RSI 지표 흡반 매매전략

개요

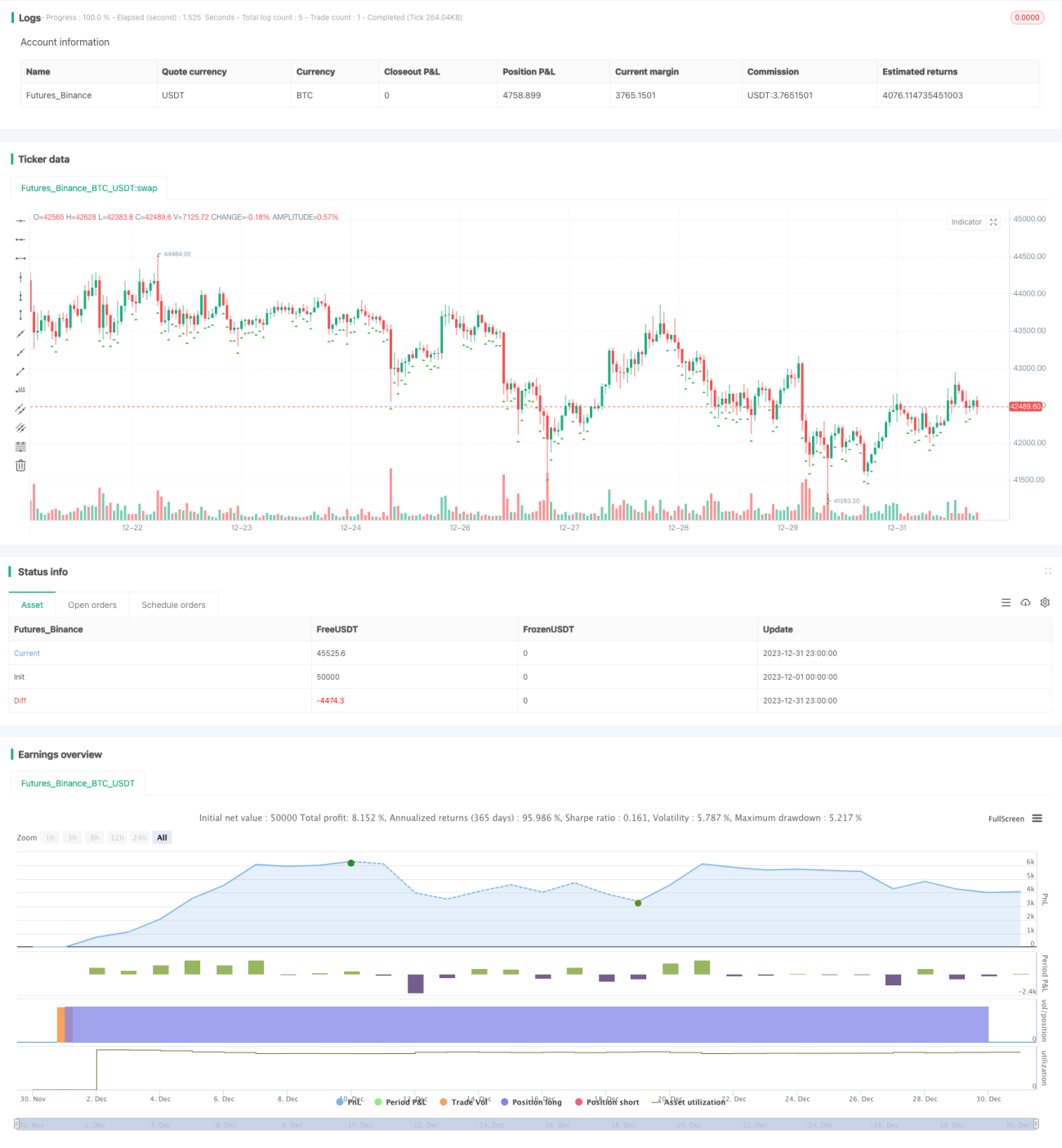

RSI 지표 흡입 거래 전략은 RSI와 CCI 지표를 통합한 고정 그리드 거래 방법입니다. 이 전략은 RSI와 CCI 지표의 값을 기반으로 진입 시점을 판단하고, 고정 수익 비율과 고정 그리드 수량을 사용하여 이익 실현 주문과 추가 주문을 설정합니다. 또한, 돌파성 가격 변동에 대한 헤지 메커니즘도 통합되어 있습니다.

전략 원리

진입 조건

5분 및 30분 RSI 지표가 모두 설정된 임계값보다 낮고, 1시간 CCI 지표도 설정값보다 낮을 때 매수 신호가 발생합니다. 이때 현재 종가(close)를 진입 가격으로 기록하고, 계정 자본과 그리드 수량에 따라 첫 번째 포지션의 수량을 계산합니다.

이익 실현 조건

진입 가격을 기준으로 설정된 목표 수익 비율에 따라 수익 가격을 계산하고, 해당 가격 수준에 이익 실현 주문을 설정합니다.

추가 주문 조건

첫 번째 주문 외에 나머지 고정 포지션 추가 주문은 진입 신호 후 하나씩放出(放出)되어 설정된 그리드 수량에 도달할 때까지 진행됩니다.

헤지 메커니즘

가격이 진입 가격보다 설정된 헤지 임계값 비율 이상 상승하면, 모든 보유 포지션을 헤지 청산합니다.

반전 메커니즘

가격이 진입 가격보다 설정된 반전 임계값 비율 이상 하락하면, 모든 미체결 주문을 취소하고 새로운 진입 기회를 기다립니다.

장점 분석

- RSI와 CCI 두 가지 지표를 결합하여 수익 확률을 높임

- 고정 그리드로 목표 수익을 설정하여 수익 확실성 증가

- 헤지 메커니즘을 통합하여 급격한 가격 변동 위험을 효과적으로 방어

- 반전 메커니즘을 추가하여 손실을 줄일 수 있음

위험 분석

- 지표의 오신호 발생 확률

- 급격한 가격 변동으로 헤지 임계값 돌파

- 반전 후 다시 방향 전환 시 재진입 불가능

지표 매개변수 조정, 헤지 폭 확대, 반전 폭 축소를 통해 이러한 위험을 줄일 수 있습니다.

최적화 방향

- 더 다양한 지표 조합 테스트 가능

- 적응형 이익 실현 메커니즘 연구 가능

- 추가 주문 로직 최적화 가능

요약

RSI 지표 흡입 거래 전략은 지표를 통해 진입 시점을 판단하고, 고정 그리드 이익 실현 및 추가 주문을 사용하여 안정적인 수익을 확보합니다. 동시에 전략은 급격한 변동에 대한 헤지와 반전 후 재진입 메커니즘을 갖추고 있습니다. 이러한 여러 메커니즘을 통합한 전략은 거래 위험을 낮추고 수익률을 높이는 데 사용될 수 있습니다. 지표 및 매개변수 설정을 추가로 최적화하면 더 나은 실전 성과를 얻을 수 있습니다.

- 1