Strategi perdagangan kuantitatif teknikal berbilang penunjuk

Gambaran Keseluruhan

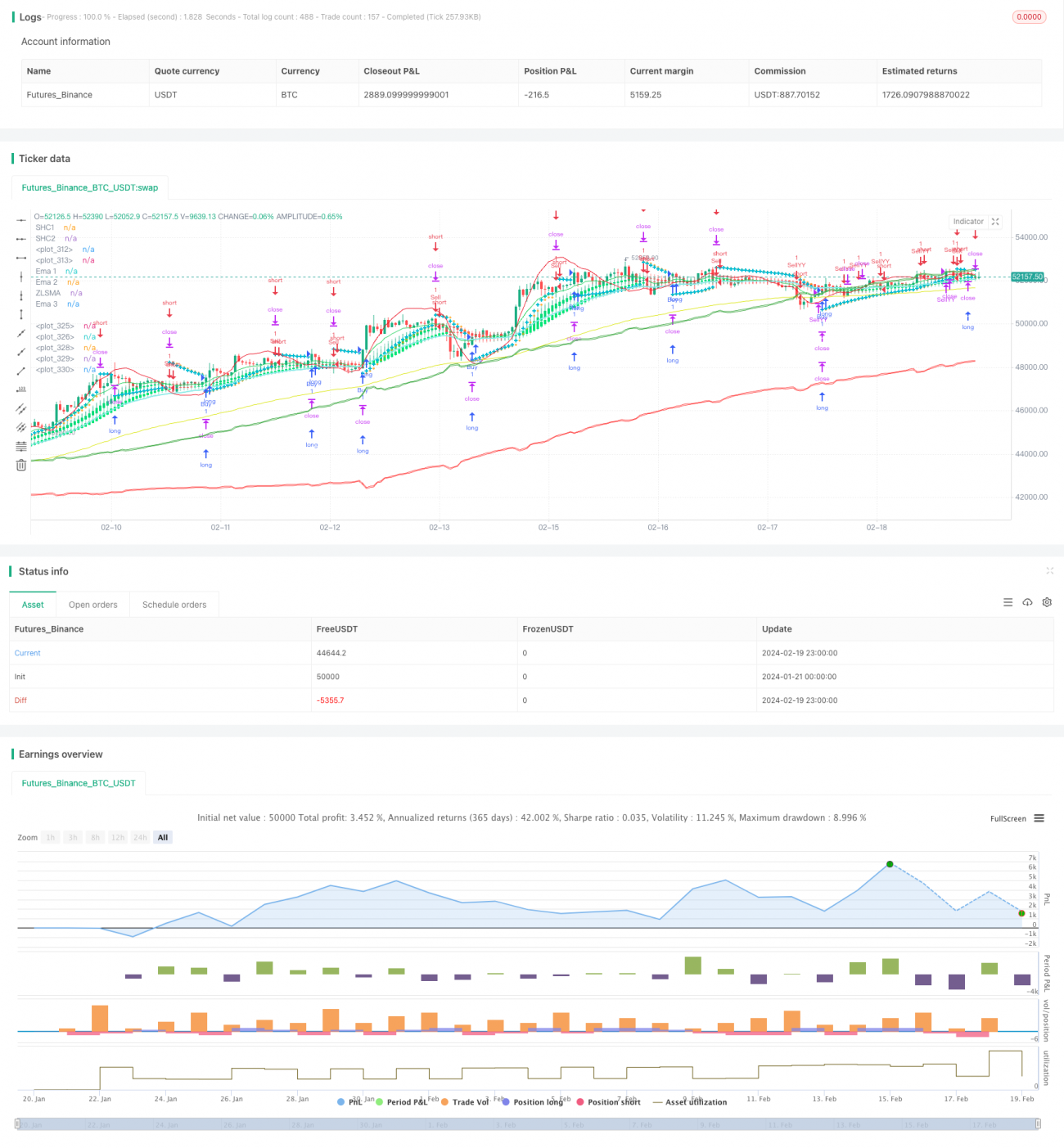

Strategi ini menggabungkan pelbagai penunjuk teknikal, termasuk Parabolic SAR, Strategi Keluar Teori Chan, Purata Bergerak Mudah Tanpa Ketinggalan (Zero Lag Simple Moving Average), Purata Bergerak Eksponen (EMA), Purata Bergerak Aliran (Smoothing Moving Average), dsb., untuk mengenal pasti potensi titik beli dan jual pada carta.

