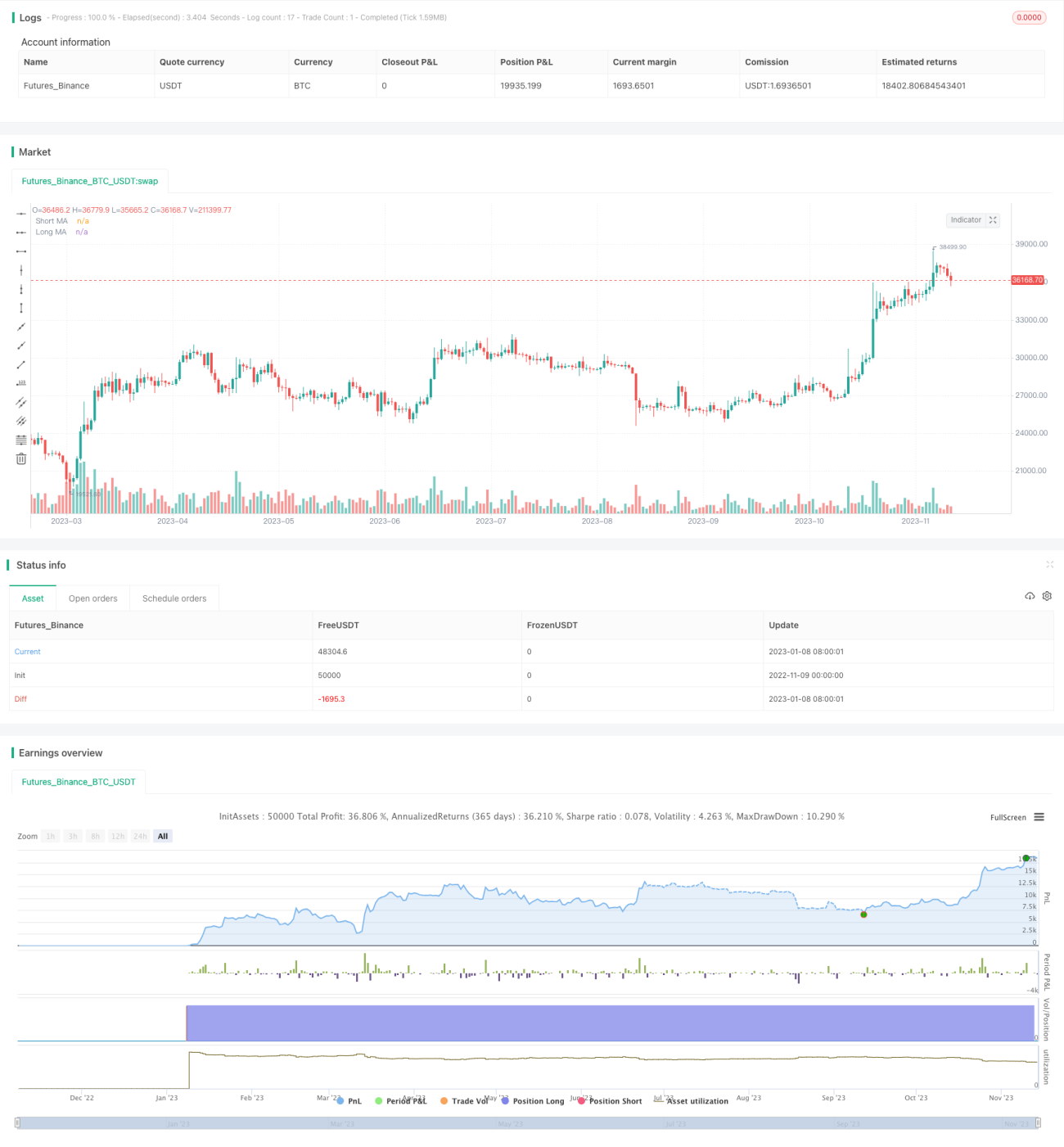

Strategi Perdagangan Kuantitatif DCA Berwajaran Elemen Progresif

Gambaran Keseluruhan

Strategi perdagangan kuantitatif DCA Berwajaran Progresif dengan Elemen ialah strategi yang menggabungkan isyarat pencetus daripada penunjuk purata bergerak dengan mekanisme purata kos dolar (dollar cost averaging) secara berwajaran progresif. Strategi ini bertujuan untuk mendapatkan pulangan yang lebih stabil dalam pasaran yang mempunyai arah trend yang kukuh melalui penilaian arah aliran dan pengagihan kos.

