이중 반전 모멘텀 지수 전략

1

Follow

1802

Followers

개요

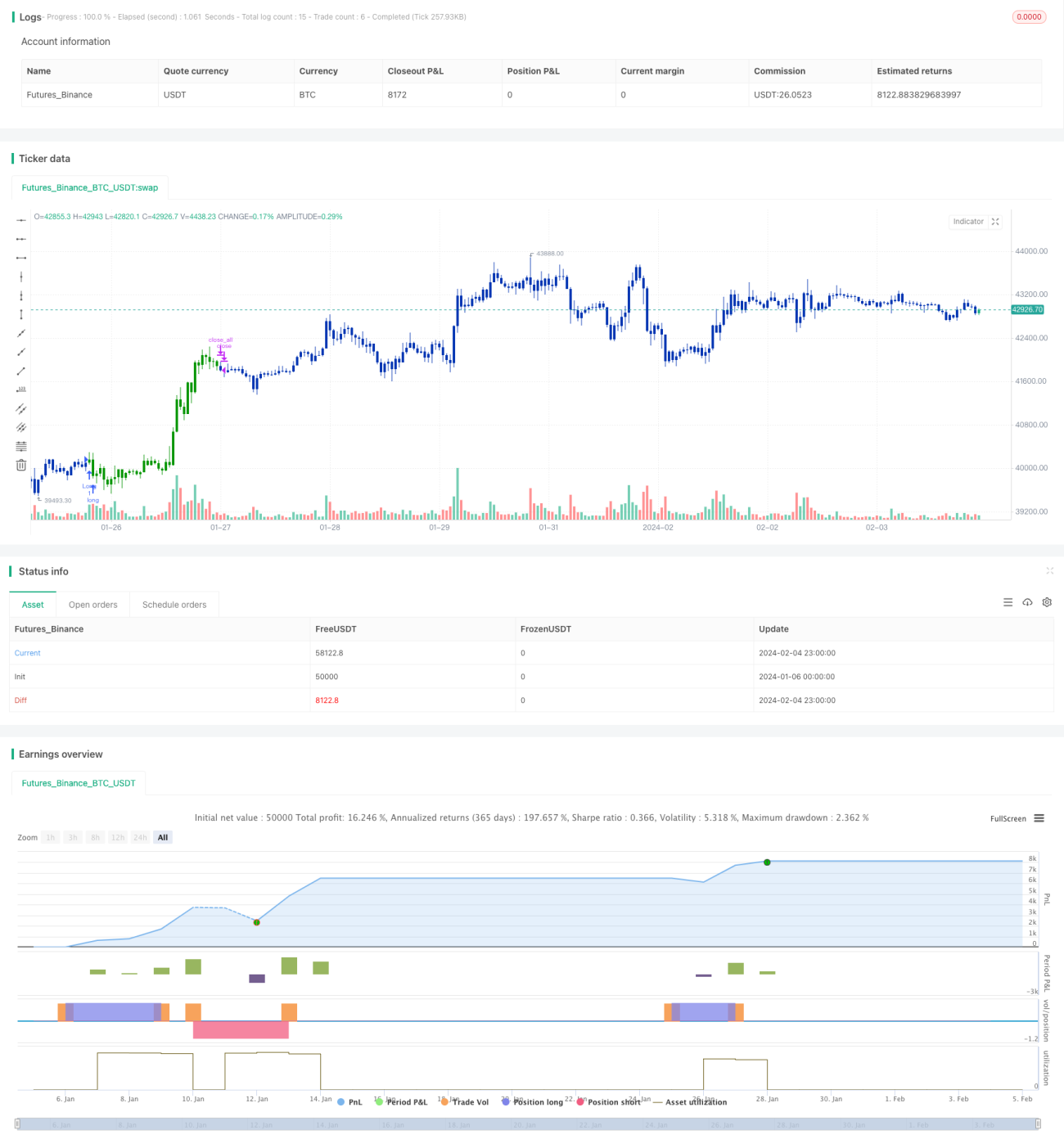

이중 반전 모멘텀 지수 전략은 123 반전 전략과 상대 모멘텀 지수(RMI) 전략을 결합한 조합 전략입니다. 이중 신호를 활용하여 거래 결정의 정확성을 높이는 것을 목표로 합니다.

전략 원리

해당 전략은 두 부분으로 구성됩니다:

-

123 반전 전략

- 전일 종가가 그전날보다 낮고, 오늘 종가가 그전날보다 높으며, 9일 Slow K선이 50 미만일 때 매수

- 전일 종가가 그전날보다 높고, 오늘 종가가 그전날보다 낮으며, 9일 Fast K선이 50 초과일 때 매도

-

상대 모멘텀 지수(RMI) 전략

- RMI는 RSI에 모멘텀 요소를 추가한 변형 지표입니다. 계산식: RMI = (상승 모멘텀 SMA) / (하락 모멘텀 SMA) * 100

- RMI가 과매수선 미만일 때 매수, RMI가 과매도선 초과일 때 매도

이 조합 전략은 123 반전과 RMI 이중 신호가 동일한 방향으로 발생할 때만 거래 신호를 생성합니다. 이를 통해 잘못된 거래 기회를 효과적으로 줄일 수 있습니다.

전략 장점 분석

해당 전략은 다음과 같은 장점을 가집니다:

- 이중 지표 결합으로 신호 정확도 향상

- 반전 전략 활용으로 횡보장에 적합

- RMI 지표가 민감하여 강한 추세의 전환점 식별 가능

전략 리스크 분석

해당 전략에는 다음과 같은 리스크도 존재합니다:

- 이중 필터링으로 일부 거래 기회를 놓칠 수 있음

- 반전 신호가 오판될 가능성

- RMI 매개변수 설정이 부적절하면 효과 저하

매개변수 조합 조정, 지표 계산 방식 최적화를 통해 이러한 리스크를 낮출 수 있습니다.

전략 최적화 방향

해당 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

- 다양한 매개변수 조합 테스트로 최적 매개변수 탐색

- KDJ, MACD 등 다른 반전 지표 조합 시도

- RMI 공식 조정으로 더 민감하게 개선

- 손절매 메커니즘 추가로 단일 손실 통제

- 거래량 결합으로 허위 신호 방지

요약

이중 반전 모멘텀 지수 전략은 이중 신호 필터링과 매개변수 최적화를 통해 거래 결정의 정확성을 효과적으로 높이고, 잘못된 신호 발생 확률을 낮춥니다. 횡보장에 적합하며 반전 기회를 포착할 수 있습니다. 이 전략은 매개변수 조정과 지표 계산 방식 최적화를 통해 효과를 더욱 강화하고 리스크를 줄일 수 있습니다.

Source

Pine

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal. Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1