Prinsip Strategi

Penunjuk Utama

- Parabolic SAR: Digunakan untuk menentukan titik henti rugi dan titik masuk yang berpotensi.

- Strategi Keluar Teori Chan: Digunakan untuk menentukan arah aliran.

- Purata Bergerak Mudah Tanpa Ketinggalan (Zero Lag SMA): Menyediakan purata bergerak dengan ketinggalan yang rendah.

- Purata Bergerak Eksponen (EMA): Mengesan arah aliran harga dan turun naik.

- Purata Bergerak Terlicin (Smoothing MA): Menjana purata bergerak yang lebih licin.

Isyarat Dagangan

- Ambil posisi panjang (long) apabila Parabolic SAR menunjukkan aliran menaik dan harga berada di atas EMA ke-99; ambil posisi pendek (short) apabila ia menunjukkan aliran menurun dan harga berada di bawah EMA ke-99.

- Gabungkan isyarat daripada Strategi Keluar Teori Chan untuk mengesahkan arah aliran dengan lebih lanjut.

- Purata Bergerak Terlicin digunakan bersama isyarat Parabolic untuk mengelakkan penembusan palsu.

Pengurusan Risiko

- Tetapkan henti rugi dan ambil untung.

- Pertimbangkan untuk menetapkan semula syarat pembelian, membolehkan pelarasan kedudukan secara fleksibel.

Analisis Kelebihan

Kelebihan utama strategi ini ialah kombinasi penunjuk yang menyeluruh, membolehkan pengesanan arah aliran dengan berkesan. Parabolic SAR menentukan titik pembalikan berpotensi; Strategi Keluar Teori Chan menilai aliran utama; Purata Bergerak menapis isyarat palsu. Pelbagai penunjuk saling mengesahkan, meningkatkan ketepatan isyarat dengan ketara.

Selain itu, strategi ini menggabungkan mekanisme henti rugi dan ambil untung untuk mengawal risiko. Purata Bergerak Terlicin juga digunakan untuk mengelakkan gangguan hingar jangka pendek. Semua ini menjadikan strategi ini sangat stabil.

Analisis Risiko

Oleh kerana bergantung kepada banyak penunjuk untuk membuat keputusan, strategi ini mungkin menghadapi kesukaran apabila penunjuk tersebut memberikan isyarat bercanggah. Selain itu, tetapan parameter yang tidak sesuai juga boleh memberi kesan buruk terhadap dagangan.

Tambahan pula, dagangan berdasarkan analisis teknikal itu sendiri mengandungi risiko tertentu dan tidak dapat mengelakkan kerugian sepenuhnya. Perlukan operasi yang berhati-hati dan elakkan mengikut secara membuta tuli.

Arah Pengoptimuman

- Uji dan optimumkan parameter penunjuk untuk mencari kombinasi terbaik.

- Masukkan algoritma pembelajaran mesin dengan menggunakan data besar untuk melatih model, seterusnya meningkatkan ketepatan isyarat.

- Gabungkan penunjuk sentimen, maklumat berita, dsb. untuk menilai keadaan pasaran, dan laraskan kedudukan serta garis henti rugi secara dinamik.

- Optimumkan logik syarat pembelian semula agar pengesanan isyarat lebih fleksibel dan berterusan.

Kesimpulan

Strategi ini mengintegrasikan pelbagai penunjuk teknikal dan mengenal pasti isyarat dagangan melalui kombinasi penunjuk. Kelebihannya ialah ketepatan isyarat yang tinggi dan kestabilan yang kukuh. Selain itu, langkah kawalan risiko diurus dengan baik. Secara keseluruhan, ia adalah pelan dagangan yang wajar dipertimbangkan. Ia boleh dipertingkatkan lagi melalui pengoptimuman parameter, latihan model, dan pengenalan penunjuk sentimen pada masa hadapan.

- 1