Strategi Serapan Semasa Penurunan Berbentuk Pelarasan

Gambaran Keseluruhan

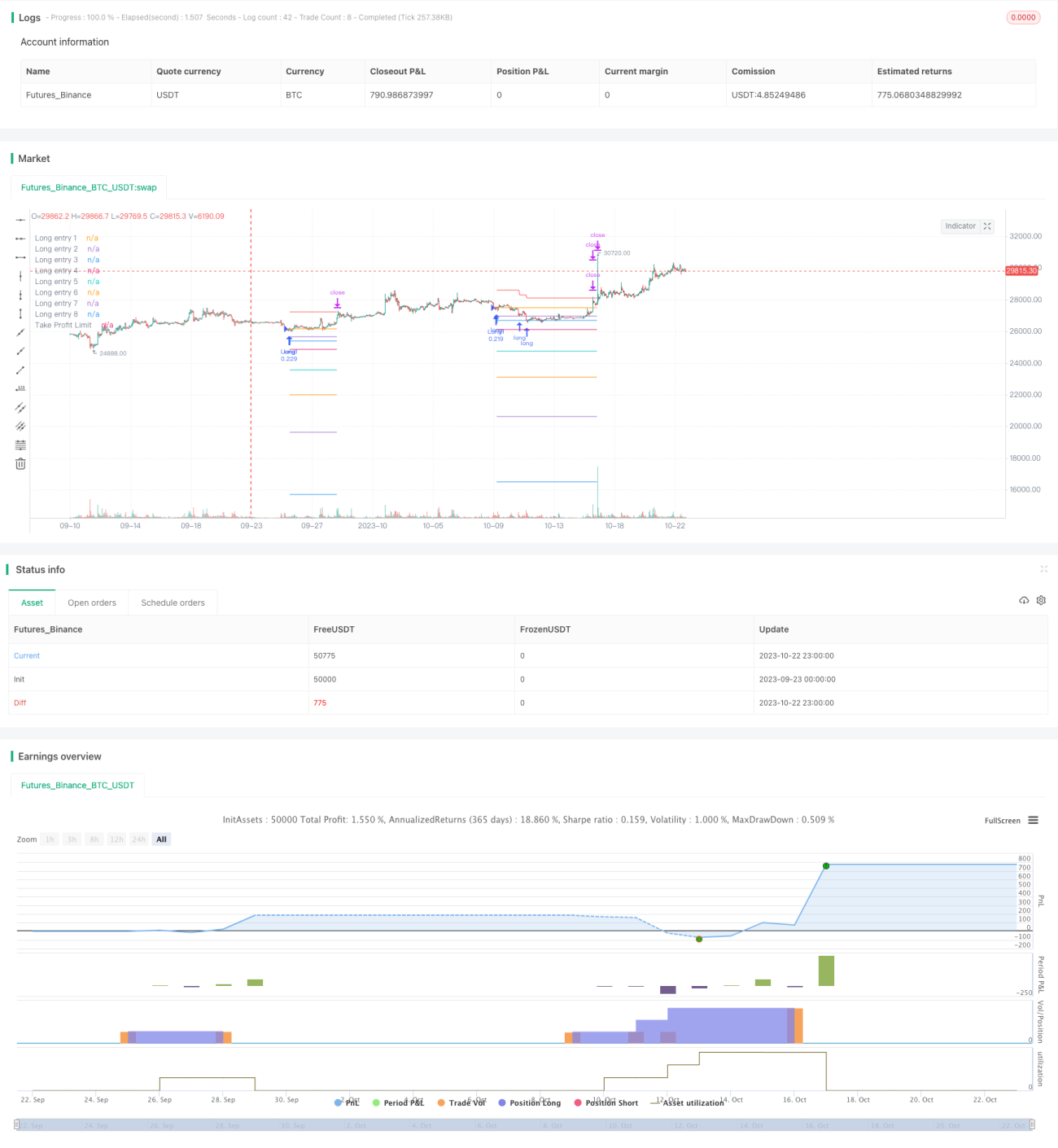

Strategi ini menggabungkan indikator RSI dan purata pergerakan harga untuk mencari peluang terlebih jual apabila harga saham jatuh di bawah purata pergerakan dan membuka kedudukan beli. Apabila harga saham terus menurun, strategi akan menambah kedudukan secara berlapis mengikut peratusan yang telah ditetapkan bagi mencapai purata kos pegangan. Apabila keuntungan kedudukan mencapai peratusan ambil untung yang dikonfigurasikan, strategi akan memilih untuk menutup kedudukan. Pada masa yang sama, strategi memperkenalkan mekanisme ambil untung progresif, yang secara dinamik melaraskan harga ambil untung keseluruhan posisi berdasarkan keuntungan kedudukan individu yang telah direalisasikan. Ini dapat mengurangkan risiko kerugian dengan berkesan dan mencapai pengeluaran secara berperingkat.

