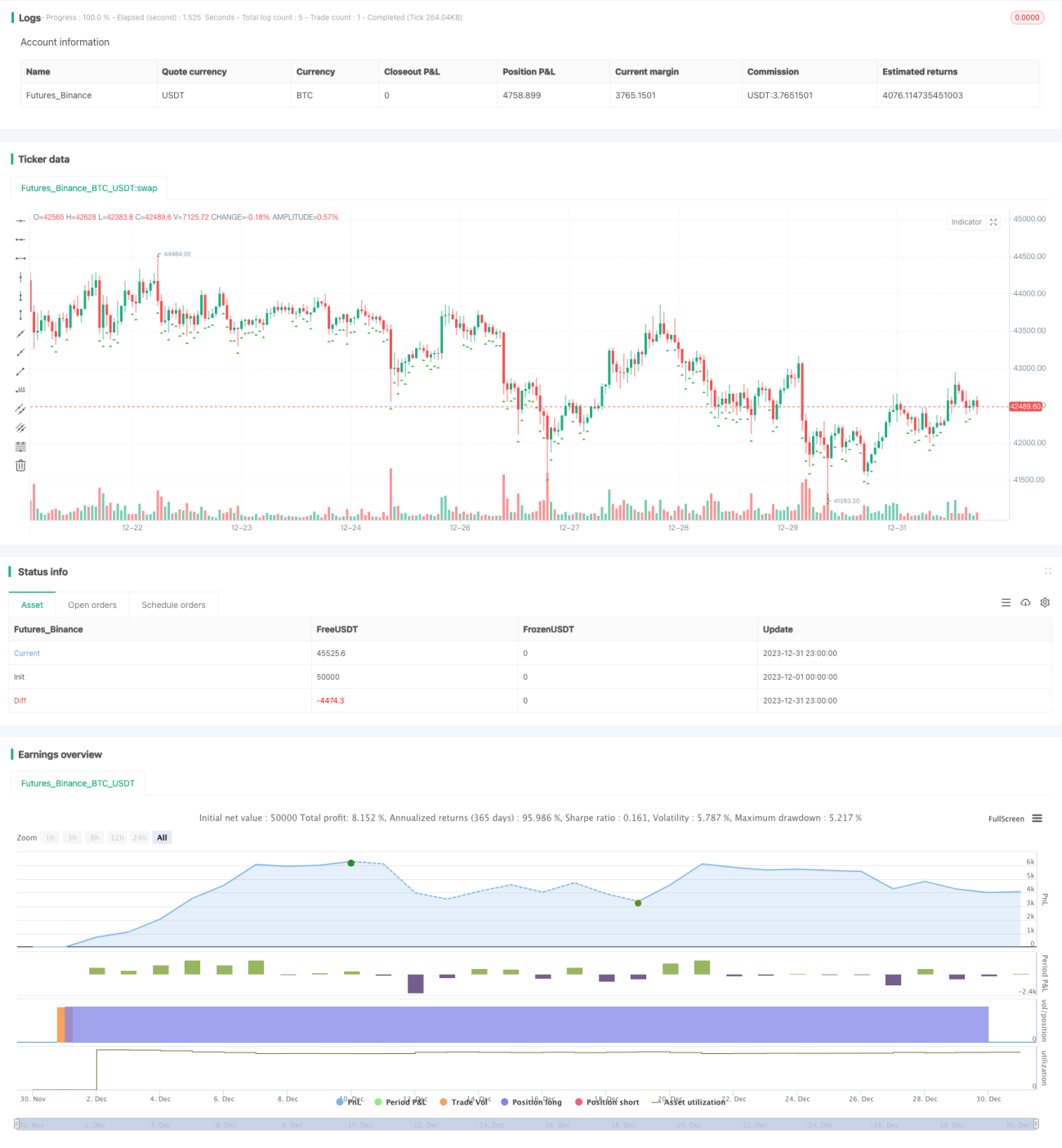

Estratégia de Trading de Sucção com Indicador RSI

Visão Geral

A estratégia de negociação de sucção baseada no indicador RSI é um método de negociação em grade fixa que integra os indicadores técnicos RSI e CCI. A estratégia utiliza os valores dos indicadores RSI e CCI para determinar o momento de entrada, definindo ordens de lucro e de adição de posições com base em uma porcentagem fixa de lucro e um número fixo de grades. Além disso, a estratégia incorpora um mecanismo de hedge para movimentos de preços de ruptura.

Princípio da Estratégia

Condição de Entrada

Quando os indicadores RSI de 5 minutos e 30 minutos estiverem abaixo do limite definido, e o indicador CCI de 1 hora também estiver abaixo do valor definido, é gerado um sinal de compra. Neste momento, o preço de fechamento atual é registrado como preço de entrada, e o tamanho da primeira posição é calculado com base no patrimônio da conta e no número de grades.

Condição de Lucro

Com base no preço de entrada, o preço de lucro é calculado de acordo com a porcentagem de lucro alvo definida, e uma ordem de lucro é colocada nesse nível de preço.

Condição de Adição de Posição

Além da primeira posição, as demais ordens de adição de posições fixas são emitidas uma a uma após o sinal de entrada, até atingir o número definido de grades.

Mecanismo de Hedge

Se o preço subir acima da porcentagem do limite de hedge definida em relação ao preço de entrada, todas as posições são fechadas por hedge.

Mecanismo de Reversão

Se o preço cair abaixo da porcentagem do limite de reversão definida em relação ao preço de entrada, todas as ordens não executadas são canceladas, aguardando novas oportunidades de entrada.

Análise de Vantagens

- Combina os indicadores RSI e CCI para aumentar a probabilidade de lucro.

- Utiliza grades fixas para definir o lucro alvo, aumentando a certeza dos ganhos.

- Integra um mecanismo de hedge para prevenir riscos de flutuações bruscas de preço.

- Inclui um mecanismo de reversão que pode reduzir perdas.

Análise de Riscos

- Probabilidade de sinais falsos gerados pelos indicadores.

- Flutuações bruscas de preço que ultrapassem o limite de hedge.

- Impossibilidade de reentrada após uma reversão que retorna ao ponto inicial.

Esses riscos podem ser reduzidos ajustando os parâmetros dos indicadores, ampliando a margem de hedge e reduzindo a margem de reversão.

Direções de Otimização

- É possível testar mais combinações de indicadores.

- Pode-se estudar um mecanismo de lucro adaptativo.

- A lógica de adição de posições pode ser otimizada.

Resumo

A estratégia de negociação de sucção baseada no indicador RSI determina o momento de entrada através de indicadores, utilizando grades fixas de lucro e adição de posições para garantir lucros estáveis. Ao mesmo tempo, a estratégia conta com hedge contra grandes flutuações e um mecanismo de reentrada após reversão. Essa estratégia integrada de múltiplos mecanismos pode ser usada para reduzir riscos de negociação e aumentar a taxa de lucro. Com mais otimizações dos indicadores e configurações de parâmetros, é possível obter melhores resultados em operações reais.

- 1