Estratégia quantitativa de seguimento de tendência baseada em Wave Trend e VWMA

Visão Geral

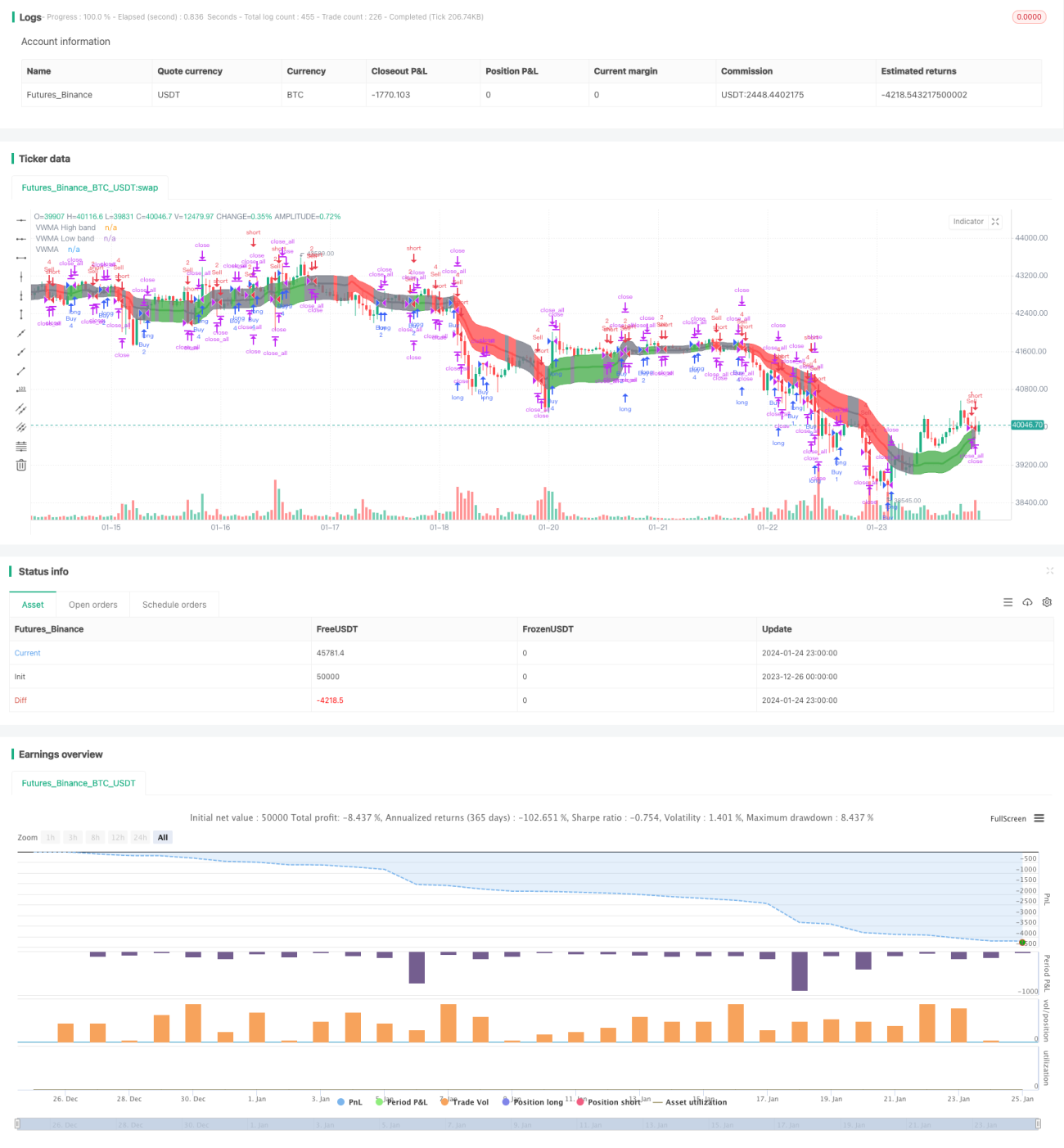

Esta estratégia combina o oscilador Wave Trend e o indicador VWMA para implementar uma estratégia quantitativa de negociação de acompanhamento de tendência. A estratégia pode identificar a tendência do mercado e gerar sinais de compra ou venda com base no oscilador Wave Trend. Além disso, o tamanho da negociação é determinado pelo sinal do indicador VWMA.

Princípio da Estratégia

A estratégia baseia-se principalmente nos dois indicadores a seguir:

-

Oscilador Wave Trend: Este é um indicador portado para o TradingView por LazyBear que pode identificar as "ondas" das flutuações de preço e gerar sinais de compra/venda. O cálculo específico é: primeiro calcula-se a média dos preços (ap), depois calcula-se a EMA de ap (chamada esa), em seguida calcula-se a EMA do valor absoluto da diferença entre ap e esa (chamada d), e finalmente calcula-se o índice de consistência ci = (ap - esa) / (0,015 * d). A EMA de ci é o Wave Trend (wt1), e a SMA de 4 períodos de wt1 é wt2. Quando wt1 cruza acima de wt2, é um sinal de compra; quando cruza abaixo, é um sinal de venda.

-

Indicador VWMA: Este é uma média móvel ponderada pelo volume. Dependendo se o preço está dentro ou fora das Bandas VWMA (bandas superior e inferior do VWMA), gera-se um sinal de +1 (longo), 0 (neutro) ou -1 (curto).

O momento de compra e venda é determinado pelos sinais do Wave Trend. Já a quantidade específica para cada negociação é determinada pelos sinais de longo/curto do indicador VWMA.

Vantagens da Estratégia

- A combinação dos sinais dos dois indicadores pode melhorar a precisão das decisões.

- O indicador VWMA, baseado no volume, permite avaliar a força do mercado.

- O período de negociação é personalizável, evitando flutuações violentas causadas por eventos noticiosos importantes.

- O tamanho da negociação é ajustado de acordo com o sinal do VWMA, o que pode reduzir o risco da negociação.

Riscos da Estratégia

- O indicador Wave Trend pode gerar sinais falsos.

- Dados de volume imprecisos podem afetar o indicador VWMA.

- São necessários longos períodos de dados históricos para o cálculo dos indicadores.

- Não considera uma estratégia de stop loss.

Direções de Otimização

- Testar diferentes combinações de parâmetros para encontrar os melhores.

- Adicionar uma estratégia de stop loss.

- Considerar a combinação com outros indicadores para filtragem de sinais.

- Testar diferentes configurações de período de negociação.

- Ajustar dinamicamente o cálculo do tamanho da negociação.

Resumo

Esta estratégia integra indicadores de tendência e volume para implementar uma estratégia de acompanhamento de tendência relativamente avançada. A estratégia apresenta certas vantagens, mas também envolve alguns riscos que requerem atenção. Através da otimização de parâmetros e regras, é possível melhorar ainda mais a estabilidade e a rentabilidade da estratégia.

- 1