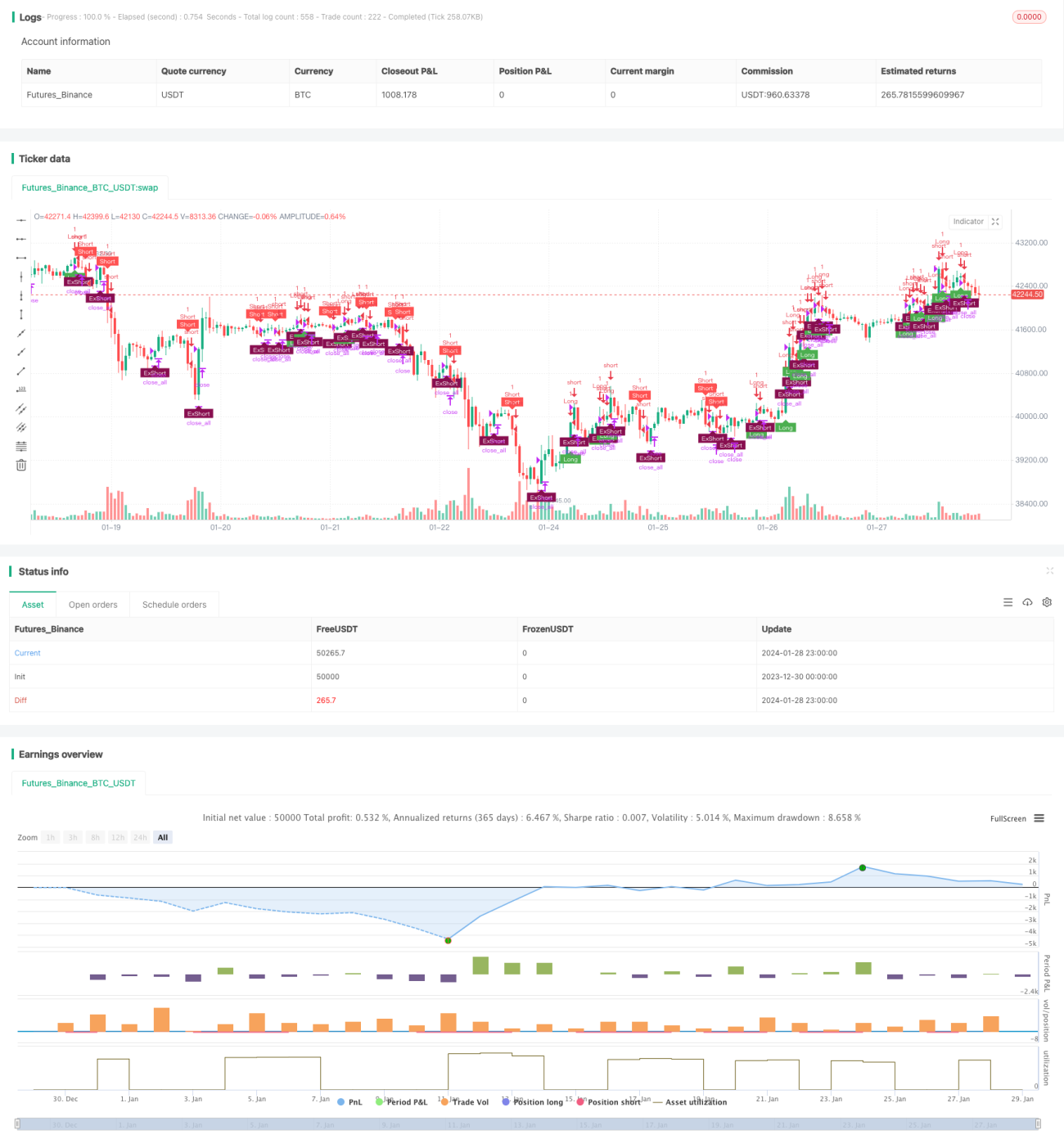

Estratégia de Negociação com RSI Duplo

Visão Geral

A estratégia de negociação de RSI duplo é uma estratégia quantitativa baseada no Índice de Força Relativa (RSI). Ela utiliza simultaneamente um RSI rápido e um RSI lento como sinais de negociação, implementando uma dupla confirmação para melhorar a qualidade dos sinais e filtrar sinais falsos.