Prinsip

Strategi ini terdiri daripada tiga bahagian utama:

-

Isyarat Kemasukan

Menggunakan persilangan antara purata bergerak pantas dan purata bergerak perlahan sebagai isyarat untuk memasuki pasaran. Pengguna boleh memilih SMA, EMA atau HMA sebagai purata pantas dan perlahan. Apabila purata pantas menembusi purata perlahan dari bawah, ia menghasilkan isyarat beli; apabila purata pantas jatuh melepasi purata perlahan dari atas, ia menghasilkan isyarat jual.

-

DCA Berwajaran Progresif

Selepas isyarat beli dicetuskan, strategi akan segera membuka kedudukan asas. Sekiranya harga terus menurun, strategi akan menambah kedudukan selamat seterusnya secara berwajaran progresif. Harga setiap kedudukan selamat baharu akan merujuk kepada harga kedudukan selamat sebelumnya dan dikurangkan sebanyak julat tertentu. Pada masa yang sama, jumlah dana untuk kedudukan selamat baharu juga akan ditingkatkan secara progresif.

Dengan cara menambah kedudukan secara progresif, kos dapat diagihkan sedikit sebanyak, menghasilkan kos yang lebih optimum sambil memastikan risiko perdagangan terkawal.

-

Ambil Untung dan Henti Rugi

Apabila harga meningkat melepasi garis ambil untung, strategi akan mengambil untung; apabila harga jatuh melepasi garis henti rugi, strategi akan menghentikan kerugian.

Garis ambil untung ditetapkan pada harga purata kedudukan asas didarab dengan (1 + nisbah tetap).

Garis henti rugi berubah-ubah mengikut harga kedudukan selamat terakhir. Isyarat henti rugi disahkan berdasarkan peratusan di bawah harga urus niaga kedudukan selamat terakhir.

Kelebihan

-

Gabungan penilaian arah aliran dan pengagihan kos menjadikan strategi lebih stabil

Penilaian arah aliran dapat mengelakkan pasaran yang tidak berarah (sideways), manakala pengagihan kos membolehkan kos yang lebih optimum dalam aliran.

-

Penambahan kedudukan secara progresif mengawal risiko

Setiap saiz kedudukan yang seimbang mempunyai julat tertentu, dan kedudukan seterusnya memerlukan penurunan harga tertentu, sekali gus mengawal risiko.

-

Pemantauan masa nyata penggunaan modal strategi

Kod dilengkapi label pemantauan masa nyata supaya pengguna mengetahui had penggunaan modal strategi dan mengelakkan penggunaan berlebihan yang boleh menyebabkan likuidasi paksa.

-

Ambil untung dan henti rugi yang fleksibel untuk setiap kedudukan

Kedudukan asas dan kedudukan selamat boleh diambil untung atau henti rugi secara berasingan, merealisasikan keuntungan dan mengawal risiko.

Risiko dan Pengoptimuman

-

Turun naik harga yang mendadak boleh menyebabkan penambahan kedudukan berganda

Apabila harga turun naik secara mendadak, ia boleh mencetuskan penambahan kedudukan berganda yang meningkatkan kerugian. Ini boleh dikurangkan dengan menetapkan keperluan penurunan harga yang lebih besar antara kedudukan selamat seterusnya.

-

Pemilihan parameter purata bergerak perlu dioptimumkan

Parameter purata bergerak secara langsung mempengaruhi masa kemasukan; parameter yang sesuai perlu diuji untuk instrumen yang berbeza.

-

Nisbah ambil untung dan henti rugi perlu diuji dan dioptimumkan

Nisbah ini mempengaruhi kadar pulangan dan kawalan pengeluaran; perlu dioptimumkan melalui data ujian semula.

-

Syarat likuidasi paksa berdasarkan pengeluaran atau masa boleh ditambah

Syarat likuidasi paksa seperti pengeluaran maksimum atau tempoh pegangan melebihi ambang boleh diuji untuk mengawal risiko selanjutnya.

Kesimpulan

Strategi perdagangan kuantitatif DCA Berwajaran Progresif dengan Elemen menggabungkan kelebihan penilaian arah aliran dan pengagihan kos, membolehkan pulangan yang stabil dalam pasaran yang mempunyai arah trend yang kuat. Dengan mengoptimumkan tetapan parameter, melaraskan saiz kedudukan dan keperluan penurunan antara kedudukan, perdagangan yang stabil dengan risiko terkawal dapat dicapai. Strategi ini boleh digunakan dalam reka bentuk dana lindung nilai, dana CTA dan strategi berlawanan.

- 1