Estratégia de Negociação Quantitativa DCA com Ponderação Progressiva de Elementos

Visão Geral

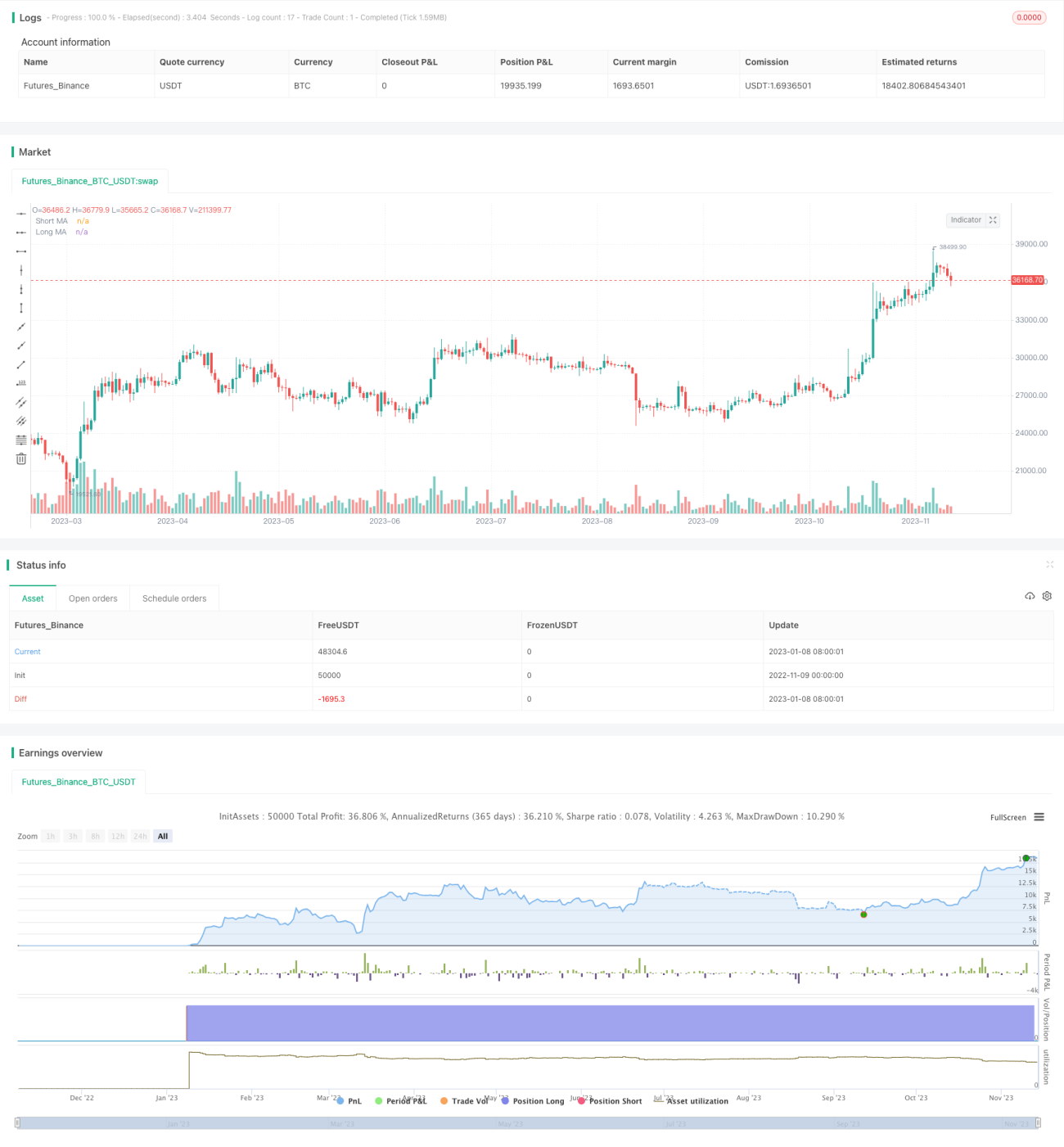

A estratégia de negociação quantitativa DCA com ponderação progressiva de elementos é uma estratégia que combina sinais acionados por indicadores de média móvel com um mecanismo de dollar cost averaging ponderado progressivamente. O objetivo é obter retornos relativamente estáveis em mercados com forte direcionalidade, por meio de julgamento de tendência e média de custos.

