Estratégia de Rompimento de Tendência Unilateral em Oscilação

Visão Geral

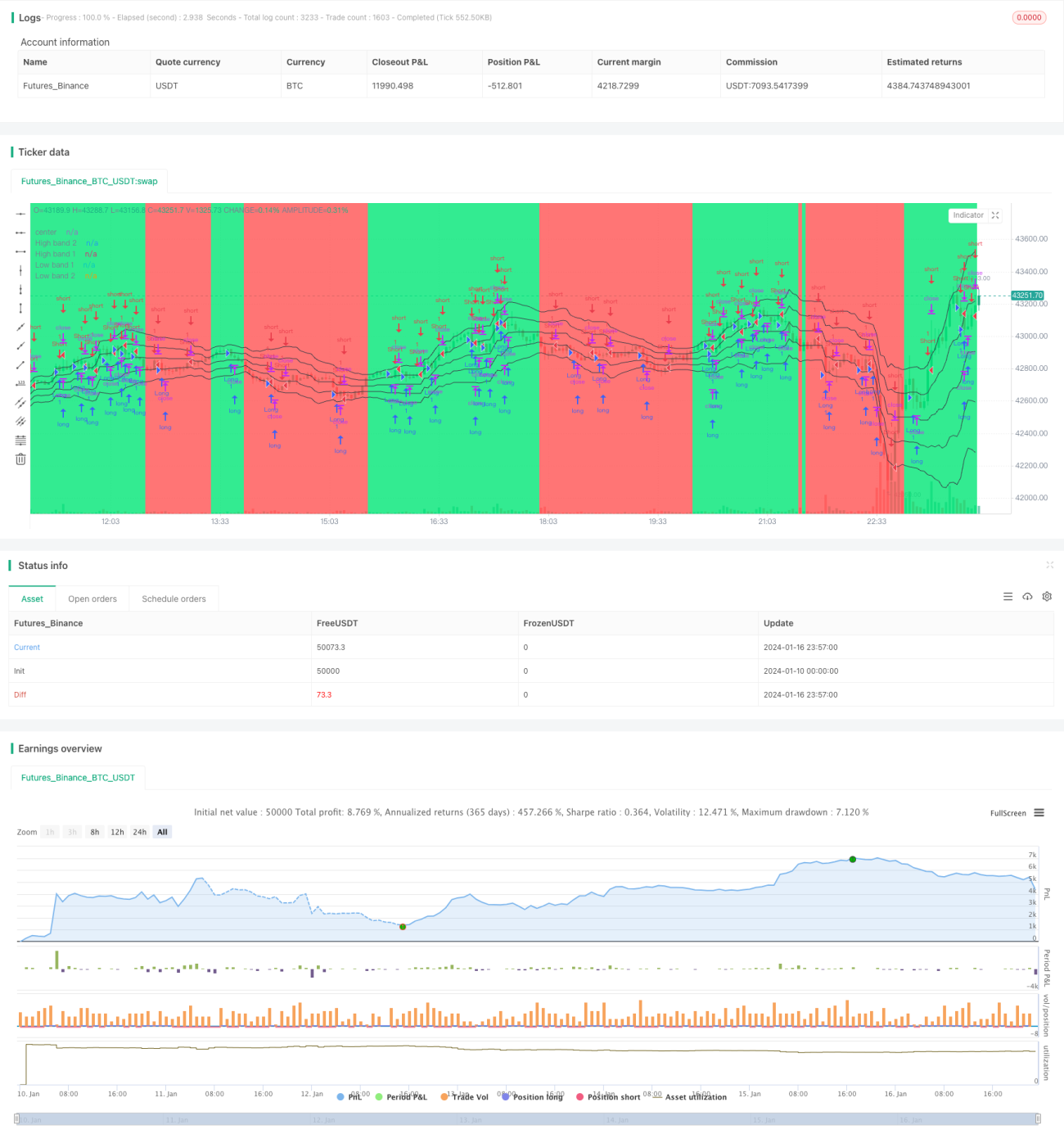

A Estratégia de Rompimento de Tendência Unilateral com Consolidação (Single Side Trend Shock Breakout Strategy) é uma estratégia de rompimento que utiliza um canal de preços e a identificação de tendência. Ela visa identificar a direção da tendência, entrar no mercado quando ocorre um rompimento da zona de consolidação e sair após atingir a meta de lucro definida.

Princípio da Estratégia

A estratégia opera calculando as bandas superior e inferior de um canal de preços e verificando se o preço rompe o canal. Especificamente, a estratégia primeiro calcula a máxima e a mínima dos últimos N períodos, bem como a linha média do preço. Em seguida, calcula a distância absoluta média entre o preço e a linha média para obter as bandas superior e inferior.

Ao identificar a tendência, a estratégia verifica se as últimas barras fecharam todas acima do canal (sinal de alta) ou abaixo do canal (sinal de baixa). Quando a tendência é identificada, a estratégia aguarda uma consolidação do preço e, em seguida, entra no mercado de forma contrária quando ocorre um rompimento próximo à banda superior ou inferior do canal.

Além disso, a estratégia também avalia o rompimento do corpo do candle como um sinal complementar de entrada. Quando o comprimento do corpo do candle excede um múltiplo do comprimento médio do corpo, um sinal é gerado. Após a entrada, a estratégia define uma meta de lucro, saindo ativamente quando o preço a atinge.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Utilizar o canal de preços para identificar a direção da tendência reduz a probabilidade de falsos rompimentos.

- A entrada contrária permite lucrar durante a consolidação da tendência.

- O rompimento do corpo do candle como sinal complementar aumenta a precisão da entrada.

- A definição de uma meta de lucro permite realizar lucros ativamente.

Análise de Riscos

A estratégia também apresenta alguns riscos:

- A parametrização inadequada do canal de preços pode resultar em um canal muito largo ou muito estreito.

- Operar contra a tendência em mercados com tendências fortes pode gerar perdas significativas.

- O rompimento do corpo do candle pode facilmente gerar sinais falsos.

- Uma meta de lucro mal ajustada pode levar à perda de parte dos lucros.

Para reduzir riscos, é possível ajustar os parâmetros para estreitar o canal, evitar posições contrárias em tendências fortes e otimizar a lógica de take profit.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Adicionar indicadores de identificação de tendência para garantir maior precisão.

- Otimizar os parâmetros de rompimento do corpo do candle para reduzir a taxa de falsos sinais.

- Combinar mais indicadores para filtrar os momentos de entrada.

- Ajustar dinamicamente o nível de take profit.

Resumo

A Estratégia de Rompimento de Tendência Unilateral com Consolidação lucra ao entrar de forma contrária durante a consolidação, utilizando um canal de preços e a identificação de tendência. Ela possui vantagens como a identificação da tendência e o take profit ativo, mas também apresenta certos riscos. Através da confirmação por múltiplos indicadores e da otimização de parâmetros, é possível reduzir riscos e aumentar o potencial de lucro. Esta estratégia é adequada para negociação de curto prazo e pode ser usada como complemento a estratégias de tendência.

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Scalper Strategy v1.5", shorttitle = "Scalper str 1.5", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

- 1