Prinsip Strategi

-

Apabila indikator RSI berada di bawah garis terlebih jual 29 dan harga penutupan berada di bawah purata pergerakan, buka pesanan pertama untuk kedudukan beli.

-

Apabila harga saham jatuh sebanyak 2% berbanding pesanan pertama, tambah kedudukan beli; apabila penurunan mencapai 3%, tambah kedudukan untuk kali ketiga, dan seterusnya sehingga maksimum 8 kali penambahan. Ini mencapai kesan pembukaan kedudukan secara berperingkat.

-

Selepas setiap pembukaan kedudukan, harga pembukaan pada masa itu akan direkodkan. Titik harga ini adalah harga rujukan untuk masuk ke pasaran. Garis harga ini akan dilukis pada carta.

-

Selepas pembukaan kedudukan, purata harga pegangan akan dikira. 3% daripada harga purata akan digunakan sebagai harga ambil untung bagi setiap kedudukan, manakala 4% sebagai harga ambil untung bagi keseluruhan posisi.

-

Apabila harga meningkat melebihi harga ambil untung sesuatu kedudukan, kedudukan tersebut akan dipilih untuk ditutup.

-

Cara pengiraan ambil untung progresif: setiap kali satu kedudukan ditutup, keuntungan yang direalisasikan oleh kedudukan tersebut akan ditolak daripada harga ambil untung keseluruhan. Ini menyebabkan garis ambil untung perlahan-lahan menurun, dan hanya apabila keuntungan semua kedudukan mencukupi untuk menampung kerugian maksimum, barulah semua kedudukan akan diambil untung.

-

Apabila harga menyentuh garis ambil untung progresif, pilih untuk menutup semua kedudukan.

Analisis Kelebihan

-

Indikator RSI dapat menilai zon terlebih jual dengan tepat, membantu menangkap peluang pembalikan.

-

Penambahan kedudukan secara berperingkat beberapa kali membolehkan purata kos pegangan pada paras rendah.

-

Ambil untung progresif dapat mengurangkan risiko kerugian dan mencapai pengeluaran secara berperingkat. Walaupun berlaku kerugian, ia boleh dikawal dalam lingkungan tertentu.

-

Nisbah ambil untung dan nisbah penambahan yang boleh dikonfigurasikan membolehkan pelarasan risiko strategi mengikut pasaran.

-

Garis rujukan buka kedudukan dan garis ambil untung digambarkan pada carta, membolehkan penilaian visual taburan kedudukan.

Analisis Risiko

-

Dalam pasaran yang berayun, banyak kali pembukaan dan ambil untung mungkin dicetuskan, menyebabkan perdagangan kerap dan kerugian gelinciran. Parameter RSI boleh dilonggarkan untuk mengurangkan kekerapan perdagangan.

-

Penetapan bilangan dan nisbah penambahan yang tidak sesuai boleh menyebabkan perdagangan berlebihan. Ia perlu dikonfigurasikan secara berhati-hati berdasarkan keadaan modal.

-

Jika pasaran terus menurun semasa penambahan, risiko lubang tanpa dasar mungkin dihadapi. Had atas bilangan penambahan harus ditetapkan, dan nisbah penambahan untuk lapisan terakhir harus konservatif.

-

Jika nisbah ambil untung ditetapkan terlalu kecil, ambil untung mungkin berlaku terlalu awal. Nisbah ambil untung yang sesuai harus ditetapkan berdasarkan data ujian sejarah.

Arah Pengoptimuman

-

Indikator seperti MACD boleh diperkenalkan untuk menapis isyarat RSI, mengurangkan perdagangan tidak berkesan.

-

Henti rugi boleh ditetapkan berdasarkan ATR untuk mengelakkan kerugian besar dalam pasaran ekstrem.

-

Parameter seperti bilangan penambahan, nisbah penambahan, dan nisbah ambil untung boleh dioptimumkan untuk menjadikan strategi lebih sesuai dengan pelbagai instrumen.

-

Nisbah ambil untung boleh diselaraskan secara pintar berdasarkan turun naik, dilonggarkan apabila turun naik tinggi.

Kesimpulan

Strategi ini memanfaatkan sepenuhnya indikator RSI untuk menilai zon terlebih jual, digabungkan dengan purata pergerakan harga untuk perdagangan pembalikan. Pada masa yang sama, mekanisme penambahan pintar dan ambil untung progresif digunakan untuk mencapai strategi beli yang cekap di bawah kawalan risiko. Dengan mengoptimumkan parameter indikator, mekanisme ambil untung, dan lain-lain, strategi boleh menjadi lebih stabil dan cekap. Strategi ini boleh digunakan secara meluas dalam instrumen kewangan seperti niaga hadapan indeks saham, mata wang kripto yang mempunyai ciri pembalikan arah aliran, dan mempunyai nilai pelaburan praktikal.

- 1