Princípio

A estratégia é composta principalmente por três partes:

-

Julgamento do sinal de entrada

Utiliza o cruzamento de uma média móvel rápida e uma média móvel lenta como sinal para entrada. De acordo com a configuração do usuário, pode-se escolher SMA, EMA ou HMA como as médias rápida e lenta. Quando a média rápida cruza acima da média lenta, gera um sinal de compra; quando a média rápida cruza abaixo da média lenta, gera um sinal de venda.

-

DCA com ponderação progressiva

Após o sinal de compra ser acionado, a estratégia abre imediatamente uma posição base. Se o preço continuar caindo, a estratégia aumenta as posições de segurança subsequentes de forma ponderada progressiva. O preço de cada nova posição de segurança é ajustado para baixo em uma determinada porcentagem em relação ao preço da posição de segurança anterior. Além disso, o montante de capital para cada nova posição de segurança também é ampliado sucessivamente.

Esse método de aumentar posições gradualmente permite, até certo ponto, realizar a média de custos, obtendo um preço de custo mais favorável enquanto mantém o risco controlável.

-

Take profit e stop loss

Quando o preço sobe e ultrapassa a linha de take profit, a estratégia opta por realizar o lucro; quando o preço cai e ultrapassa a linha de stop loss, a estratégia opta por encerrar a posição.

A linha de take profit é fixada como o preço médio de execução da posição base multiplicado por 1 mais uma porcentagem fixa.

A linha de stop loss acompanha a flutuação do preço da última posição de segurança. O sinal de stop loss é confirmado com base no preço de execução da última posição de segurança, subtraindo uma determinada porcentagem.

Vantagens

-

Combinação de julgamento de tendência e média de custos torna a estratégia mais estável

O julgamento de tendência evita mercados laterais sem direção, e a média de custos permite obter um custo mais favorável na tendência.

-

O aumento progressivo das posições controla o risco

Cada posição subsequente tem um tamanho escalonado, e as posições seguintes exigem um determinado recuo, controlando assim o risco.

-

Monitoramento em tempo real do capital utilizado pela estratégia

O código inclui rótulos de monitoramento em tempo real, permitindo que o usuário saiba claramente o limite de capital utilizado pela estratégia, evitando uso excessivo que leve à liquidação forçada.

-

Flexibilidade no take profit e stop loss de cada posição

A posição base e as posições de segurança podem ter take profit e stop loss separados, garantindo lucros e controlando riscos.

Riscos e Otimizações

-

Fortes oscilações de preço podem levar a múltiplas adições de posições

Em oscilações violentas de preço, podem ser acionadas várias adições de posições, aumentando as perdas. Para reduzir o número de adições, pode-se aumentar adequadamente a exigência de recuo entre as posições de segurança subsequentes.

-

A escolha dos parâmetros da média móvel precisa ser otimizada

Os parâmetros da média móvel afetam diretamente o timing de entrada. Diferentes ativos exigem testes para determinar os parâmetros adequados.

-

As proporções de stop loss e take profit precisam ser testadas e otimizadas

As proporções de stop loss e take profit influenciam a taxa de retorno e o controle de drawdown. Devem ser otimizadas com base em dados de backtest.

-

Pode-se definir condições de encerramento forçado com base em drawdown ou tempo

É possível testar a adição de condições de encerramento forçado quando o drawdown máximo ou o tempo de manutenção da posição ultrapassam um limite, para controlar ainda mais o risco.

Resumo

A estratégia de negociação quantitativa DCA com ponderação progressiva de elementos combina as vantagens do julgamento de tendência e da média de custos, obtendo retornos estáveis em movimentos de tendência forte. Ao otimizar os parâmetros, ajustar o tamanho das posições e as exigências de recuo entre posições, é possível realizar uma negociação estável com risco controlável. Essa estratégia pode ser aplicada em fundos de hedge, fundos CTA e no design de estratégias adversárias.

- 1