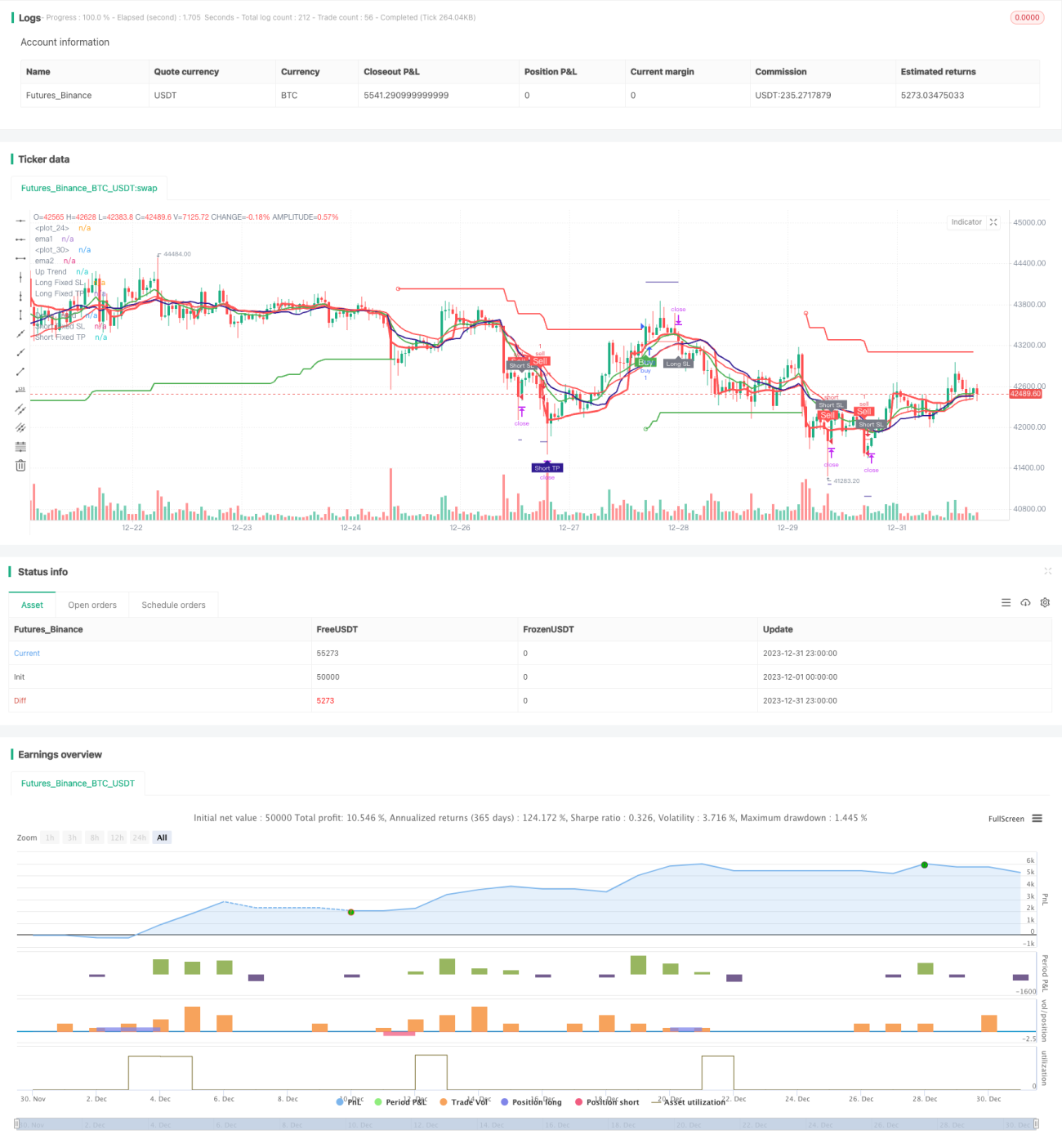

Uma estratégia de negociação quantitativa que utiliza múltiplos indicadores técnicos

Visão Geral

Esta estratégia é uma estratégia de negociação quantitativa que utiliza múltiplos indicadores técnicos. Baseia-se principalmente na combinação de vários indicadores, como o cruzamento de médias móveis exponenciais (EMA), o indicador SuperTrend, o índice de força relativa (RSI) e o MACD, para gerar sinais de negociação.

