Pacientemente rastrear uma estratégia de seguir tendência

Visão Geral

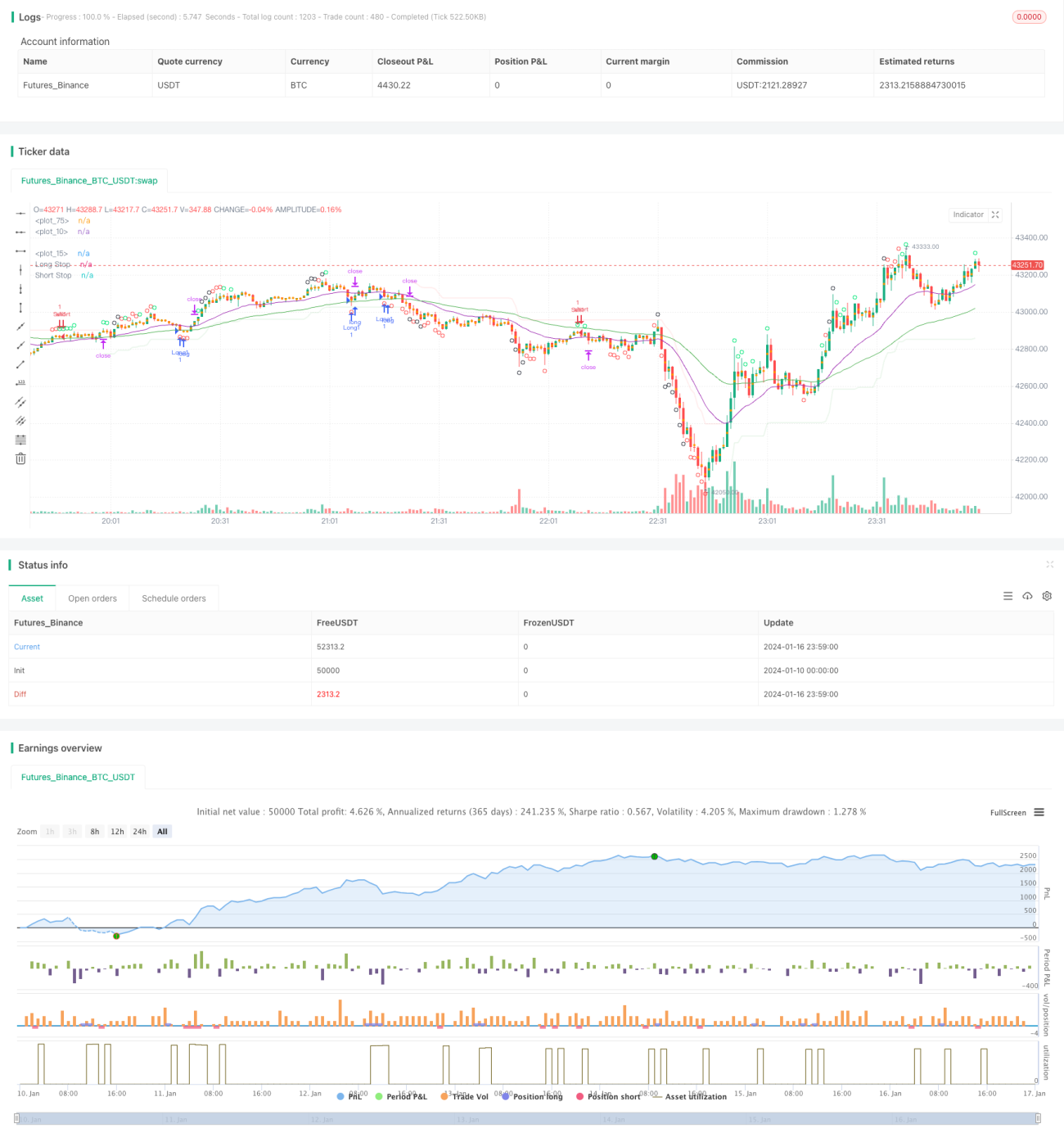

A estratégia de rastreamento de tendência paciente é uma estratégia seguidora de tendência. Ela utiliza uma combinação de médias móveis para determinar a direção da tendência e combina o indicador de sobrecompra/sobrevenda CCI para gerar sinais de negociação. A estratégia busca grandes tendências, evitando ser pego em movimentos laterais.

Princípio da Estratégia

Esta estratégia utiliza a combinação de EMAs de 21 e 55 períodos para determinar a direção da tendência. Quando a EMA de curto prazo está acima da EMA de longo prazo, define-se uma tendência de alta; quando a EMA de curto prazo está abaixo da EMA de longo prazo, define-se uma tendência de baixa.

O indicador CCI é usado para identificar condições de sobrecompra e sobrevenda. Quando o CCI cruza acima da linha -100, é um sinal de sobrevenda no fundo; quando cruza abaixo da linha +100, é um sinal de sobrecompra no topo. De acordo com diferentes níveis de sobrecompra/sobrevenda do CCI, a estratégia possui três níveis de intensidade de sinal de negociação.

Em uma tendência de alta, se o CCI emitir um forte sinal de sobrevenda no fundo, é feita uma entrada longa. Em uma tendência de baixa, se o CCI emitir um forte sinal de sobrecompra no topo, é feita uma entrada short.

O stop loss é definido pelo indicador SuperTrend, e o alvo de lucro é fixado em um número de pontos predeterminado.

Análise das Vantagens

As principais vantagens desta estratégia são:

- Rastreia grandes tendências, evitando ser pego em movimentos contrários.

- O indicador CCI pode identificar efetivamente pontos de reversão.

- O stop loss do SuperTrend é configurado de forma razoável.

- Stop loss fixo e take profit fixo, risco controlável.

Análise de Risco

Os principais riscos desta estratégia são:

- Probabilidade de erro na identificação da grande tendência.

- Probabilidade de sinais falsos do indicador CCI.

- Probabilidade de stop loss muito apertado ou muito largo, causando perdas desnecessárias.

- Probabilidade de o take profit fixo não conseguir capturar completamente o lucro da tendência contínua.

Para mitigar esses riscos, podemos otimizar ajustando os períodos das EMAs, os parâmetros do CCI e os níveis de stop loss/take profit. Também é necessário introduzir mais indicadores para validação dos sinais da estratégia.

Direções de Otimização

As principais direções de otimização para esta estratégia são:

- Testar combinações de mais indicadores para encontrar melhores formas de determinar a tendência e validar sinais.

- Utilizar stop loss/take profit dinâmicos com ATR para melhor rastrear a tendência e controlar o risco.

- Introduzir modelos de aprendizado de máquina treinados com dados históricos para estimar a probabilidade da tendência.

- Ajustar e otimizar os parâmetros para diferentes ativos.

Resumo

A estratégia de rastreamento de tendência paciente é, no geral, uma estratégia seguidora de tendência muito prática. Ela utiliza médias móveis para determinar a direção da grande tendência, o indicador CCI para detectar pontos de reversão, e um stop loss baseado em SuperTrend configurado de forma razoável. Com ajustes de parâmetros e combinação com múltiplos indicadores para validação, esta estratégia pode ser ainda mais otimizada e merece ser acompanhada e testada em tempo real no longo prazo.

- 1