Princípio da Estratégia

A estratégia usa dois RSIs com períodos diferentes como principais indicadores de negociação. O RSI rápido tem um período de 5 dias, para capturar condições de sobrecompra/sobrevenda de curto prazo; o RSI lento tem um período de 14 dias, para avaliar a tendência de médio/longo prazo e suportes/resistências chave.

As regras específicas de negociação são:

- Quando o RSI rápido cruza acima de 70 e o RSI lento está acima de 50, compre (long); quando o RSI rápido cruza abaixo de 30 e o RSI lento está abaixo de 50, venda (short).

- O stop loss para posições compradas é quando o RSI rápido cruza abaixo de 55; o stop loss para posições vendidas é quando o RSI rápido cruza acima de 45.

Através da combinação de RSIs rápidos e lentos, a estratégia complementa diferentes períodos, permitindo identificar eficazmente condições de sobrecompra/sobrevenda enquanto confirma a tendência de médio/longo prazo, gerando assim sinais de negociação de alta qualidade. O mecanismo de filtragem dupla do RSI também ajuda a reduzir negociações ruidosas causadas por falsos rompimentos.

Análise de Vantagens

A maior vantagem da estratégia de RSI duplo é filtrar eficazmente sinais falsos, melhorar a qualidade dos sinais, reduzir negociações desnecessárias e diminuir a frequência de negociação. As vantagens específicas são:

- A combinação de RSIs rápidos e lentos identifica pontos de sobrecompra/sobrevenda de curto, médio e longo prazo, aumentando a precisão dos sinais.

- O mecanismo de filtragem dupla do RSI reduz eficazmente o ruído, evitando ficar preso em posições.

- Baixa frequência de negociação ajuda a reduzir custos de transação e perdas por derrapagem.

- O mecanismo de stop loss controla perdas individuais e o drawdown máximo.

Análise de Riscos

A estratégia de RSI duplo também apresenta certos riscos, principalmente provenientes dos seguintes aspetos:

- A inerente defasagem do RSI pode causar atrasos nas negociações.

- O mecanismo de filtragem dupla pode perder algumas oportunidades de negociação.

- Não pode evitar completamente os riscos sistémicos de movimentos extremos de mercado.

Os seguintes métodos podem reduzir os riscos acima:

- Ajustar adequadamente os parâmetros do RSI rápido para aumentar a sensibilidade.

- Otimizar as condições de abertura de posição e stop loss para equilibrar risco e retorno.

- Combinar com sistemas de tendência, algoritmos de aprendizado de máquina, etc.

Direções de Otimização

A estratégia de RSI duplo tem espaço para otimização adicional, principalmente nas seguintes direções:

- Otimizar dinamicamente os parâmetros do RSI, ajustando automaticamente conforme as condições de mercado.

- Adicionar um módulo de gestão de risco baseado em volatilidade.

- Incorporar sinais alternativos como análise de texto e dados sociais.

- Utilizar modelos de aprendizado de máquina para ajudar a filtrar sinais.

Através destas otimizações, é possível melhorar ainda mais a rentabilidade, robustez e adaptabilidade da estratégia.

Resumo

A estratégia de RSI duplo é, no geral, uma estratégia de negociação quantitativa muito prática. Ela combina mecanismos como acompanhamento de tendência, identificação de sobrecompra/sobrevenda e filtragem dupla, formando um sistema de negociação relativamente completo. Esta estratégia destaca-se no controlo de risco e na redução da frequência de negociação, sendo adequada para posições de médio a longo prazo. Com otimização e iteração contínuas, a estratégia de RSI duplo tem potencial para se tornar uma parte importante da nova geração de estratégias quantitativas.

- 1