Strategi Penjejakan Ayunan Jalur Terapung

Gambaran Keseluruhan

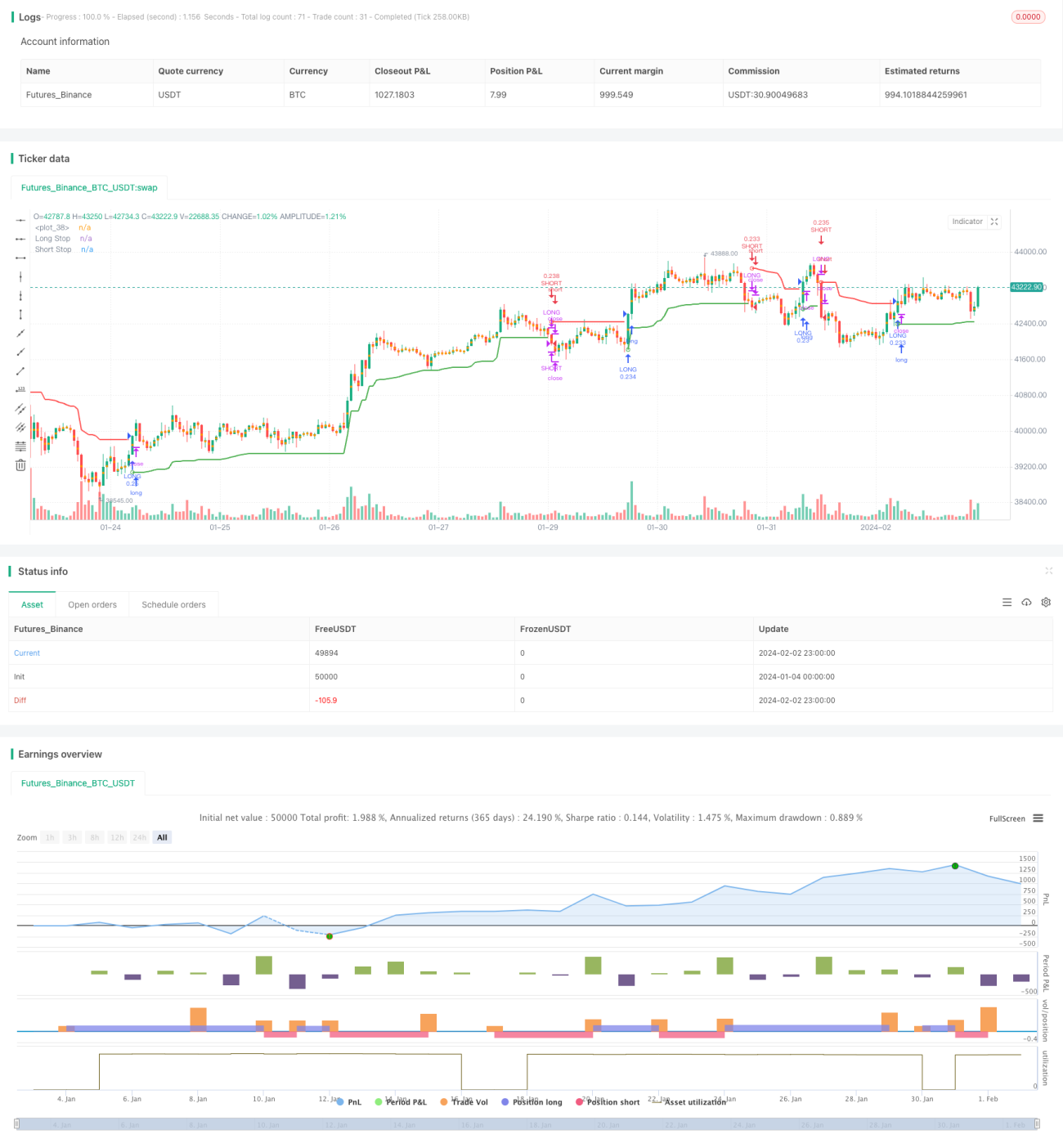

Idea utama strategi ini adalah untuk mengira tahap henti rugi jangka panjang dan jangka pendek berdasarkan penunjuk ATR, dan menjana isyarat dagangan apabila harga menembusi garisan henti rugi ini. Ia mempunyai fungsi menjejak arah aliran dan menangkap turun naik pasaran.