Princípios da Estratégia

A lógica central de negociação desta estratégia baseia-se nos seguintes aspetos:

-

Cruzamento de Médias Móveis Exponenciais (EMA): São calculadas uma EMA rápida (EMA1) e uma EMA lenta (EMA2). Quando a EMA rápida cruza acima da EMA lenta, gera-se um sinal de compra; quando cruza abaixo, gera-se um sinal de venda.

-

Média Móvel Ponderada por Volume (VWMA): É calculada uma VWMA. Quando o preço de fecho cruza acima desta média, é considerado um sinal de compra; quando cruza abaixo, um sinal de venda.

-

Indicador SuperTrend: As bandas superior e inferior do SuperTrend são calculadas com base no Average True Range (ATR) e no parâmetro multiplicador (

multiplier), determinando a direção da tendência. Gera um sinal de compra numa tendência de alta e um sinal de venda numa tendência de baixa. -

Índice de Força Relativa (RSI): É calculado o RSI. Quando o RSI está acima da linha de sobrecompra, é considerado um sinal de venda; quando está abaixo da zona de sobrevenda, é considerado um sinal de compra.

-

MACD (Convergência/Divergência das Médias Móveis): São calculadas a linha rápida, a linha lenta e a linha de sinal do MACD. Quando a linha rápida cruza acima da linha de sinal, gera-se um sinal de compra; quando cruza abaixo, gera-se um sinal de venda.

Após obter os sinais de negociação dos múltiplos indicadores acima, a estratégia utiliza a lógica "AND" para a tomada de decisão. Isto significa que o sinal final de compra ou venda só é gerado quando vários indicadores emitem o mesmo sinal simultaneamente.

Vantagens da Estratégia

Esta estratégia, ao integrar múltiplos indicadores para avaliar o mercado, pode reduzir eficazmente os falsos sinais. As principais vantagens incluem:

-

Filtragem Composta: A utilização de vários indicadores para uma filtragem composta reduz os sinais errados que um único indicador poderia gerar.

-

Combinação de Tendência e Oscilador: A combinação de indicadores de tendência e osciladores permite obter lucros adicionais em mercados com tendência.

-

Lógica de Stop-Loss Robusta: A implementação de uma lógica de stop-loss completa permite controlar eficazmente a perda máxima por negociação.

-

Lógica de Aumento Progressivo de Posição: A lógica de aumento progressivo de posição (martingale) oferece a oportunidade de recuperar perdas através do aumento da posição.

Riscos da Estratégia

Esta estratégia apresenta principalmente os seguintes riscos:

-

Excesso de Conservadorismo: A combinação de múltiplos indicadores pode ser demasiado conservadora, levando à perda de algumas oportunidades de negociação. A combinação de indicadores pode ser simplificada conforme necessário.

-

Amplificação de Perdas com Martingale: A lógica de aumento progressivo de posição pode ampliar as perdas. O número de vezes para aumentar a posição deve ser limitado de forma razoável.

-

Definição Inadequada de Stop-Loss: Uma definição inadequada do nível de stop-loss pode levar a perdas desnecessárias. Deve ser implementado um stop-loss adaptativo.

-

Parâmetros Inadequados: A definição incorreta dos parâmetros dos indicadores pode gerar demasiados sinais errados. Os parâmetros devem ser otimizados para encontrar a melhor combinação.

Direções de Otimização da Estratégia

Esta estratégia pode ser otimizada nos seguintes aspetos:

-

Avaliação de Pesos: Avaliar o efeito de diferentes combinações de parâmetros dos indicadores e selecionar os pesos adequados para cada um.

-

Teste de Parâmetros: Testar diferentes configurações de parâmetros para os indicadores.

-

Stop-Loss Adaptativo: Adicionar uma lógica de stop-loss adaptativa.

-

Gestão Dinâmica de Posição: Incorporar um mecanismo dinâmico de gestão de posição.

-

Otimização com Machine Learning: Utilizar métodos de aprendizado de máquina para otimizar os parâmetros e o modelo.

Conclusão

No geral, esta estratégia é uma estratégia de negociação quantitativa muito prática. Ela combina as vantagens de múltiplos indicadores técnicos clássicos, permitindo uma avaliação eficaz do mercado. Através da otimização de parâmetros e da iteração do modelo, esta estratégia pode alcançar melhores resultados de negociação.

- 1