Strategi Intraday Pengesanan Trend yang Menggabungkan Pelbagai Stop Loss

Gambaran Keseluruhan

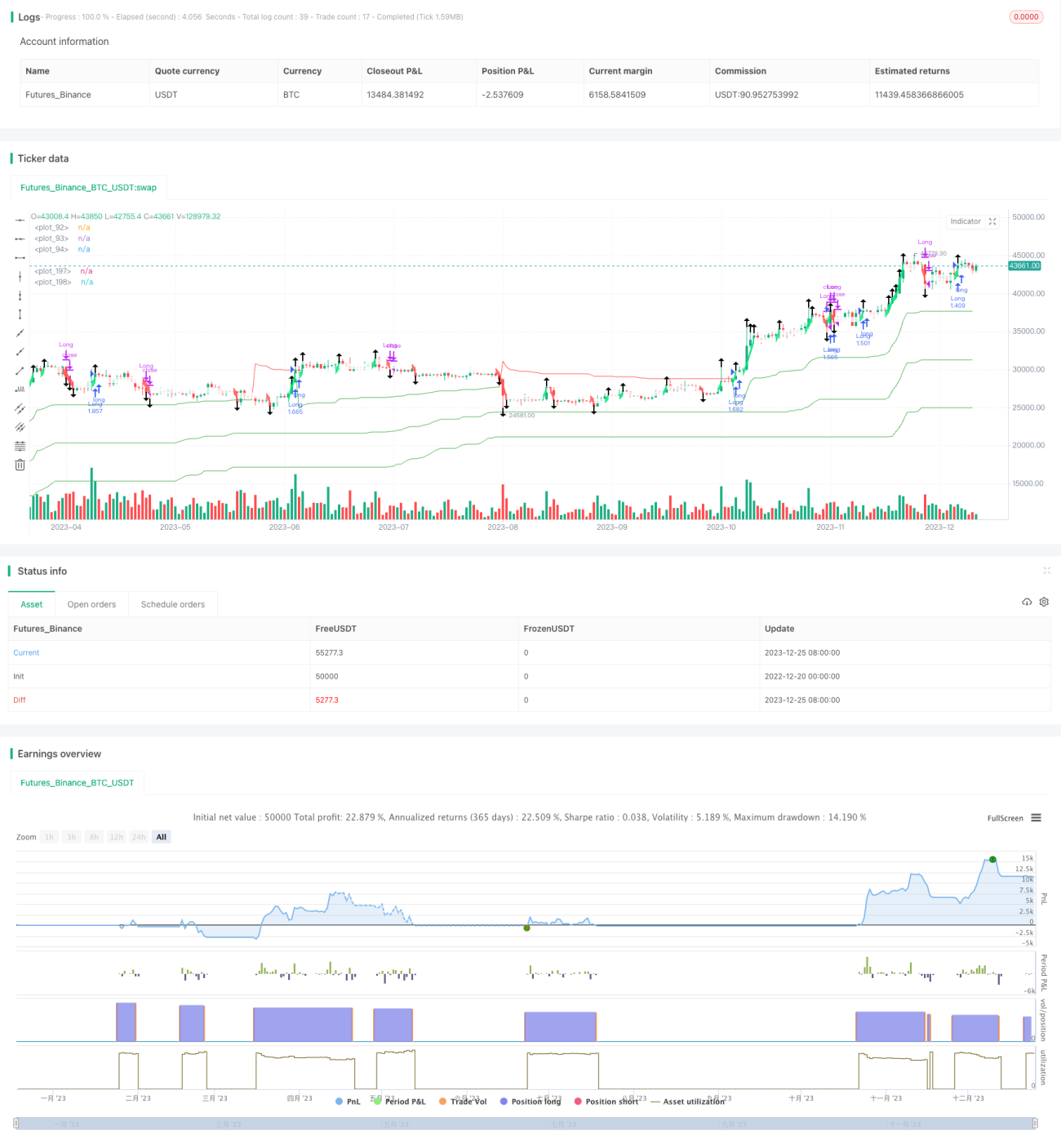

Strategi ini menggabungkan beberapa henti rugi dinamik ATR dan blok Renko yang diperbaiki, bertujuan untuk menangkap arah aliran Intraday. Ia menggabungkan penunjuk arah aliran dan penunjuk blok, melaksanakan analisis pelbagai jangka masa, yang dapat mengenal pasti arah aliran dengan berkesan dan menghentikan kerugian tepat pada masanya.