Prinsip Strategi

Strategi ini menggunakan ATR tempoh N didarab dengan pekali untuk mengira garisan henti rugi di kedua-dua belah. Formula pengiraan khusus adalah seperti berikut:

Henti rugi jangka panjang = Harga tertinggi - ATR * pekali

Henti rugi jangka pendek = Harga terendah + ATR * pekali

Apabila harga meningkat dan menembusi garisan henti rugi jangka panjang, ia akan mengambil posisi beli (long); apabila harga menurun dan menembusi garisan henti rugi jangka pendek, ia akan mengambil posisi jual (short). Selepas mengambil posisi beli atau jual, pergerakan harga akan dijejaki secara masa nyata untuk mengalihkan garisan henti rugi.

Kaedah menetapkan garisan henti rugi menggunakan jalur ATR ini dapat menangkap sepenuhnya arah aliran harga sambil memastikan risiko henti rugi dikawal. Apabila harga mengalami penembusan yang ketara, isyarat akan dijana, yang berkesan menapis penembusan palsu.

Analisis Kelebihan

Kelebihan terbesar strategi ini ialah ia dapat melaraskan tahap henti rugi secara automatik, menangkap arah aliran harga sambil mengawal risiko. Kelebihan khusus adalah seperti berikut:

-

Berdasarkan penunjuk ATR untuk menetapkan henti rugi terapung, ia dapat melaraskan tahap henti rugi mengikut turun naik pasaran, mengawal kerugian setiap dagangan dengan berkesan.

-

Menggunakan kaedah penembusan untuk menjana isyarat, ia dapat menapis sebahagian bunyi pasaran, mengelakkan membeli di puncak dan menjual di dasar.

-

Melaraskan garisan henti rugi secara masa nyata untuk menjejak turun naik harga, mengelakkan henti rugi terlalu longgar, mengunci lebih banyak keuntungan.

Analisis Risiko

Strategi ini juga mempunyai beberapa risiko, terutamanya tertumpu pada penetapan tahap henti rugi dan kaedah penjanaan isyarat. Titik risiko khusus adalah seperti berikut:

-

Tempoh ATR dan pekali yang tidak sesuai boleh menyebabkan henti rugi terlalu lebar atau terlalu sempit.

-

Kaedah isyarat penembusan mungkin terlepas peluang awal arah aliran.

-

Penjejakan henti rugi pada akhir arah aliran mungkin agak ketinggalan, tidak dapat keluar dengan sempurna.

Langkah balas utama adalah dengan melaraskan parameter untuk menjadikan henti rugi lebih munasabah, atau menggunakan penunjuk lain untuk menilai arah aliran dan isyarat.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan lagi dari beberapa aspek berikut:

-

Menetapkan lapisan henti rugi kedua untuk mengawal risiko dengan lebih lanjut.

-

Menggabungkan penunjuk lain untuk menilai arah aliran, meningkatkan kualiti isyarat.

-

Menambah strategi ambil untung bergerak (trailing stop) untuk meningkatkan keuntungan apabila arah aliran berterusan.

-

Mengoptimumkan parameter tempoh ATR dan pekali supaya henti rugi lebih hampir dengan pergerakan harga sebenar.

Kesimpulan

Secara keseluruhan, strategi ini sangat praktikal. Ia dapat melaraskan tahap henti rugi secara automatik untuk mengawal risiko dengan berkesan, sambil memperoleh keuntungan yang baik melalui penjejakan arah aliran. Kita boleh mengoptimumkan dan menambah baik strategi ini dengan menggabungkan kaedah analisis lain berdasarkan asas sedia ada, menjadikannya lebih stabil dan pintar.

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © melihtuna

//@version=4

strategy("Chandelier Exit - Strategy",shorttitle="CE-STG" , overlay=true, default_qty_type=strategy.cash, default_qty_value=10000, initial_capital=10000, currency=currency.USD, commission_value=0.03, commission_type=strategy.commission.percent)- 1