다중 기간 SMA 지표 기반의 추세 추종 전략

1

Follow

1802

Followers

개요

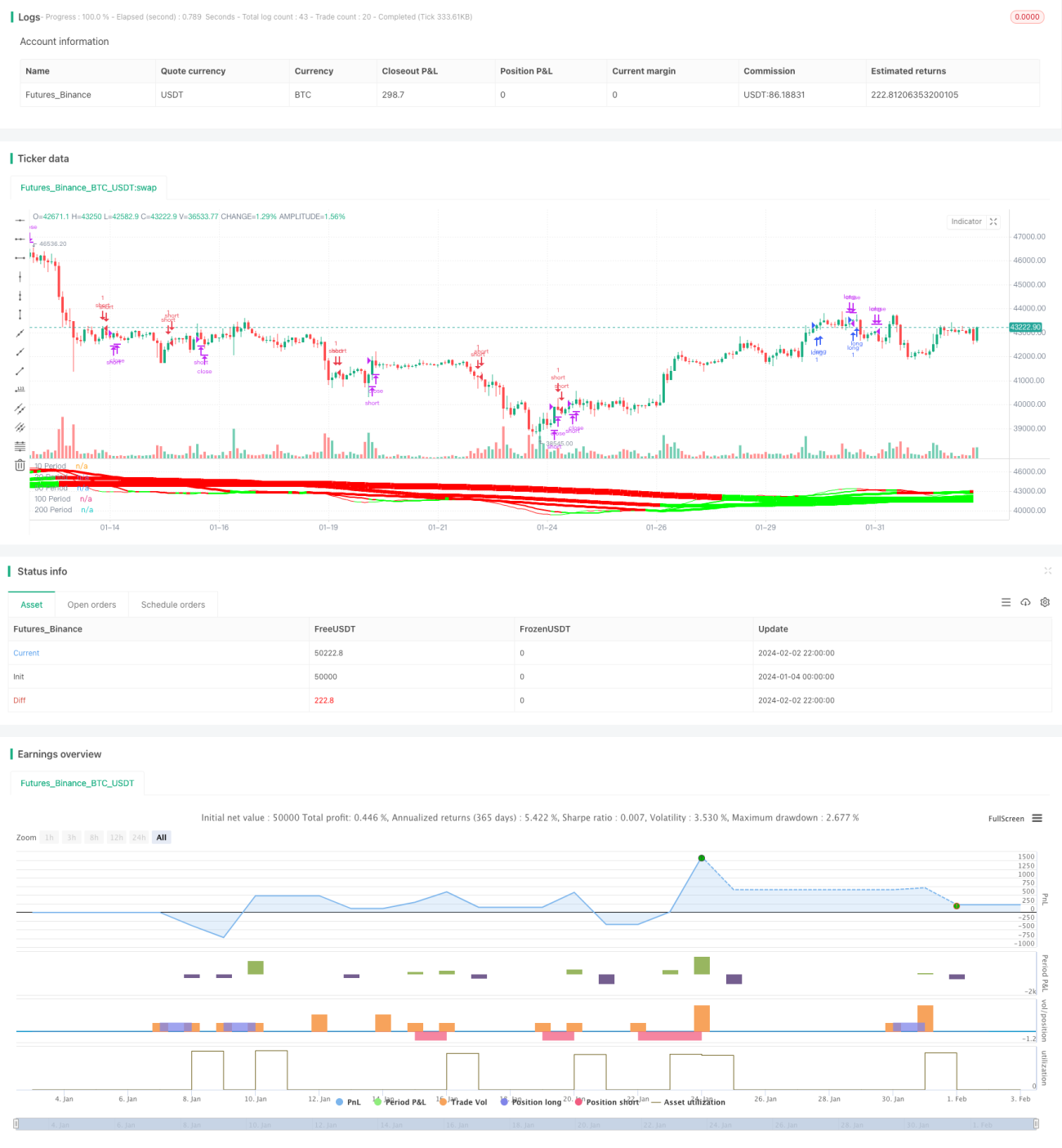

본 전략은 다양한 주기의 SMA 이동평균선을 조합하여 추세를 판단하고 추적합니다. 핵심 아이디어는 서로 다른 주기 SMA의 상승 및 하락 방향을 비교하여 추세를 판단하고, 단기 SMA가 장기 SMA를 상향 돌파하면 매수, 단기 SMA가 장기 SMA를 하향 돌파하면 매도하는 것입니다. 동시에 ZeroLagEMA 지표를 사용하여 진입 및 청산을 확인합니다.

