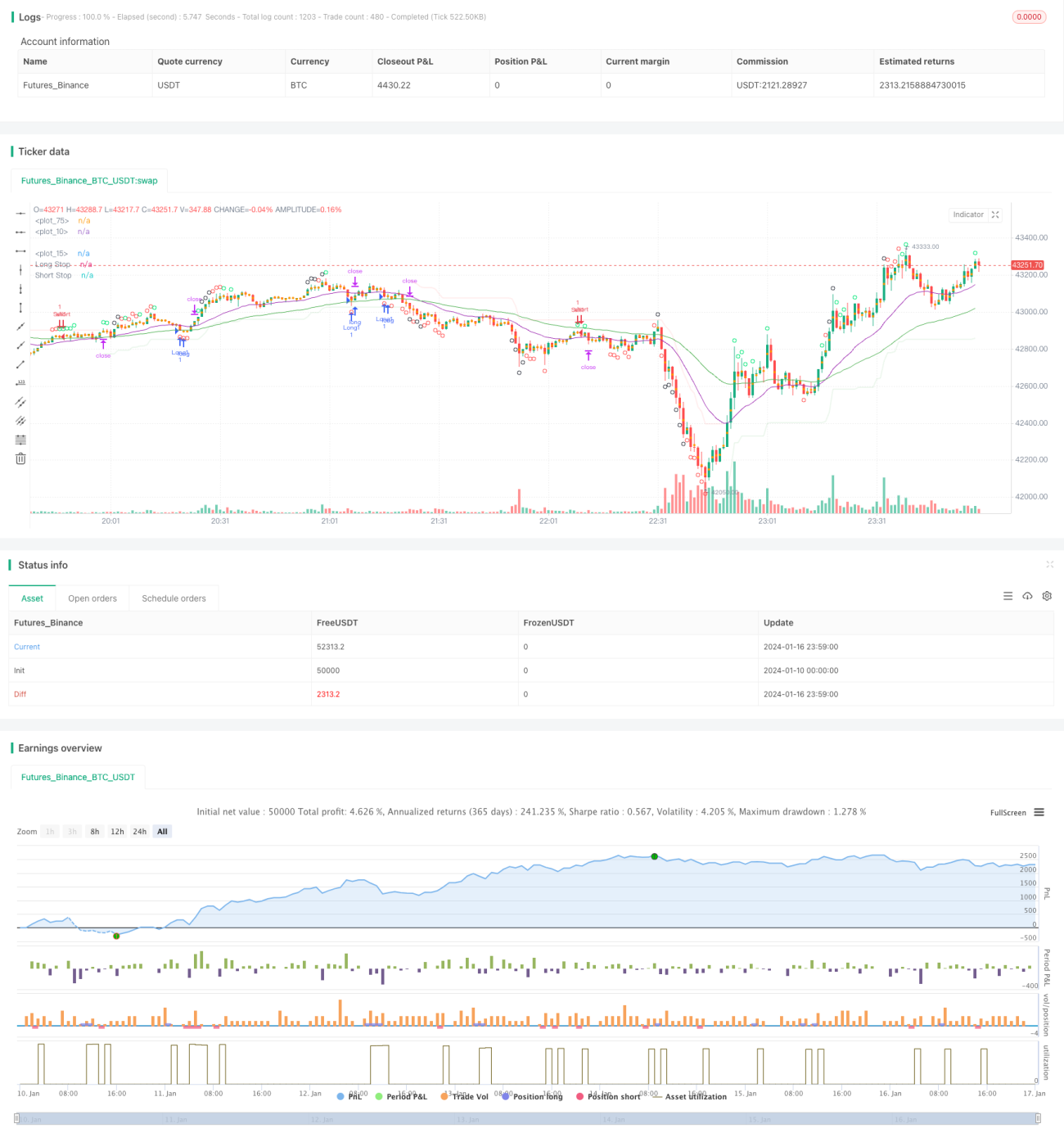

인내심 추세 추적 전략(耐心追踪趋势策略)은 추세 추종형 전략입니다. 이동평균선의 지표 조합을 사용하여 추세 방향을 판단하고, 과매수/과매도 지표인 CCI를 결합하여 매매 신호를 발생시킵니다. 이 전략은 큰 추세를 추구하며, 횡보장에서 효과적으로 물림을 피할 수 있습니다.

전략 원리

이 전략은 21주기와 55주기 EMA 조합을 사용하여 추세 방향을 판단합니다. 단기 EMA가 장기 EMA 위에 있을 때 상승 추세로 정의하고, 단기 EMA가 장기 EMA 아래에 있을 때 하락 추세로 정의합니다.

CCI 지표는 과매수/과매도 상황을 판단하는 데 사용됩니다. CCI가 -100선을 상향 돌파하면 바닥 과매도 신호, 100선을 하향 돌파하면 천장 과매수 신호입니다. CCI 지표의 다양한 과매수/과매도 선에 따라 전략은 세 가지 매매 신호 강도 수준으로 구분됩니다.

상승 추세로 판단될 때 CCI 지표가 강력한 바닥 과매도 신호를 발생시키면 롱 포지션에 진입합니다. 하락 추세로 판단될 때 CCI 지표가 강력한 천장 과매수 신호를 발생시키면 숏 포지션에 진입합니다.

손절선은 SuperTrend 지표로 설정되고, 목표 이익은 고정된 포인트로 설정됩니다.

장점 분석

이 전략의 주요 장점은 다음과 같습니다:

- 큰 추세를 추적하여 물림 방지

- CCI 지표가 반전 지점을 효과적으로 판단

- SuperTrend 손절선 설정이 합리적

- 고정 손절 및 고정 이익실현으로 위험 통제 가능

위험 분석

이 전략의 주요 위험은 다음과 같습니다:

- 큰 추세 판단 오류 가능성

- CCI 지표의 가짜 신호 발생 가능성

- 손절점이 너무 얕거나 깊어 불필요한 손절 발생 가능성

- 고정 이익실현으로 추세 지속 이익을 추구하기 어려운 가능성

이러한 위험에 대응하기 위해 EMA 주기 파라미터, CCI 파라미터, 손절 및 이익실현 포인트를 조정하여 최적화할 수 있습니다. 또한 더 많은 지표를 도입하여 전략 신호를 검증하는 것도 필요합니다.

최적화 방향

이 전략의 최적화 방향은 주로 다음과 같습니다:

- 더 많은 지표 조합을 테스트하여 더 나은 추세 판단 및 신호 검증 지표를 찾습니다.

- ATR을 사용한 동적 손절 및 이익실현을 통해 추세 추적과 위험 통제를 개선합니다.

- 과거 데이터를 기반으로 훈련된 머신러닝 모델을 도입하여 추세 확률을 판단합니다.

- 다양한 종목에 맞춰 파라미터를 조정하여 최적화합니다.

요약

인내심 추세 추적 전략은 전체적으로 매우 실용적인 추세 추종 전략입니다. 이동평균선을 사용하여 큰 추세 방향을 판단하고, CCI 지표로 반전 지점 신호를 발견하며, 슈퍼트렌드 손절선이 합리적으로 설정됩니다. 파라미터 조정과 다중 지표 조합 검증을 통해 이 전략은 더욱 최적화될 수 있으며, 장기적인 실전 매매 추적 검증을 통해 확인할 가치가 있습니다.

- 1