단일 추세 변동 돌파 전략

개요

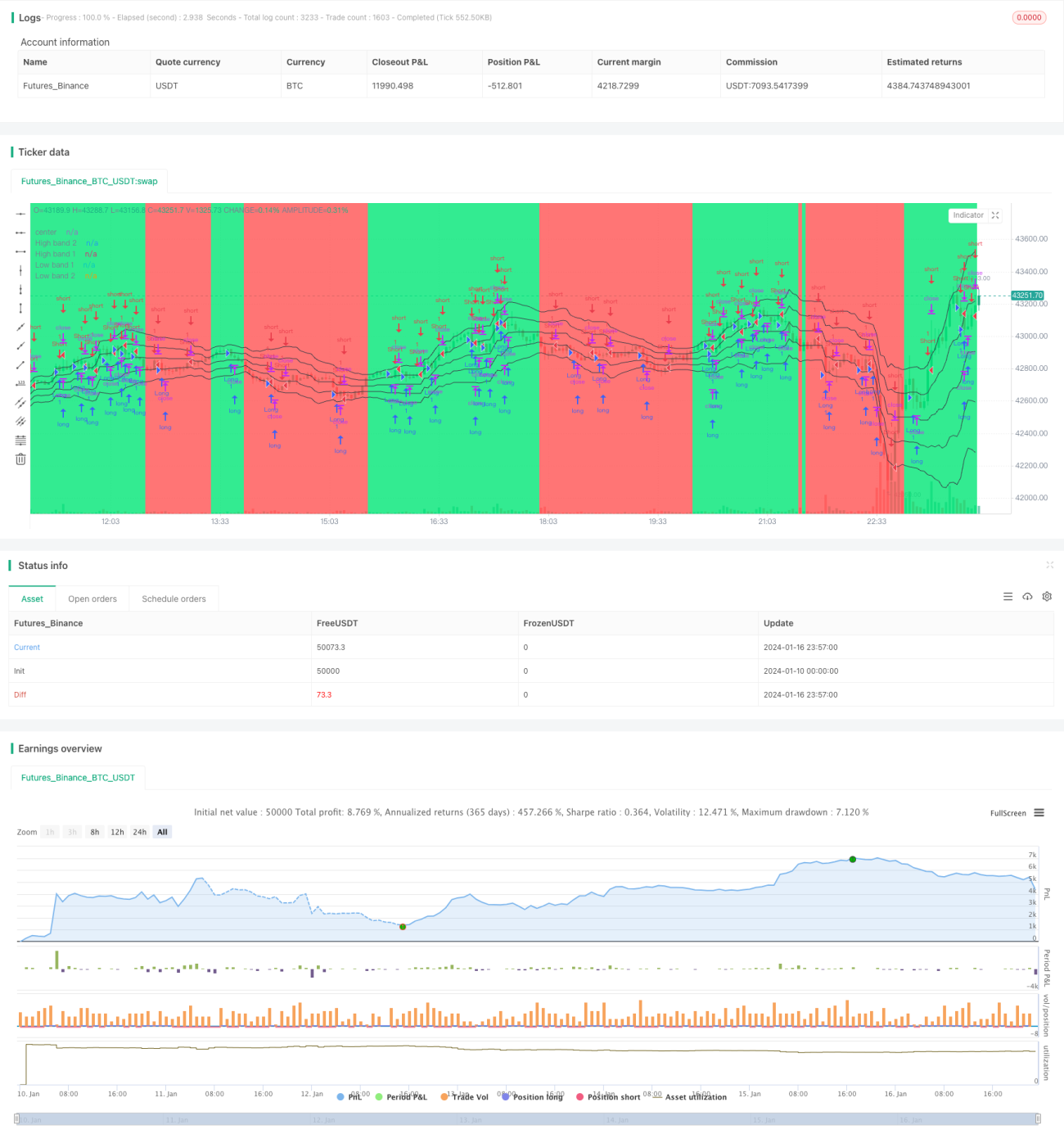

단일 추세 변동 돌파 전략(Single Side Trend Shock Breakout Strategy)은 가격 채널과 추세 판단을 활용한 돌파 전략입니다. 추세 방향을 식별하고, 변동 구간 돌파 시 진입하여 설정된 이익 목표에 도달하면 청산하는 것을 목표로 합니다.

전략 원리

이 전략은 가격 채널의 상하단을 계산하여 가격이 채널을 돌파하는지 여부를 판단하여 매매를 실행합니다. 구체적으로, 전략은 먼저 최근 N기간의 최고가와 최저가를 계산하고 가격 중간선을 산출합니다. 그런 다음 가격과 중간선의 평균 절대 거리를 계산하여 상하단을 구합니다.

추세를 판단할 때, 전략은 최근 몇 개의 캔들이 모두 채널 위(매수 신호) 또는 채널 아래(매도 신호)에 있는지 확인합니다. 추세가 확인되면 전략은 가격이 변동하기를 기다리며, 채널 상단 또는 하단 근처에서 돌파가 발생하여 신호를 형성할 때 반대 방향으로 진입합니다.

또한, 전략은 캔들 몸통 돌파를 보조 진입 신호로 사용합니다. 몸통 길이가 평균 몸통 길이의 일정 배수를 초과하면 신호가 발생합니다. 전략은 진입 후 이익 목표를 설정하고 가격이 목표에 도달하면 능동적으로 이익을 확정합니다.

장점 분석

이 전략은 다음과 같은 장점이 있습니다:

- 가격 채널을 이용한 추세 방향 판단으로 가짜 돌파 확률 감소

- 반대 방향 진입으로 추세 변동 구간에서 수익 창출 가능

- 몸통 돌파를 보조 신호로 활용하여 진입 정확도 향상

- 이익 목표 설정으로 능동적인 이익 확정

위험 분석

이 전략은 다음과 같은 위험도 존재합니다:

- 가격 채널 매개변수 설정이 부적절하면 채널 범위가 너무 넓거나 좁아질 수 있음

- 강한 추세에서 반대 방향 매매는 큰 손실을 초래할 수 있음

- 몸통 돌파는 가짜 신호를 형성하기 쉬움

- 이익 목표 설정이 부적절하면 일부 수익을 놓칠 수 있음

위험을 줄이기 위해 매개변수를 조정하여 채널 범위를 좁히고, 강한 추세에서 반대 방향 포지션을 피하며, 이익 확정 로직을 최적화하는 등의 방법을 사용할 수 있습니다.

최적화 방향

이 전략은 다음과 같은 방향으로 최적화할 수 있습니다:

- 추세 판단 지표 추가로 추세 판단 정확도 향상

- 몸통 돌파 매개변수 최적화로 가짜 신호율 감소

- 더 많은 지표 결합으로 진입 시점 필터링

- 동적 이익 목표 조정

요약

단일 추세 변동 돌파 전략은 가격 채널과 추세 판단을 통해 변동 구간에서 반대 방향으로 포지션을 구축하여 수익을 얻습니다. 추세 판단과 능동적인 이익 확정이라는 장점이 있지만, 일부 위험도 존재합니다. 여러 지표 확인, 매개변수 최적화 등을 통해 위험을 줄이고 수익 공간을 확대할 수 있습니다. 이 전략은 단기 매매에 적합하며, 추세 전략의 보완으로 사용할 수 있습니다.

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Scalper Strategy v1.5", shorttitle = "Scalper str 1.5", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

- 1