전략 원리

- 5개의 다른 주기 SMA 이동평균선을 사용합니다: 10주기, 20주기, 50주기, 100주기, 200주기.

- 이 5개 이동평균선의 상승 및 하락 방향을 비교하여 추세 방향을 판단합니다. 예를 들어, 10주기, 20주기, 100주기, 200주기 SMA가 모두 상승하면 상승 추세로 판단하고, 모두 하락하면 하락 추세로 판단합니다.

- 서로 다른 주기 SMA 값을 비교하여 거래 신호를 생성합니다. 예를 들어, 10주기 SMA가 20주기 SMA를 상향 돌파하면 매수(진입 신호), 10주기 SMA가 20주기 SMA를 하향 돌파하면 매도(진입 신호)합니다.

- ZeroLagEMA를 진입 확인 및 청산 신호로 사용합니다. 빠른 주기 ZeroLagEMA가 느린 주기를 상향 돌파하면 매수, 하향 돌파하면 매수 포지션을 청산합니다. 매도 신호는 반대로 판단합니다.

전략 장점

- 다양한 주기의 SMA 이동평균선 조합을 사용하여 시장 추세 방향을 효과적으로 판단할 수 있습니다.

- 주기 SMA 값 비교를 통해 거래 신호를 생성하여 정량화된 진입 및 청산 규칙을 제공합니다.

- ZeroLagEMA 필터를 사용하여 불필요한 거래를 피하고 전략 안정성을 높입니다.

- 추세 판단과 거래 신호를 결합하여 추세 추종 거래를 구현합니다.

전략 위험 및 해결 방안

- 시장이 횡보 국면에 진입하면 SMA 이동평균선 신호가 빈번하게 교차하여 무효 거래 및 손실 위험이 증가할 수 있습니다.

- 해결 방법: ZeroLagEMA 필터 파라미터를 증가시켜 무효 신호 진입을 방지합니다.

- 많은 주기의 SMA를 참조하기 때문에 신호 판단에 일부 지연이 발생하여 단기 급격한 가격 변동에 신속하게 대응하지 못할 수 있습니다.

- 해결 방법: MACD 등 더 민감한 지표를 결합하여 보조 판단합니다.

전략 최적화 방향

- SMA 주기 파라미터를 최적화하여 최적의 파라미터 조합을 찾습니다.

- 손절 전략(예: 트레일링 스톱)을 추가하여 단일 손실을 추가로 제어합니다.

- 포지션 크기 관리 메커니즘을 추가하여 추세가 강할 때 포지션을 확대하고, 변동성이 적을 때 포지션을 축소합니다.

- MACD, KDJ 등 더 많은 보조 지표를 결합하여 전반적인 전략 안정성을 높입니다.

요약

본 전략은 여러 주기의 SMA 이동평균선을 조합하여 시장 추세 방향을 효과적으로 판단하고 정량적 거래 신호를 생성합니다. 또한 ZeroLagEMA 적용을 통해 전략 성공률을 높였습니다. 전반적으로 추세 추종 기반의 정량 거래 접근법을 구현하여 효과가 뚜렷합니다. SMA 주기 파라미터, 손절 전략, 포지션 관리 등을 추가로 최적화하면 전략 효과를 더욱 강화할 수 있으며, 실전 검증 및 적용 가치가 있습니다.

Source

Pine

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Forex MA Racer - SMA Performance /w ZeroLag EMA Trigger", shorttitle = "FX MA Racer (5x SMA, 2x zlEMA)", overlay=false )

// === INPUTS ===Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1