Prinsip Strategi

Inti strategi ini terletak pada mekanisme henti rugi berbilang ATR. Ia menetapkan 3 kumpulan henti rugi dinamik ATR, dengan parameter masing-masing 5 kali ATR, 10 kali ATR, dan 15 kali ATR. Apabila harga menembusi ketiga-tiga garis henti rugi ini, ia menunjukkan perubahan arah aliran, dan posisi akan ditutup. Penetapan berbilang henti rugi ini dapat menapis isyarat palsu yang disebabkan oleh turun naik jangka pendek dengan berkesan.

Bahagian teras yang lain ialah blok Renko yang diperbaiki. Blok ini membahagikan kenaikan berdasarkan nilai ATR, dan menggabungkan penunjuk SMA untuk menentukan arah aliran. Ia lebih sensitif daripada blok Renko biasa, dan dapat mengesahkan perubahan arah aliran lebih awal. Apabila warna blok berubah, ia menunjukkan perubahan arah aliran dan boleh digunakan sebagai isyarat henti rugi.

Syarat masuk adalah apabila harga menembusi ke atas ketiga-tiga henti rugi ATR, maka buka posisi panjang; apabila harga menembusi ke bawah ketiga-tiga henti rugi ATR, maka buka posisi pendek. Syarat keluar adalah apabila harga mencetuskan mana-mana satu henti rugi ATR atau warna blok Renko berubah, maka tutup posisi.

Kelebihan Strategi

- Henti rugi berbilang ATR mengawal risiko dengan berkesan

- Blok Renko yang diperbaiki lebih sensitif, membolehkan henti rugi awal

- Menggabungkan penunjuk arah aliran dan penunjuk blok untuk memastikan penangkapan arah aliran

- Analisis pelbagai jangka masa menjadikan penentuan arah aliran lebih boleh dipercayai

- Parameter boleh laras, sesuai dengan pelbagai persekitaran pasaran

Risiko Strategi dan Pengoptimuman

Risiko utama strategi ini adalah henti rugi ditembusi menyebabkan kerugian yang lebih besar. Ia boleh dioptimumkan melalui kaedah berikut:

- Laraskan gandaan henti rugi ATR; dalam pasaran dengan arah aliran yang kuat, boleh dilonggarkan sedikit; apabila arah aliran lemah, perlu diketatkan

- Laraskan parameter tempoh ATR bagi blok Renko untuk mengimbangi sensitiviti dan kestabilan

- Tambah penunjuk henti rugi lain, seperti saluran Donchian, untuk memastikan henti rugi lebih boleh dipercayai

- Tambah penapis untuk mengelakkan perdagangan kerap dalam pasaran yang mendatar

Kesimpulan

Secara keseluruhan, strategi ini sesuai untuk arah aliran kuat Intraday. Ciri-cirinya adalah penetapan henti rugi yang saintifik, dan penunjuk blok dapat mengenal pasti perubahan arah aliran lebih awal. Melalui pelarasan parameter, ia dapat menyesuaikan diri dengan pelbagai persekitaran pasaran, menjadikannya strategi penjejakan arah aliran yang layak untuk pengesahan secara langsung.

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Lancelot vstop intraday strategy", overlay=true, currency=currency.NONE, initial_capital = 100, commission_type=strategy.commission.percent,

commission_value=0.075, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

- 1