Strategi Perdagangan Penjejakan Grid K-Line Dua Hala

1

Follow

1802

Followers

Gambaran Keseluruhan

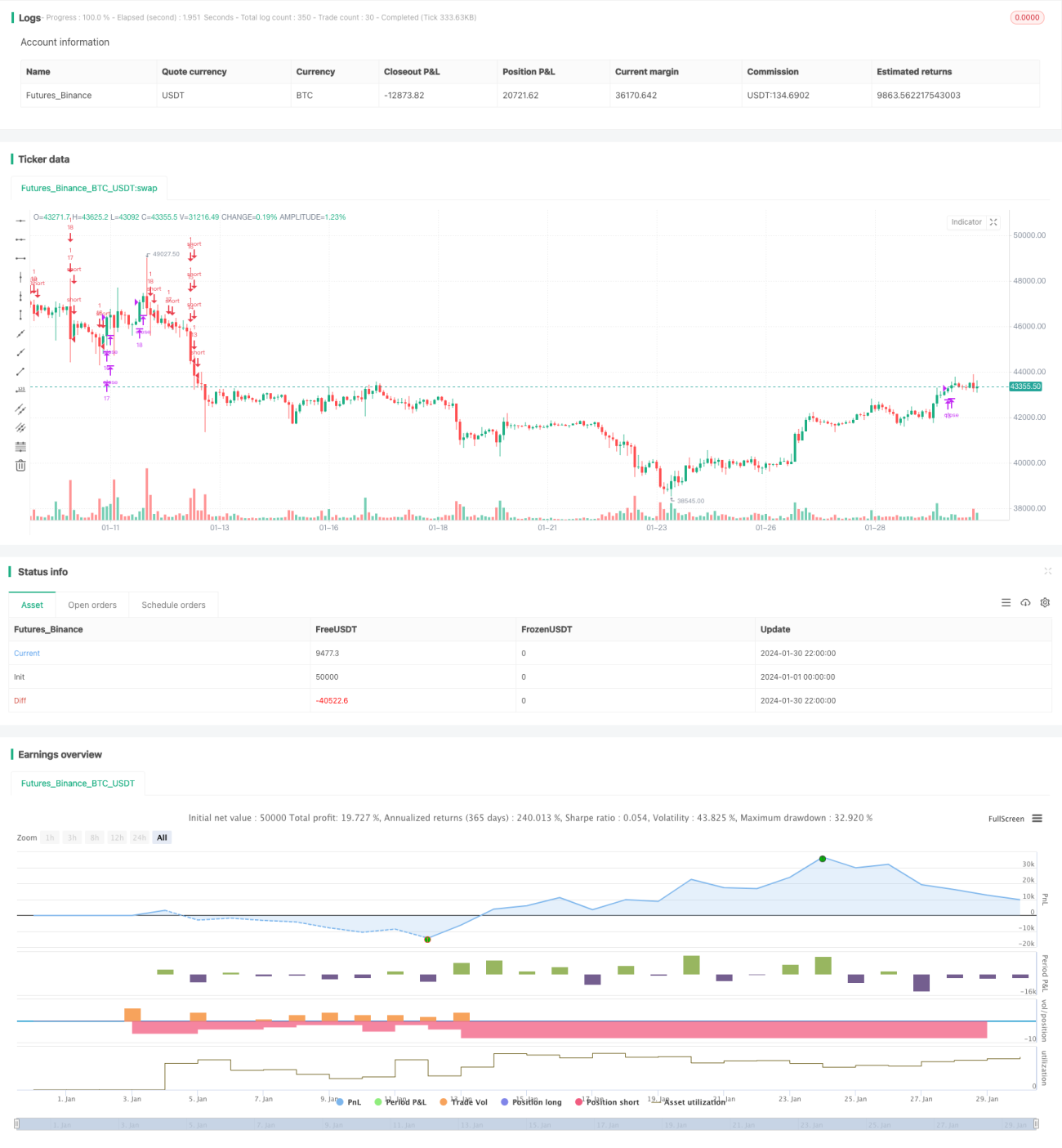

Strategi ini adalah strategi perdagangan grid dua hala berdasarkan perubahan masa nyata lilin candlestick. Ia boleh memperoleh keuntungan yang stabil dalam kedua-dua pasaran menaik (bull market) dan menurun (bear market).

Prinsip Strategi

- Berdasarkan bilangan grid yang ditetapkan oleh pengguna, ia secara automatik mengira julat harga grid dan harga setiap grid.

- Apabila harga menembusi harga grid, pesanan beli (long) dibuka dengan kuantiti tetap; apabila harga jatuh di bawah harga grid, posisi beli ditutup dan pesanan jual (short) dibuka.

- Dengan cara ini, apabila harga berayun dalam julat grid, keuntungan dapat diperoleh dengan menjejaki perubahan harga.

Analisis Kelebihan

- Mengira julat grid yang munasabah secara automatik, tidak perlu menentukan sokongan dan rintangan secara manual.

- Perdagangan dua hala, boleh menyesuaikan diri dengan persekitaran pasaran yang berubah-ubah.

- Kuantiti buka posisi tetap, membantu dalam kawalan risiko.

- Kod yang jelas dan ringkas, mudah difahami dan diubah suai.

Analisis Risiko

- Turun naik pasaran yang mendadak boleh menyebabkan kerugian meningkat.

- Pengumpulan kos transaksi juga akan mempengaruhi keuntungan akhir.

- Perlu menentukan bilangan grid dengan munasabah; terlalu banyak grid akan meningkatkan kekerapan transaksi tetapi keuntungan setiap kali adalah terhad.

Hala Tuju Pengoptimuman

- Menambah strategi stop loss untuk mengelakkan kerugian yang lebih besar.

- Menambah fungsi pelarasan dinamik bilangan grid.

- Mempertimbangkan untuk menambah leveraj bagi meningkatkan volum dagangan.

Kesimpulan

Strategi ini mempunyai idea yang jelas dan ringkas secara keseluruhan, memperoleh pendapatan yang stabil melalui perdagangan grid dua hala, namun juga mempunyai risiko perdagangan tertentu. Dengan pengoptimuman berterusan, ia dijangka dapat mencapai hasil yang lebih baik.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1